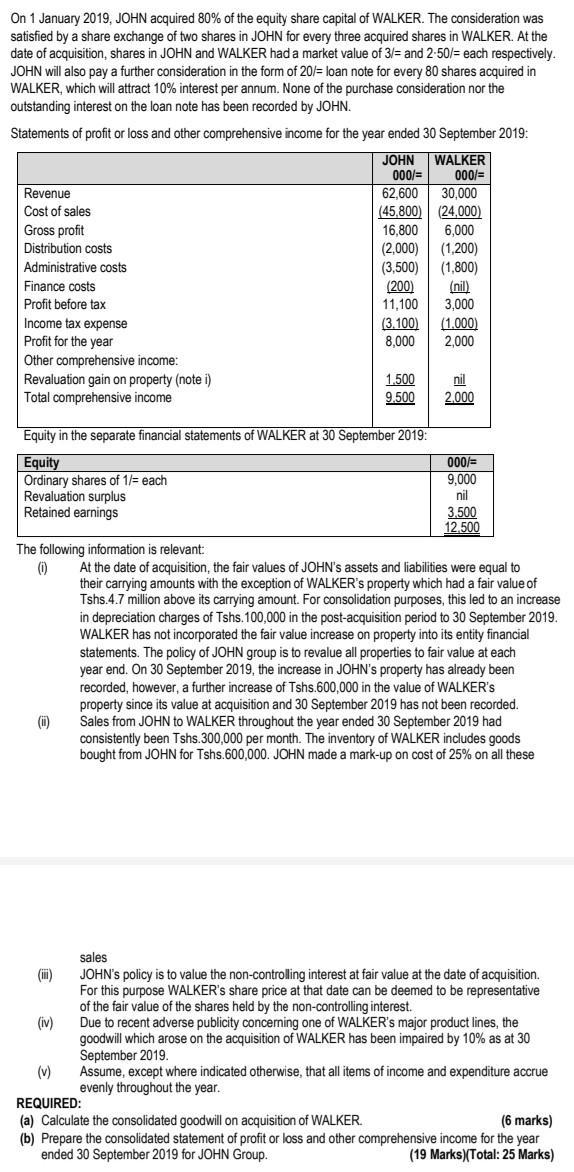

On 1 January 2019, JOHN acquired 80% of the equity share capital of WALKER. The consideration...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

On 1 January 2019, JOHN acquired 80% of the equity share capital of WALKER. The consideration was satisfied by a share exchange of two shares in JOHN for every three acquired shares in WALKER. At the date of acquisition, shares in JOHN and WALKER had a market value of 3/= and 2-50/= each respectively. JOHN will also pay a further consideration in the form of 20/= loan note for every 80 shares acquired in WALKER, which will attract 10% interest per annum. None of the purchase consideration nor the outstanding interest on the loan note has been recorded by JOHN. Statements of profit or loss and other comprehensive income for the year ended 30 September 2019: JOHN WALKER 000/= Revenue Cost of sales Gross profit Distribution costs Administrative costs Finance costs Profit before tax Income tax expense Profit for the year Other comprehensive income: Revaluation gain on property (note i) Total comprehensive income The following information is relevant: (0) (ii) (iii) 000/= (iv) 62,600 30,000 (45,800) (24,000) 16,800 6,000 (2,000) (1,200) (3,500) (1,800) Equity in the separate financial statements of WALKER at 30 September 2019: Equity Ordinary shares of 1/= each Revaluation surplus Retained earnings (200) 11,100 (nil) 3,000 (3.100) (1.000) 8,000 2,000 1.500 9.500 nil 2.000 000/= 9,000 nil 3.500 12.500 At the date of acquisition, the fair values of JOHN's assets and liabilities were equal to their carrying amounts with the exception of WALKER's property which had a fair value of Tshs.4.7 million above its carrying amount. For consolidation purposes, this led to an increase in depreciation charges of Tshs. 100,000 in the post-acquisition period to 30 September 2019. WALKER has not incorporated the fair value increase on property into its entity financial statements. The policy of JOHN group is to revalue all properties to fair value at each year end. On 30 September 2019, the increase in JOHN's property has already been recorded, however, a further increase of Tshs.600,000 in the value of WALKER'S property since its value at acquisition and 30 September 2019 has not been recorded. Sales from JOHN to WALKER throughout the year ended 30 September 2019 had consistently been Tshs.300,000 per month. The inventory of WALKER includes goods bought from JOHN for Tshs.600,000. JOHN made a mark-up on cost of 25% on all these sales JOHN's policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose WALKER's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest. Due to recent adverse publicity concerning one of WALKER's major product lines, the goodwill which arose on the acquisition of WALKER has been impaired by 10% as at 30 September 2019. Assume, except where indicated otherwise, that all items of income and expenditure accrue evenly throughout the year. (v) REQUIRED: (a) Calculate the consolidated goodwill on acquisition of WALKER. (6 marks) (b) Prepare the consolidated statement of profit or loss and other comprehensive income for the year ended 30 September 2019 for JOHN Group. (19 Marks)(Total: 25 Marks) On 1 January 2019, JOHN acquired 80% of the equity share capital of WALKER. The consideration was satisfied by a share exchange of two shares in JOHN for every three acquired shares in WALKER. At the date of acquisition, shares in JOHN and WALKER had a market value of 3/= and 2-50/= each respectively. JOHN will also pay a further consideration in the form of 20/= loan note for every 80 shares acquired in WALKER, which will attract 10% interest per annum. None of the purchase consideration nor the outstanding interest on the loan note has been recorded by JOHN. Statements of profit or loss and other comprehensive income for the year ended 30 September 2019: JOHN WALKER 000/= Revenue Cost of sales Gross profit Distribution costs Administrative costs Finance costs Profit before tax Income tax expense Profit for the year Other comprehensive income: Revaluation gain on property (note i) Total comprehensive income The following information is relevant: (0) (ii) (iii) 000/= (iv) 62,600 30,000 (45,800) (24,000) 16,800 6,000 (2,000) (1,200) (3,500) (1,800) Equity in the separate financial statements of WALKER at 30 September 2019: Equity Ordinary shares of 1/= each Revaluation surplus Retained earnings (200) 11,100 (nil) 3,000 (3.100) (1.000) 8,000 2,000 1.500 9.500 nil 2.000 000/= 9,000 nil 3.500 12.500 At the date of acquisition, the fair values of JOHN's assets and liabilities were equal to their carrying amounts with the exception of WALKER's property which had a fair value of Tshs.4.7 million above its carrying amount. For consolidation purposes, this led to an increase in depreciation charges of Tshs. 100,000 in the post-acquisition period to 30 September 2019. WALKER has not incorporated the fair value increase on property into its entity financial statements. The policy of JOHN group is to revalue all properties to fair value at each year end. On 30 September 2019, the increase in JOHN's property has already been recorded, however, a further increase of Tshs.600,000 in the value of WALKER'S property since its value at acquisition and 30 September 2019 has not been recorded. Sales from JOHN to WALKER throughout the year ended 30 September 2019 had consistently been Tshs.300,000 per month. The inventory of WALKER includes goods bought from JOHN for Tshs.600,000. JOHN made a mark-up on cost of 25% on all these sales JOHN's policy is to value the non-controlling interest at fair value at the date of acquisition. For this purpose WALKER's share price at that date can be deemed to be representative of the fair value of the shares held by the non-controlling interest. Due to recent adverse publicity concerning one of WALKER's major product lines, the goodwill which arose on the acquisition of WALKER has been impaired by 10% as at 30 September 2019. Assume, except where indicated otherwise, that all items of income and expenditure accrue evenly throughout the year. (v) REQUIRED: (a) Calculate the consolidated goodwill on acquisition of WALKER. (6 marks) (b) Prepare the consolidated statement of profit or loss and other comprehensive income for the year ended 30 September 2019 for JOHN Group. (19 Marks)(Total: 25 Marks)

