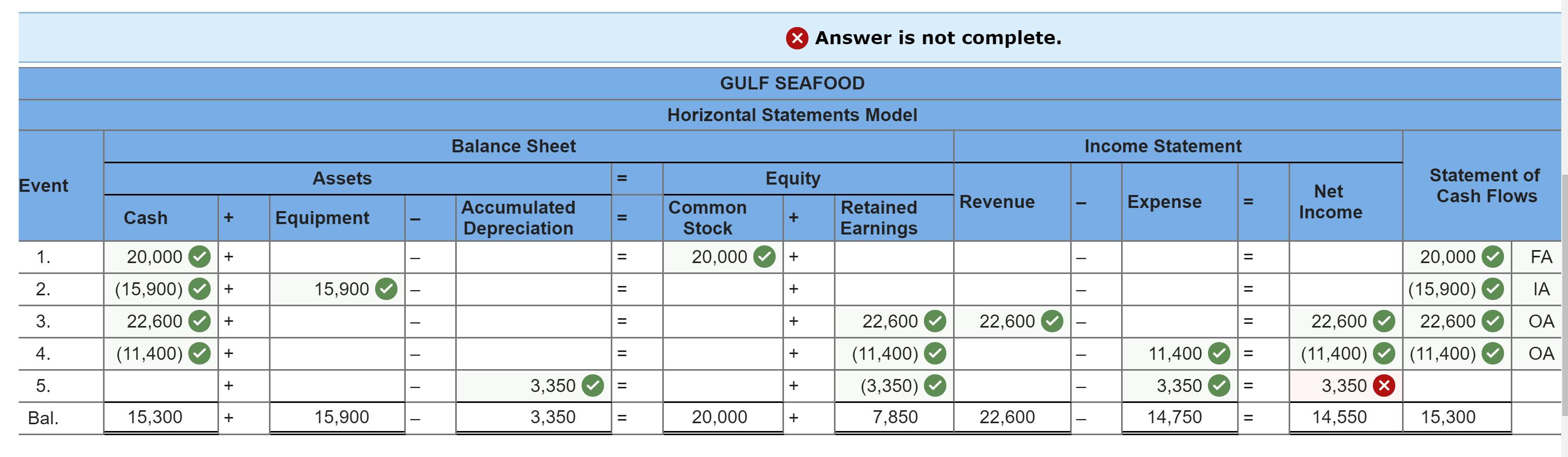

The following events apply to Gulf Seafood for the Year 1 fiscal year: The company started when

Fantastic news! We've Found the answer you've been seeking!

Question:

The following events apply to Gulf Seafood for the Year 1 fiscal year:

- The company started when it acquired $20,000 cash by issuing common stock.

- Purchased a new cooktop that cost $15,900 cash.

- Earned $22,600 in cash revenue.

- Paid $11,400 cash for salaries expense.

- Adjusted the records to reflect the use of the cooktop. Purchased on January 1, Year 1, the cooktop has an expected useful life of four years and an estimated salvage value of $2,500. Use straight-line depreciation. The adjusting entry was made as of December 31, Year 1.

Required:

a. Record the above transactions in a horizontal statements model. (In the Cash Flow column, indicate whether the item is an operating activity (OA), an investing activity (IA), a financing activity (FA) and net change in cash (NC). Enter any decreases to account balances and cash outflows with a minus sign. Not all cells in the "Statement of Cash Flows" column may require an input - leave cells blank if there is no corresponding input needed.)

Expert Answer:

Related Book For

Introductory Financial Accounting for Business

ISBN: 978-1260299441

1st edition

Authors: Thomas Edmonds, Christopher Edmonds

Posted Date: