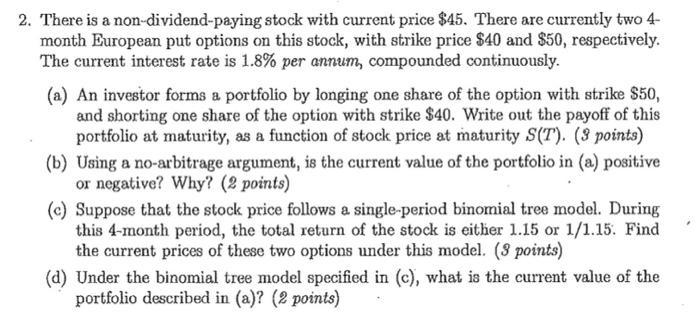

2. There is a non-dividend-paying stock with current price $45. There are currently two 4- month...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

SOLUTION a Let ST denote the stock price at maturity The payoff of the portfolio at maturity is given by Payoff Long Put with strike 50 Short Put with ... View the full answer

Related Book For

Posted Date: