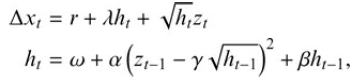

The Heston?Nandi-model for option pricing (Heston and Nandi, 1997, 2000) is specified as where z t? is

Question:

The Heston?Nandi-model for option pricing (Heston and Nandi, 1997, 2000) is specified as

where zt?is again independent and identically standard normally distributed. In going from probability measure P to Q, the model can be written in unchanged algebraic form but with the substitutions ? ? ?Q, zt ? zQt and ? ? ?Q. What are the modified quantities ?Q, zQt?and??Q?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

When changing from probability measure P to Q we need to modify the parameters of the HestonNandi mo...View the full answer

Answered By

Morris Maina

I am a professional teaching in different Colleges and university to solved the Assignments and Project . I am Working more then 3 year Online Teaching in Zoom Meet etc. I will provide you the best answer of your Assignments and Project.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: