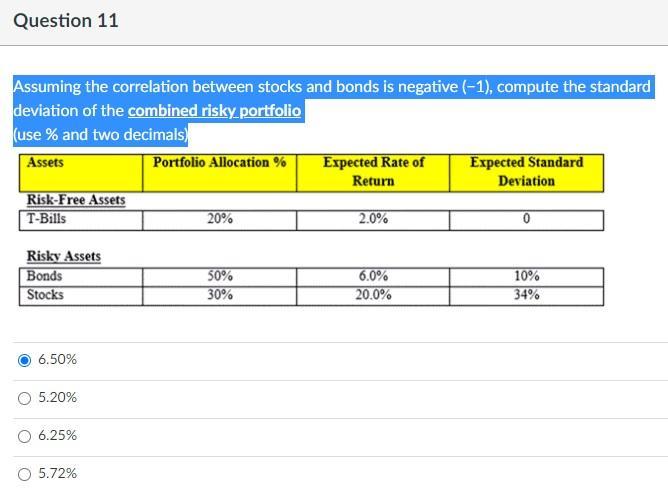

Assuming the correlation between stocks and bonds is negative (1), compute the standard deviation of the combined

Fantastic news! We've Found the answer you've been seeking!

Question:

Assuming the correlation between stocks and bonds is negative (−1), compute the standard deviation of the combined risky portfolio

(use % and two decimals)

Please provide steps in excel

Expert Answer:

Related Book For

Business Statistics in Practice

ISBN: 978-0077404741

6th edition

Authors: Bruce Bowerman, Richard O'Connell

Posted Date: