FREE-CASH-FLOWS-BASED VALUATION. In Problem, we projected financial statements for Wal-Mart Stores, Inc. (Walmart) for Years +1 through

Question:

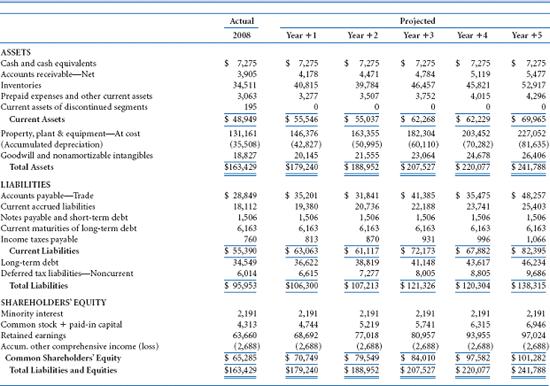

FREE-CASH-FLOWS-BASED VALUATION. In Problem, we projected financial statements for Wal-Mart Stores, Inc. (Walmart) for Years +1 through +5. The data in Exhibits 1–3 (see pages 985–987) include the actual amounts for 2008 and the projected amounts for Year +1 to Year +5 for the income statements, balance sheets, and statements of cash flows for Walmart (in millions).

The market equity beta for Walmart at the end of Year 4 was 0.80. Assume that the risk-free interest rate was 3.5 percent and the market risk premium was 5.0 percent. Walmart had 3,925 million shares outstanding at the end of 2008. At the end of 2008, Walmart’s share price was $46.06.

Required

Part I—Computing Walmart’s Share Value Using Free Cash Flows to Common Equity Shareholders

a. Use the CAPM to compute the required rate of return on common equity capital for Walmart.

b. Beginning with projected net cash flows from operations, derive the projected free cash flows for common equity shareholders for Walmart for Years +1 through +5 based on the projected financial statements. Assume that Walmart uses any change in cash each year for operating liquidity purposes.

c. Project the continuing free cash flow for common equity shareholders in Year +6. Assume that the steady-state long-run growth rate will be 3 percent in Year +6 and beyond. Project that the Year +5 income statement and balance sheet amounts will grow by 3 percent in Year +6; then derive the projected statement of cash flows for Year +6. Derive the projected free cash flow for common equity shareholders in Year +6 from the projected statement of cash flows for Year +6.

d. Using the required rate of return on common equity from Part a as a discount rate, compute the sum of the present value of free cash flows for common equity shareholders for Walmart for Years +1 through +5.

e. Using the required rate of return on common equity from Part a as a discount rate and the long-run growth rate from Part c, compute the continuing value of Walmart as of the start of Year +6 based on Walmart’s continuing free cash flows for common equity shareholders in Year +6 and beyond. After computing continuing value as of the start of Year +6, discount it to present value at the start of Year +1.

f. Compute the value of a share of Walmart common stock. (1) Compute the total sum of the present value of all future free cash flows for equity shareholders (from Parts d and e). (2) Adjust the total sum of the present value using the midyear discounting adjustment factor. (3) Compute the per-share value estimate.

Note: If you worked Problem in Chapter 11 and computed Walmart’s share value using the dividends valuation approach, compare your value estimate from that problem with the value estimate you obtain here. They should be the same.

Part II—Computing Walmart’s Share Value Using Free Cash Flows to All Debt and Equity Stakeholders

g. At the end of 2008, Walmart had $42,218 million in outstanding interest-bearing short-term and long-term debt on the balance sheet and no preferred stock. Assume that the balance sheet value of Walmart’s debt is approximately equal to the market value of the debt. During 2008, Walmart’s income statement included interest expense of $2,184 million. During 2008, Walmart faced an average interest expense of roughly 5.0 percent. Assume that at the start of Year +1, Walmart will continue to incur interest expense of 5.0 percent on debt capital and that Walmart’s average tax rate will be 34.2 percent. Compute the weighted average cost of capital for Walmart as of the start of Year +1.

h. Beginning with projected net cash flows from operations, derive the projected free cash flows for all debt and equity stakeholders for Walmart for Years +1 through +5 based on the projected financial statements.

i. Project the continuing free cash flows for all debt and equity stakeholders in Year +6. Use the projected financial statements for Year +6 from Part c to derive the projected free cash flow for all debt and equity stakeholders in Year +6.

j. Using the weighted average cost of capital from Part g as a discount rate, compute the sum of the present value of free cash flows for all debt and equity stakeholders for Walmart for Years +1 through +5.

k. Using the weighted average cost of capital from Part g as a discount rate and the long-run growth rate from Part c, compute the continuing value of Walmart as of the start of Year +6 based on Walmart’s continuing free cash flows for all debt and equity stakeholders in Year +6 and beyond. After computing continuing value as of the start of Year +6, discount it to present value as of the start of Year +1.

l. Compute the value of a share of Walmart common stock. (1) Compute the total value of Walmart’s net operating assets using the total sum of the present value of free cash flows for all debt and equity stakeholders (from Parts j and k). (2) Subtract the value of outstanding debt to obtain the value of equity. (3) Adjust the present value of equity using the midyear discounting adjustment factor. (4) Compute the per-share value estimate of Walmart’s common equity shares.

Note: Do not be alarmed if your share value estimate from Part f is slightly different from your share value estimate from Part l. The weighted average cost of capital computation in Part g used the weight of equity based on the market price of Walmart’s stock at the end of 2008. The share value estimates from Parts f and l likely differ from the market price, so the weights used to compute the weighted average cost of capital are not internally consistent with the estimated share values.

Part III—Sensitivity Analysis and Recommendation

m. Using the free cash flows to common equity shareholders, recompute the value of Walmart shares under two alternative scenarios. Scenario 1: Assume that Walmart’s long-run growth will be 2 percent, not 3 percent as before, and assume that Walmart’s required rate of return on equity is 1 percentage point higher than the rate you computed using the CAPM in Part a. Scenario 2: Assume that Walmart’s longrun growth will be 4 percent, not 3 percent as before, and assume that Walmart’s required rate of return on equity is 1 percentage point lower than the rate you computed using the CAPM in Part a. To quantify the sensitivity of your share value estimate for Walmart to these variations in growth and discount rates, compare (in percentage terms) your value estimates under these two scenarios with your value estimate from Part f.

n. Using these data at the end of Year 4, what reasonable range of share values would you have expected for Walmart common stock? At that time, what was the market price for Walmart shares relative to this range? What would you have recommended?

Problem

PREPARING AND INTERPRETING FINANCIAL STATEMENT FORECASTS. Wal-Mart Stores, Inc. (Walmart) is the largest retailing firm in the world. Building on a base of discount stores, Walmart has expanded into warehouse clubs and Supercenters, which sell traditional discount store items and grocery products.

Exhibits 4–6 present the financial statements of Walmart for 2006–2008. Exhibits (Case 4.2 in Chapter 4) also present summary financial statements for Walmart, and Exhibit presents selected financial statement ratios for Years 2006–2008. (Note: A few of the amounts presented in Chapter 4 for Walmart differ slightly from the amounts provided here because, for purposes of computing financial analysis ratios, the Chapter 4 data have been adjusted slightly to remove the effects of nonrecurring items such as discontinued operations.)

Required (additional requirements follow on page 862)

a. Design a spreadsheet and prepare a set of financial statement forecasts for Walmart for Year +1 to Year +5 using the assumptions that follow. Project the amounts in the order presented (unless indicated otherwise) beginning with the income statement, then the balance sheet, and then the statement of cash flows. For this portion of the problem, assume that Walmart will exercise its financial flexibility with the cash and cash equivalents account to balance the balance sheet.

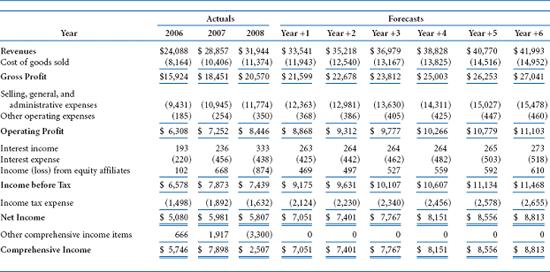

EXHIBIT 1 The Coca-Cola Company Projected implied statements of Cash flows for year+1 through +6 (amounts in millions)

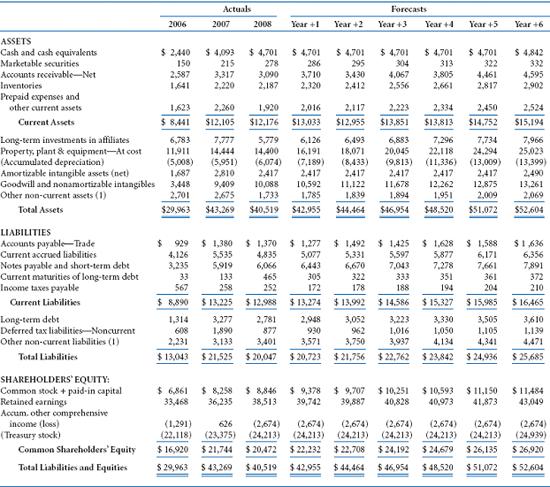

EXHIBIT 2 The Coca-Cola Company Projected implied statements of Cash flows for year+1 through +6 (amounts in millions)

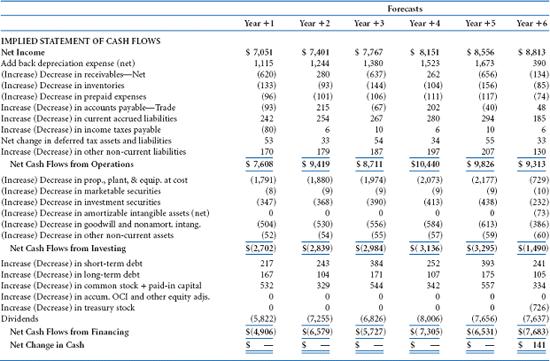

EXHIBIT 3 The Coca-Cola Company Projected implied statements of Cash flows for year+1 through +6 (amounts in millions)

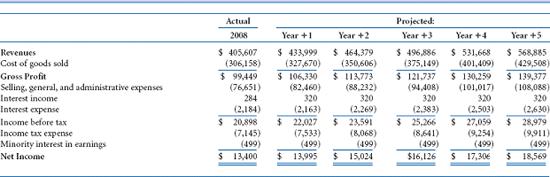

Exhibit 4 Wal-Mart Stores. Inc. Income Statements for 2008 (Actual) and Year +1 through +5 (Projected) (amounts in millions) (Problem)

Exhibit 5 Wal-Mart Stores. Inc. Balance Sheets for 2008 (Actual) and Year +1 through +5 (Projected) (amounts in millions) (Problem)

Exhibit 6 Wal-Mart Stores, Inc. Projected Implied Statements of Cash Flows for Year +1 through +5 (amounts in millions) (Problem)

Expert Answer:

Free Cash Flows based valuation WalMart Stores The market equity beta of WalMart ... View the full answer

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1285190907

8th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw