Assume that you are the auditor of ABC Inc, for the fiscal year 2006. No audit procedures

Question:

Assume that you are the auditor of ABC Inc, for the fiscal year 2006. No audit procedures have been performed other than general information gathering. Please read all the information given below carefully and then identify any possible material misstatements that exist in the accompanying financial statements and the notes. Brief Description of Operations and Management obtained during general information gathering:

ABC Inc. is a large publicly held corporation that is involved in manufacturing operations. ABC’s manufacturing operations are spread over 4 states and 2 foreign countries. The company has reasonably reliable internal controls. It maintains an in-house internal audit function, which is run by an experienced and well trained group of company employees, who are answerable only to an audit committee comprised of independent directors. The divisional managers of the company decide the timing and scope of all internal audit work. The internal auditors also spend a significant amount of time on consulting work in addition to their usual internal audit compliance work. Due to the large geographical coverage and international operations, the divisional managers have to deal with complex revenue recognition, asset valuation and, transfer pricing issues. This makes it necessary for the divisional managers to use their judgment and discretion to come up with various estimates for some of the company’s complex transactions. The company’s external audit is performed by a Big 4 accounting firm. ABC Inc. is the largest client for the Big 4 accounting firm office, located in the region where the company is incorporated. The company rotates its external auditors at regular intervals.

The divisional managers’ compensation plans consist of a relatively low fixed salary. A significant part of the compensation consists of generous and large bonuses that are dependent on meeting aggressive earnings and performance targets. Through this compensation scheme, the board of directors hopes to encourage the divisional managers to improve ABC’s overall earnings performance. The divisional managers have struggled to meet these earnings targets in the past 3 quarters. The manufacturing industry as a whole has experienced a marginal growth in sales for the last three years amidst increasing competition from local and foreign companies.

Gross Profit: Our gross profit margin increased to 66.1 percent in 2006 from 64.5 percent in 2005. Our gross margin was favorably impacted by improvements in the business model. Specifically, we decided to change the method of recognizing gross profit from a version of the Installment Sales method to a modified version of Point of Sale method. Although the Installment Sales method has been applied consistently in previous years, this change was implemented because the Point of Sale method is considered more appropriate. By changing to the Point of Sale recognition method, we were able to recognize additional gross profits of $585. Our gross margin in 2006 was also impacted favorably by price increases, partially offset by increases in the cost of raw materials and freight, primarily in North America, and by an unfavorable product mix. In 2007, the Company expects the cost of raw materials to increase, primarily in North America. We will attempt to mitigate the overall impact on our business through appropriate pricing and other strategies. Gross profit margin in 2006 was favorably impacted by the receipt of approximately $109 million in proceeds related to a class action lawsuit settlement concerning price-fixing in the sale of high fructose corn syrup ("HFCS") purchased by the Company during the years 1991 to 1995. The Company's portion of the settlement was approximately $87 million, which was recorded as a reduction of cost of goods sold. Our gross profit margin decreased to 64.5 percent in 2005 from 64.7 percent in 2004, primarily due to higher raw material and freight costs driven by rising oil prices. As discussed above, in 2006, this decrease was partially offset by the receipt of net settlement proceeds of approximately $87 million.

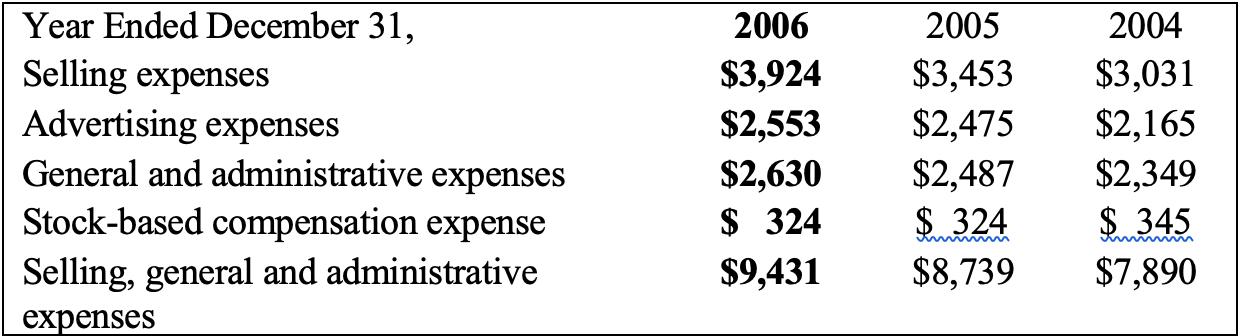

Total selling, general and administrative expenses were approximately 8 percent higher in 2006 versus 2005. The increases in selling and advertising expenses were primarily related to increased investments in marketing activities, combined with new product innovation activities. General and administrative expenses in 2006 also reflected the impact of a $100 million donation made to ABC Inc Foundation. Stock-based compensation expense was flat in 2006 compared to 2005. Stock-based compensation expense in 2005 included approximately $50 million of expense due to a change in our estimated service period for retirement-eligible participants in our plans. This amount was offset primarily by the impact of the timing of stock-based compensation grants in prior years.

As of December 31, 2006, we had approximately $376 million of total unrecognized compensation cost related to non-vested share-based compensation arrangements granted under our plans. This cost is expected to be recognized as stock-based compensation expense over a weighted-average period of 8 years. This amortization of the cost is in accordance with industry practices. This expected cost does not include the impact of any future stock-based compensation awards.

Other Operating Charges: During 2006, our Company recorded other operating charges of $185 million. Of these charges, approximately $108 million were primarily related to the impairment of assets and investments in our bottling operations, approximately $53 million were for contract termination costs related to production capacity efficiencies and approximately $24 million were related to other restructuring costs. The company decided to capitalize other operating charges worth $96 million, which related to costs of replacement of small value items in its manufacturing facilities. The company will depreciate these assets over a period of 6 years on a straight-line basis.

Operating Income and Operating Margin: In 2006, price increases across the majority of operating segments favorably impacted both operating income and operating margins, while increased spending on marketing and innovation activities negatively impacted operating income and operating margins. Although operating margin was at a healthy rate, it was slightly below the industry levels and analysts expectations.

Other Income: Other income indicated a net income of $195 million for 2006 compared to a net loss of $93 million for 2005, a difference of $288 million. In 2006, other income (loss) included a net gain of approximately $175 million resulting from the sale of a portion of our shares held as long-term investments and a gain of approximately $123 million resulting from the sale of a portion of our investment in an IPO of a competitor company. Other income was also significantly affected by the inclusion of gain of $75 million from sale of company’s operational assets, which were damaged in a fire, to some of its own customers. Balance Sheet (All numbers are in millions)

Inventories

Inventories consist primarily of raw materials and packaging (which includes ingredients and supplies), finished goods (which includes concentrates and syrups in our concentrate and foodservice operations, and finished beverages in our bottling and canning operations). Inventories are valued at the lower of cost or market. We determine cost on the basis of the average cost or first-in, first-out methods. During 2006 we changed the valuation method for some of our inventory items from average cost to first- in first-out method to ensure that the valuation of all items belonging to a particular inventory category was done using the same method. This change in valuation method increased inventory value by $91 million.

In November 2004, the FASB issued SFAS No. 151, "Inventory Costs, an amendment of Accounting Research Bulletin No. 43, Chapter 4." SFAS No. 151 requires that abnormal amounts of idle facility expense, freight, handling costs and wasted materials (spoilage) be recorded as current period charges and that the allocation of fixed production overheads to inventory be based on the normal capacity of the production facilities. The Company adopted SFAS No. 151 on January 1, 2006. The adoption of SFAS No. 151 did not have a material impact on our consolidated financial statements and hence we do not report on it.

Cash Equivalents: We classify marketable securities that are highly liquid and have maturities of twelve months or less at the date of purchase as cash equivalents. Prior to the current year we classified securities with maturities of three months or less as cash equivalents, this change in classification increased our cash balance by $95 million. We manage our exposure to counterparty credit risk through specific minimum credit standards, diversification of counterparties and procedures to monitor our credit risk concentrations.

Trade Accounts Receivable: We record trade accounts receivable at net realizable value. This value includes an appropriate allowance for estimated uncollectible accounts to reflect any loss anticipated on the trade accounts receivable balances and charged to the provision for doubtful accounts. We calculate this allowance based on our history of write-offs, level of past-due accounts based on the contractual terms of the receivables, and our relationships with and the economic status of our bottling partners and customers.

All of ABC Inc.’s sales are made to distributors under agreements allowing right of return. Accounts Receivables include $178 million for goods that were sold in December and it is likely that approximately 70% of these goods will be returned.

Property Plant and Equipment: Property, plant and equipment are stated at cost. Repair and maintenance costs that do not improve service potential or extend economic life are expensed as incurred. Depreciation is recorded principally by the straight-line method over the estimated useful lives of our assets, which generally have the following ranges: buildings and improvements: 40 years or less; machinery and equipment: 15 years or less; containers: 10 years or less.

Machinery and equipment contains interest costs of $115 million. These costs were related to the construction of certain infrastructure facilities such as roads and street lighting in the immediate area surrounding the company’s manufacturing plant

Goodwill, Trademarks and Other Intangible Assets: In accordance with SFAS No. 142, "Goodwill and Other Intangible Assets," we classify intangible assets into three categories: (1) intangible assets with definite lives subject to amortization, (2) intangible assets with indefinite lives not subject to amortization, and (3) goodwill. We test intangible assets with definite lives for impairment if conditions exist that indicate the carrying value may not be recoverable. Such conditions may include an economic downturn in a geographic market or a change in the assessment of future operations. We record an impairment charge when the carrying value of the definite lived intangible asset is not recoverable by the cash flows generated from the use of the asset. Purchases of property, plant and equipment accounted for the most significant cash outlays for investing activities in each of the three years ended December 31, 2006. Our Company currently estimates that purchases of property, plant and equipment in 2007 will be approximately $1.5 billion. Acquisitions and investments represented the next most significant investing activity, accounting for $901 million in 2006. In 2006, our Company acquired a controlling interest in CCCIL. The remaining amount of cash used for acquisitions and investments was primarily related to the acquisition of various trademarks and brands, none of which were individually significant. Investing activities in 2006 also included proceeds of approximately $198 million received from the sale of shares in connection with the public offering of ABC Inc. and proceeds of approximately $427 million received from the sale of a portion of ABC Inc.’s long term investments. The profits from the sale of these investments were included in “other income”.

Cash Flows from Financing Activities:

Based on your reading of the case, please answer the following questions:

Based on the reading of only the “Brief Description of Operations and Management obtained during general information gathering” list all possible fraud risk factors included in that section. Do not refer to, or base your answer, on the accompanying financial statements and related notes and management explanations. Please classify the fraud risk factors into pressures and opportunities.

Pressures:?

Opportunities:?

Please indicate any potential material misstatements noted during the reading of the financial statements. You may refer to the case information, perform calculations, and make assumptions, if necessary. (The number of spaces given is not indicative of the actual number of instances of material misstatements).

How and where do you believe the client’s financial statements might be susceptible to material misstatement? Identify the specific management assertions which could be violated for each material misstatement identified and explain how.

Provide answers for this question in 10 bullet points.

1. 2. 3. 4. 5. 6. 7. 8. 9. 10.

Expert Answer:

1 Inventories There may be a potential misstatement due to the change in valuation method from average cost to firstin firstout method to recognize additional gross profits of 585 which could lead to ... View the full answer

Auditing and Assurance services an integrated approach

ISBN: 978-0132575959

14th Edition

Authors: Alvin a. arens, Randal j. elder, Mark s. Beasley