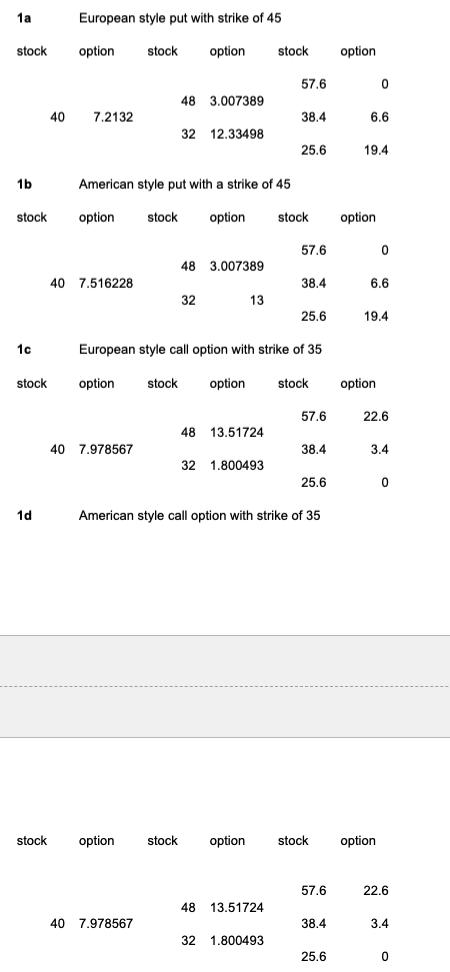

A stock's price is $40. Over each of the next two three month periods it is expected

Question:

A stock's price is $40. Over each of the next two three month periods it is expected to go up or down by

20%. The risk free rate is 6% p.a.

a. What should be the current price of a 6-month European style put option with a strike price of $45?

b. What should be the current price of a 6-month American style put option with a strike price of $45?

c. What should be the current price of a 6-month European style call option with a strike price of $35?

d. What should be the current price of a 6-month American style call option with a strike price of $35?

Since the risk free rate is 6%p.a. and the time period for each option is 3 months we have to change the rate to a per period basis or 1.5% every 3 months. The value of p =(1+.015-.8)/(1.2-.8)= 0.5375. also when we discount we should be discounting by dividing by (1+r)=(1+.015).

Expert Answer: