? Dean and Ellen Price are married and have a manufacturing business. They bought a piece of

Fantastic news! We've Found the answer you've been seeking!

Question:

?

?

Transcribed Image Text:

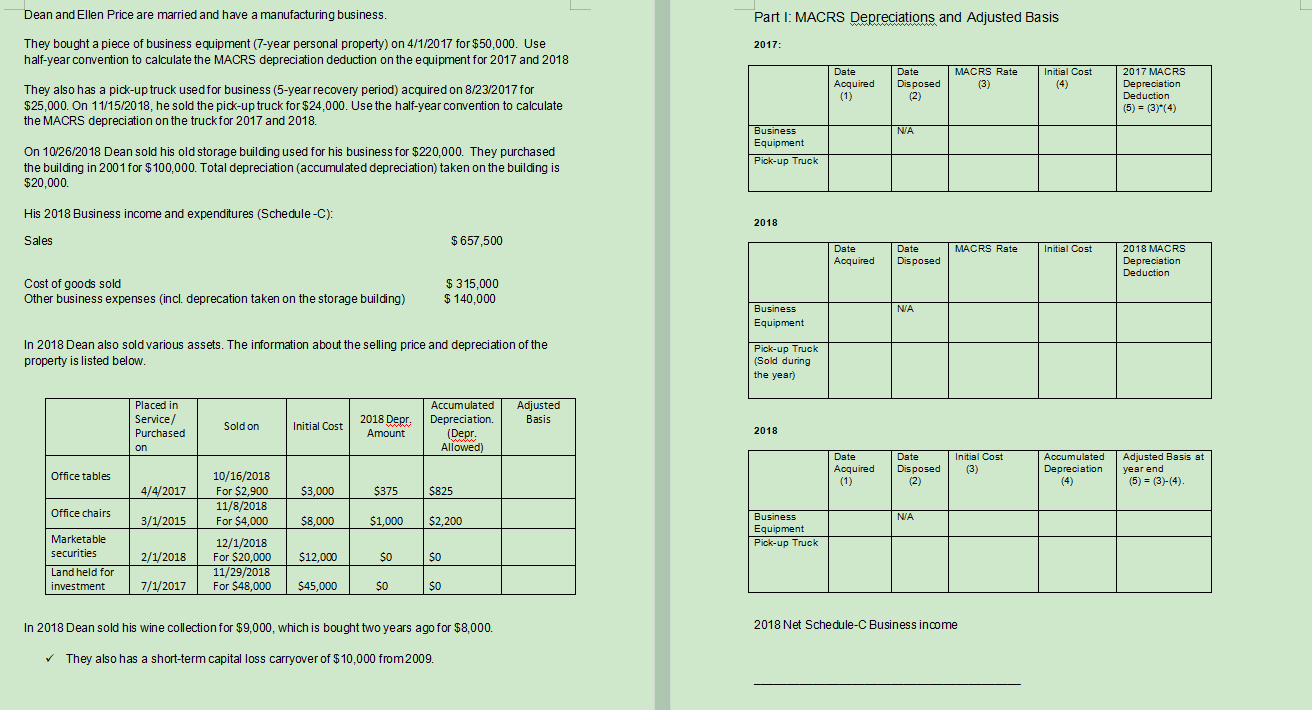

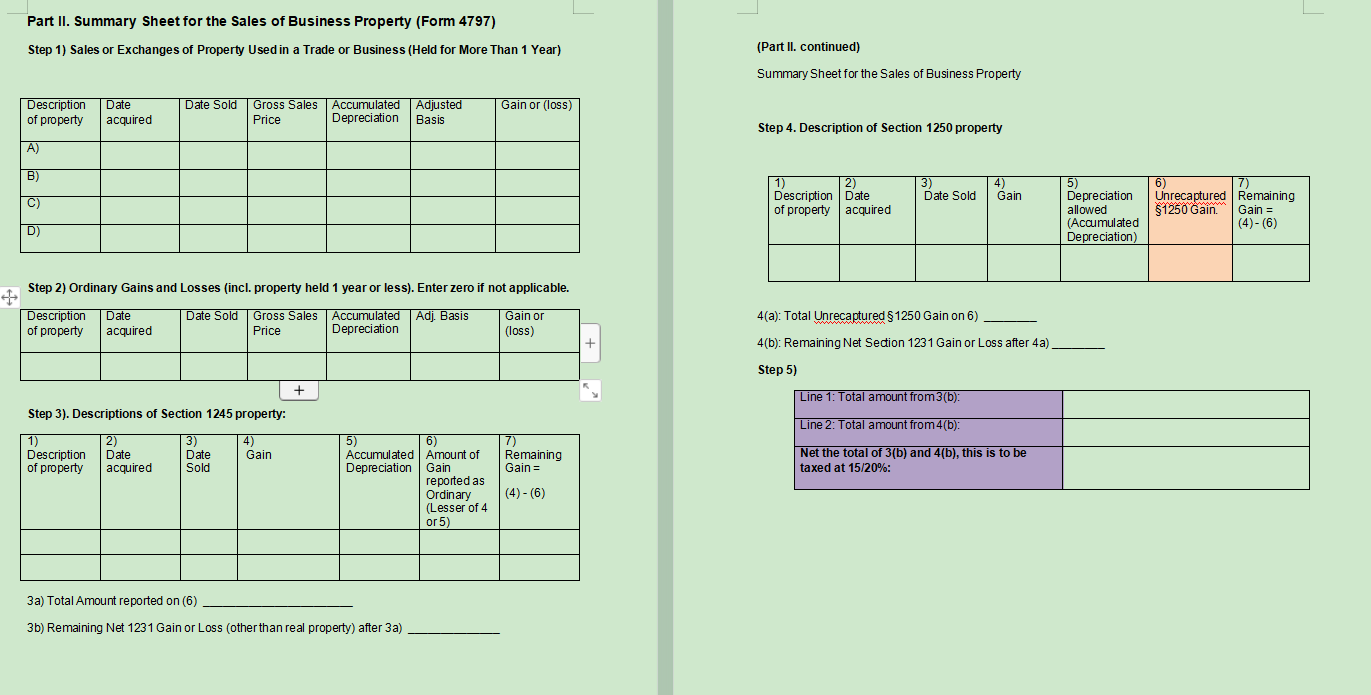

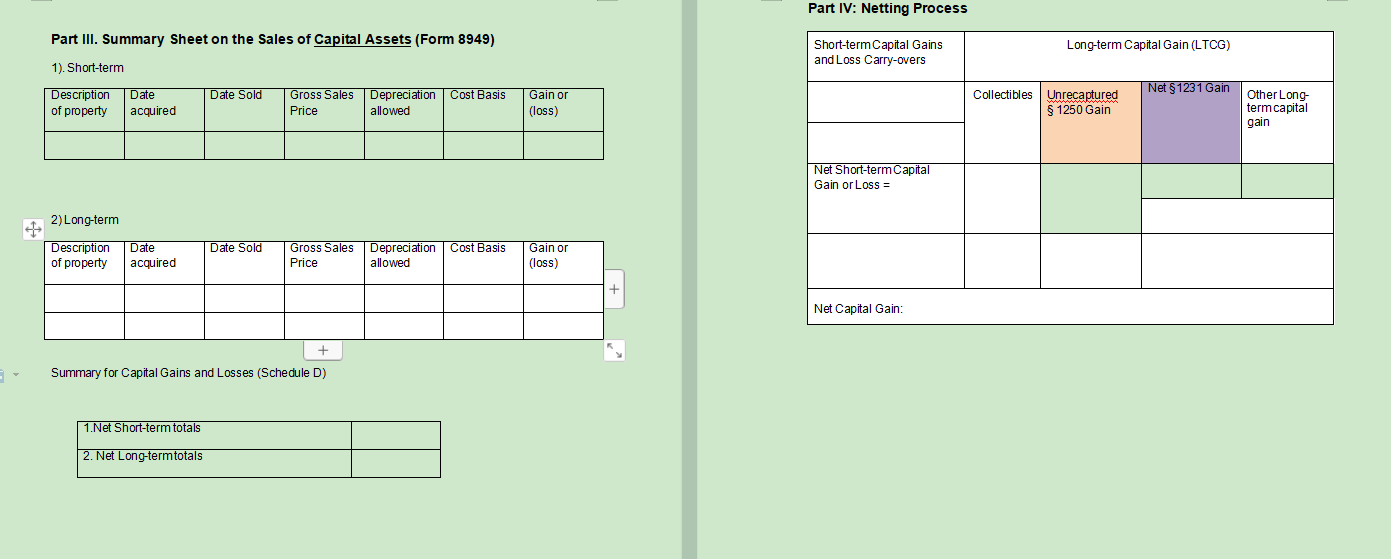

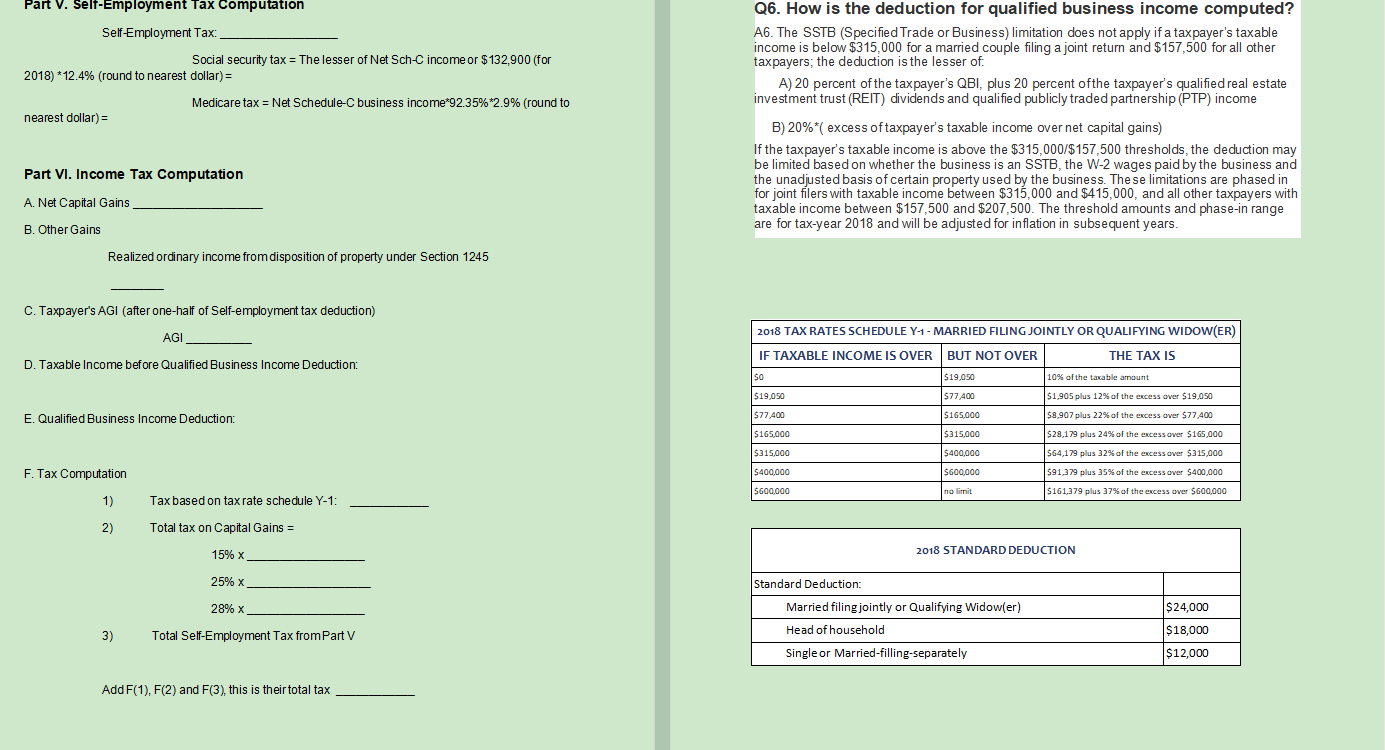

Dean and Ellen Price are married and have a manufacturing business. They bought a piece of business equipment (7-year personal property) on 4/1/2017 for $50,000. Use half-year convention to calculate the MACRS depreciation deduction on the equipment for 2017 and 2018 They also has a pick-up truck used for business (5-year recovery period) acquired on 8/23/2017 for $25,000. On 11/15/2018, he sold the pick-up truck for $24,000. Use the half-year convention to calculate the MACRS depreciation on the truck for 2017 and 2018. On 10/26/2018 Dean sold his old storage building used for his business for $220,000. They purchased the building in 2001 for $100,000. Total depreciation (accumulated depreciation) taken on the building is $20,000. His 2018 Business income and expenditures (Schedule-C): Sales Cost of goods sold Other business expenses (incl. deprecation taken on the storage building) Office tables In 2018 Dean also sold various assets. The information about the selling price and depreciation of the property is listed below. Office chairs Marketable securities Land held for investment Placed in Service/ Purchased on 4/4/2017 3/1/2015 2/1/2018 7/1/2017 Sold on 10/16/2018 For $2,900 11/8/2018 For $4,000 12/1/2018 For $20,000 11/29/2018 For $48,000 Initial Cost $3,000 $8.000 $12,000 $45,000 2018 Depr. Amount $375 $1,000 $0 $0 $ 657,500 $315,000 $140.000 Accumulated Adjusted Depreciation. Basis (Depr Allowed) $825 $0 $2,200 $0 In 2018 Dean sold his wine collection for $9,000, which is bought two years ago for $8,000. ✓ They also has a short-term capital loss carryover of $10,000 from 2009. Part I: MACRS Depreciations and Adjusted Basis 2017: Business Equipment Pick-up Truck 2018 Business Equipment Pick-up Truck (Sold during the year) 2018 Business Equipment Pick-up Truck Date Acquired (1) Date Acquired Date Acquired (1) Date Disposed (2) N/A Date Disposed N/A Date Disposed (2) N/A MACRS Rate (3) MACRS Rate Initial Cost (3) 2018 Net Schedule-C Business income Initial Cost (4) Initial Cost Accumulated Depreciation (4) 2017 MACRS Depreciation Deduction (5) = (3)*(4) 2018 MACRS Depreciation Deduction Adjusted Basis at year end (5) (3)-(4). Part II. Summary Sheet for the Sales of Business Property (Form 4797) Step 1) Sales or Exchanges of Property Used in a Trade or Business (Held for More Than 1 Year) Description Date of property A) B) C) D) acquired Date Sold Gross Sales Accumulated Adjusted Price Depreciation Basis Step 2) Ordinary Gains and Losses (incl. property held 1 year or less). Enter zero if not applicable. + Description Date Date Sold Gross Sales Accumulated | Adj. Basis Price Depreciation Gain or (loss) of property acquired Step 3). Descriptions of Section 1245 property: 1) 2) Description Date 3) Date Sold of property acquired 4) Gain + 5) Accumulated Depreciation 3a) Total Amount reported on (6) 3b) Remaining Net 1231 Gain or Loss (other than real property) after 3a) Gain or (loss) 6) Amount of Gain reported as Ordinary (Lesser of 4 or 5) 7) Remaining Gain = (4)-(6) (Part II. continued) Summary Sheet for the Sales of Business Property Step 4. Description of Section 1250 property 1) 2) Description Date of property acquired 3) Date Sold 4) Gain 4(a): Total Unrecaptured §1250 Gain on 6) 4(b): Remaining Net Section 1231 Gain or Loss after 4a). Step 5) Line 1: Total amount from 3(b): Line 2: Total amount from 4(b): Net the total of 3(b) and 4(b), this is to be taxed at 15/20%: 5) Depreciation allowed (Accumulated Depreciation) 6) Unrecaptured $1250 Gain. 7) Remaining Gain = (4)-(6) Part III. Summary Sheet on the sales of Capital Assets (Form 8949) 1). Short-term Description | Date of property acquired 2) Long-term Description Date of property acquired Date Sold 1.Net Short-term totals 2. Net Long-term totals Date Sold Gross Sales Depreciation Cost Basis Price allowed Gross Sales Depreciation Cost Basis Price allowed + Summary for Capital Gains and Losses (Schedule D) Gain or (loss) Gain or (loss) Part IV: Netting Process Short-term Capital Gains and Loss Carry-overs Net Short-term Capital Gain or Loss = Net Capital Gain: Long-term Capital Gain (LTCG) Collectibles Unrecaptured wwwwwwwwwwwwww § 1250 Gain Net §1231 Gain Other Long- term capital gain Part V. Self-Employment Tax Computation Self-Employment Tax: 2018) *12.4% (round to nearest dollar) = nearest dollar) = Social security tax = The lesser of Net Sch-C income or $132,900 (for Part VI. Income Tax Computation A. Net Capital Gains B. Other Gains Realized ordinary income from disposition of property under Section 1245 Medicare tax = Net Schedule-C business income *92.35% *2.9% (round to C. Taxpayer's AGI (after one-half of Self-employment tax deduction) AGI D. Taxable Income before Qualified Business Income Deduction: F. Tax Computation E. Qualified Business Income Deduction: 1) 2) 3) Tax based on tax rate schedule Y-1: Total tax on Capital Gains = 15% X 25% X 28% X Total Self-Employment Tax from Part V Add F(1), F(2) and F(3), this is their total tax Q6. How is the deduction for qualified business income computed? A6. The SSTB (Specified Trade or Business) limitation does not apply if a taxpayer's taxable income is below $315,000 for a married couple filing a joint return and $157,500 for all other taxpayers; the deduction is the lesser of: A) 20 percent of the taxpayer's QBI, plus 20 percent of the taxpayer's qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income B) 20% *( excess of taxpayer's taxable income over net capital gains) If the taxpayer's taxable income is above the $315,000/$157,500 thresholds, the deduction may be limited based on whether the business is an SSTB, the W-2 wages paid by the business and the unadjusted basis of certain property used by the business. The se limitations are phased in for joint filers with taxable income between $315,000 and $415,000, and all other taxpayers with taxable income between $157,500 and $207,500. The threshold amounts and phase-in range are for tax-year 2018 and will be adjusted for inflation in subsequent years. 2018 TAX RATES SCHEDULE Y-1₁-MARRIED FILING JOINTLY OR QUALIFYING WIDOW(ER) IF TAXABLE INCOME IS OVER THE TAX IS So $19,050 $77,400 $165,000 $315.000 $400,000 $600,000 Standard Deduction: BUT NOT OVER $19,050 $77,400 $165,000 $315,000 $400,000 $600,000 no limit 10% of the taxable amount $1,905 plus 12% of the excess over $19,050 $8,907 plus 22% of the excess over $77,400 $28,179 plus 24% of the excess over $165,000 $64,179 plus 32% of the excess over $315,000 $91,379 plus 35% of the excess over $400,000 $161,379 plus 37% of the excess over $600,000 2018 STANDARD DEDUCTION Married filing jointly or Qualifying Widow(er) Head of household Single or Married-filling-separately $24,000 $18,000 $12,000 Dean and Ellen Price are married and have a manufacturing business. They bought a piece of business equipment (7-year personal property) on 4/1/2017 for $50,000. Use half-year convention to calculate the MACRS depreciation deduction on the equipment for 2017 and 2018 They also has a pick-up truck used for business (5-year recovery period) acquired on 8/23/2017 for $25,000. On 11/15/2018, he sold the pick-up truck for $24,000. Use the half-year convention to calculate the MACRS depreciation on the truck for 2017 and 2018. On 10/26/2018 Dean sold his old storage building used for his business for $220,000. They purchased the building in 2001 for $100,000. Total depreciation (accumulated depreciation) taken on the building is $20,000. His 2018 Business income and expenditures (Schedule-C): Sales Cost of goods sold Other business expenses (incl. deprecation taken on the storage building) Office tables In 2018 Dean also sold various assets. The information about the selling price and depreciation of the property is listed below. Office chairs Marketable securities Land held for investment Placed in Service/ Purchased on 4/4/2017 3/1/2015 2/1/2018 7/1/2017 Sold on 10/16/2018 For $2,900 11/8/2018 For $4,000 12/1/2018 For $20,000 11/29/2018 For $48,000 Initial Cost $3,000 $8.000 $12,000 $45,000 2018 Depr. Amount $375 $1,000 $0 $0 $ 657,500 $315,000 $140.000 Accumulated Adjusted Depreciation. Basis (Depr Allowed) $825 $0 $2,200 $0 In 2018 Dean sold his wine collection for $9,000, which is bought two years ago for $8,000. ✓ They also has a short-term capital loss carryover of $10,000 from 2009. Part I: MACRS Depreciations and Adjusted Basis 2017: Business Equipment Pick-up Truck 2018 Business Equipment Pick-up Truck (Sold during the year) 2018 Business Equipment Pick-up Truck Date Acquired (1) Date Acquired Date Acquired (1) Date Disposed (2) N/A Date Disposed N/A Date Disposed (2) N/A MACRS Rate (3) MACRS Rate Initial Cost (3) 2018 Net Schedule-C Business income Initial Cost (4) Initial Cost Accumulated Depreciation (4) 2017 MACRS Depreciation Deduction (5) = (3)*(4) 2018 MACRS Depreciation Deduction Adjusted Basis at year end (5) (3)-(4). Part II. Summary Sheet for the Sales of Business Property (Form 4797) Step 1) Sales or Exchanges of Property Used in a Trade or Business (Held for More Than 1 Year) Description Date of property A) B) C) D) acquired Date Sold Gross Sales Accumulated Adjusted Price Depreciation Basis Step 2) Ordinary Gains and Losses (incl. property held 1 year or less). Enter zero if not applicable. + Description Date Date Sold Gross Sales Accumulated | Adj. Basis Price Depreciation Gain or (loss) of property acquired Step 3). Descriptions of Section 1245 property: 1) 2) Description Date 3) Date Sold of property acquired 4) Gain + 5) Accumulated Depreciation 3a) Total Amount reported on (6) 3b) Remaining Net 1231 Gain or Loss (other than real property) after 3a) Gain or (loss) 6) Amount of Gain reported as Ordinary (Lesser of 4 or 5) 7) Remaining Gain = (4)-(6) (Part II. continued) Summary Sheet for the Sales of Business Property Step 4. Description of Section 1250 property 1) 2) Description Date of property acquired 3) Date Sold 4) Gain 4(a): Total Unrecaptured §1250 Gain on 6) 4(b): Remaining Net Section 1231 Gain or Loss after 4a). Step 5) Line 1: Total amount from 3(b): Line 2: Total amount from 4(b): Net the total of 3(b) and 4(b), this is to be taxed at 15/20%: 5) Depreciation allowed (Accumulated Depreciation) 6) Unrecaptured $1250 Gain. 7) Remaining Gain = (4)-(6) Part III. Summary Sheet on the sales of Capital Assets (Form 8949) 1). Short-term Description | Date of property acquired 2) Long-term Description Date of property acquired Date Sold 1.Net Short-term totals 2. Net Long-term totals Date Sold Gross Sales Depreciation Cost Basis Price allowed Gross Sales Depreciation Cost Basis Price allowed + Summary for Capital Gains and Losses (Schedule D) Gain or (loss) Gain or (loss) Part IV: Netting Process Short-term Capital Gains and Loss Carry-overs Net Short-term Capital Gain or Loss = Net Capital Gain: Long-term Capital Gain (LTCG) Collectibles Unrecaptured wwwwwwwwwwwwww § 1250 Gain Net §1231 Gain Other Long- term capital gain Part V. Self-Employment Tax Computation Self-Employment Tax: 2018) *12.4% (round to nearest dollar) = nearest dollar) = Social security tax = The lesser of Net Sch-C income or $132,900 (for Part VI. Income Tax Computation A. Net Capital Gains B. Other Gains Realized ordinary income from disposition of property under Section 1245 Medicare tax = Net Schedule-C business income *92.35% *2.9% (round to C. Taxpayer's AGI (after one-half of Self-employment tax deduction) AGI D. Taxable Income before Qualified Business Income Deduction: F. Tax Computation E. Qualified Business Income Deduction: 1) 2) 3) Tax based on tax rate schedule Y-1: Total tax on Capital Gains = 15% X 25% X 28% X Total Self-Employment Tax from Part V Add F(1), F(2) and F(3), this is their total tax Q6. How is the deduction for qualified business income computed? A6. The SSTB (Specified Trade or Business) limitation does not apply if a taxpayer's taxable income is below $315,000 for a married couple filing a joint return and $157,500 for all other taxpayers; the deduction is the lesser of: A) 20 percent of the taxpayer's QBI, plus 20 percent of the taxpayer's qualified real estate investment trust (REIT) dividends and qualified publicly traded partnership (PTP) income B) 20% *( excess of taxpayer's taxable income over net capital gains) If the taxpayer's taxable income is above the $315,000/$157,500 thresholds, the deduction may be limited based on whether the business is an SSTB, the W-2 wages paid by the business and the unadjusted basis of certain property used by the business. The se limitations are phased in for joint filers with taxable income between $315,000 and $415,000, and all other taxpayers with taxable income between $157,500 and $207,500. The threshold amounts and phase-in range are for tax-year 2018 and will be adjusted for inflation in subsequent years. 2018 TAX RATES SCHEDULE Y-1₁-MARRIED FILING JOINTLY OR QUALIFYING WIDOW(ER) IF TAXABLE INCOME IS OVER THE TAX IS So $19,050 $77,400 $165,000 $315.000 $400,000 $600,000 Standard Deduction: BUT NOT OVER $19,050 $77,400 $165,000 $315,000 $400,000 $600,000 no limit 10% of the taxable amount $1,905 plus 12% of the excess over $19,050 $8,907 plus 22% of the excess over $77,400 $28,179 plus 24% of the excess over $165,000 $64,179 plus 32% of the excess over $315,000 $91,379 plus 35% of the excess over $400,000 $161,379 plus 37% of the excess over $600,000 2018 STANDARD DEDUCTION Married filing jointly or Qualifying Widow(er) Head of household Single or Married-filling-separately $24,000 $18,000 $12,000

Expert Answer:

Answer rating: 100% (QA)

Step 1 Compute the Depreciations For a 7year property it is in the MACRS table that year 1 is 1429 Therefore the computation is as follows Using straight line method Year 2018 Depreciation 50000 x 142... View the full answer

Related Book For

Horngrens Accounting

ISBN: 978-0133117417

10th edition

Authors: Tracie L. Miller-Nobles, Brenda L. Mattison, Ella Mae Matsumura

Posted Date:

Students also viewed these accounting questions

-

Bene Petit currently offers three meal sizes: single-serve, dual-serve, and family-sized. Single-serve meals make up about 5% of total sales revenue and have the lowest contribution margin of the...

-

Casandra and Gene are married and have a daughter who is a junior at State University. Their adjusted gross income for the year is $78,000, and they are in the 25% marginal tax bracket. They paid...

-

Jason and Jill are married and have a six-year-old daughter. During the year, they sell one acre of land for $80,000. Three years ago, they paid $70,000 for two acres of land. Their other income and...

-

A company sells four types of gift packages. The cost per unit and demand for each package type is shown in the table below. A fixed cost of $1,000 is also incurred for each different type of gift...

-

What competitive advantages and disadvantages do regional chains have in comparison with national chains?

-

STATEMENT OF CASH FLOWS Refer to Problem 23-9B. The following additional information was obtained from Kenningtons financial statements and auxiliary records for the year ended December 31, 20-2....

-

Consider the regression models described in Example 8.4. Example 8.4 a. Graph the response function associated with Eq. (8.10). Equation (8.10) b. Graph the response function associated with Eq....

-

McIver's Swimwear Distributors is a relatively small, privately held swimwear distribution company that operates in the Midwest and handles several product lines, including footwear, clothing, and...

-

Q1. You work at a space agency and are responsible for designing an energy portfolio for setting up a human colony on a celestial body that is X km away from the sun, and Y km away from the earth....

-

A box B contains 1 white ball, 3 red balls and 2 black balls. Another box B contains 2 white balls, 3 red balls and 4 black balls. A third box B3 contains 3 white balls, 4 red balls and 5 black...

-

78. An 8 year old child sustains fall from height while flying kite on the roof. He develops gross swelling over right ankle immediately. He is taken to a doctor whereby X rays were done which don't...

-

The issued share capital of Edwards ple consists of 800,000 ordinary shares. There are no preference shares. Some years ago, the entity issued EUR 2m of 10 per cent convertible loan stock. The...

-

(a) What is a construction contract? (b) How and why should construction contracts be combined or segmented? (c) How is the stage of completion determined? (d) What is the effect of variations and...

-

Section 11.5.4, used the linear associator algorithm to make two vector pair associations. Select three (new) vector pair associations and solve the same task. Test whether your linear associator is...

-

The appellant is Arkansas Insurance Commissioner W. H. L. Woodyard, III. The appellee is Arkansas Diversified Insurance Company (ADIC). ADIC sought a certificate of authority from Woodyard to sell...

-

In 2003, then U.S. Secretary of Defense Donald Rumsfeld won Britain's Plain English Campaign 2003 Golden Bull Award for this statement: "Reports that say that something hasn't happened are always...

-

A worker having an hourly wage rate of Rs. 23 produces 309 pieces of a job in the normal time of 46 hours of a week. If the allowed time per piece is 13 minutes. calculate the bonus earned by the...

-

Subprime loans have higher loss rates than many other types of loans. Explain why lenders offer subprime loans. Describe the characteristics of the typical borrower in a subprime consumer loan.

-

What is cost-volume-pro fit analysis?

-

How is the times-interest-earned ratio calculated and what does it evaluate?

-

Brett Knight Company operates four bowling alleys. The owner just received the October 31 bank statement from City National Bank, and the statement shows an ending balance of $905. Listed on the...

-

The circuit in Figure P32.96 represents your planned design for a wall power supply that will run a radio that usually runs on a 9-V battery. The power supply uses a transformer (not shown) to...

-

Your boss has purchased a new AC power source to run a high-voltage, low-current display, but it is not working. While he is fuming, you look at the owner's manual and discover that this power source...

-

Construct a phasor diagram representing the current and potential difference in Figure 32. 10 at \(t=T / 4, T / 2\), and \(3 T / 4\). Data from Figure 32.10 Ve maximum, current zero Ve minimum,...

Study smarter with the SolutionInn App