Expert Answer:

Answer rating: 100% (QA)

a Calculation of goodwill on acquisition of WALKER 80 of WALKERs equity share capital 80 x 9000 7200 ... View the full answer

Related Book For

International Financial Reporting A Practical Guide

ISBN: 978-1292200743

6th edition

Authors: Alan Melville

Posted Date:

Students also viewed these accounting questions

-

On 1 January 2019 a company that prepares accounts to 31 December enters into a five-year lease of a machine from a developer. Lease payments are 50,000 per annual, payable at the end of the year....

-

Statement of profit or loss and other comprehensive income Year ended 31 Nine-month Dec-18 period ended 31 Dec-17 Revenue 2,200,228 1,561,138 Cost of sales -1,199,154 -877,354 Gross profit 1,001,074...

-

Prepare a statement of profit or loss and other comprehensive income, and a statement of changes in equity for Sandham for the year ended 31 August 2022 and a statement of financial position at 31...

-

In the context of online marketing communications, briefly explain what viral marketing is. Is it a worth-while pursuit for marketing organizations?

-

Patrick has a PAP with liability limits of $50,000/$100,000/$25,000. Patrick failed to stop at a red light and hit a van. The van sustained damages of $15,000. Three passengers in the van were...

-

Income and education levels are on the rise in many parts of the world. a) How do you think your own post-college boost in income (after you land your first "real" job) will affect your consumption...

-

Leicht Transfer & Storage provides warehousing services and often purchases pallets from Pallet Central. The companies followed a standard practice for documenting these transactions in which Pallet...

-

At December 31, 2013, Walton Company reported the following as plant assets. During 2014, the following selected cash transactions occurred. April 1 Purchased land for $2,200,000. May 1 Sold...

-

Scenario 11:Accountant 11 is a senior accountant. She says: I recommended a wonderful coffee serviceto my audit client, I received a commission from the coffee service company, can I take...

-

The Tastee Bakery Company supplies a bakery product to many supermarkets in a metropolitan area. The company wishes to study the effect of the height of the shelf display employed by the supermarkets...

-

Assume that COMPANY A has a standard deviation of 65%, COMPANY B has a standard deviation of 35% and the correlation between COMPANY A and COMPANY B is 0.0. What is the standard deviation of the...

-

Jave Answer Newton's Law of Gravitation, which we will study soon, is written as F=GmM/R2 where F is the force of attraction, m and M are any two masses, and R is the separation between them. G is...

-

6p Determine the number of atoms in a solid square disc of pure Silicon with sides measuring 6.9 cm and a thickness of 1.6 mm. Assume the atomic weight and density of Si are 0.0280855 g/millimole and...

-

7p The spring constant for a helical coil spring, k, theoretically follows the form shown where d (lower case) is the wire diameter, D (UPPER CASE) is the mean diameter of the coil, na is the number...

-

A 80 kg skier grips a moving rope that is powered by an engine and is pulled at constant speed to the top of a 21 hill. The skier is pulled a distance z = 240 m along the incline and it takes 2.3 min...

-

The diameter of the He atom is approximately 0.10 nm. Calculate the density of the He atom in g/cm (assuming that it is a sphere). Express your answer in grams per cubic centimeter.

-

'Remedies in Judicial Review would not be granted to a mere busybody who is interfering in things which do not concern him.' Critically examine this statement in relation to the concept of Locus...

-

Identify the source of funds within Micro Credit? How does this differ from traditional sources of financing? What internal and external governance mechanisms are in place in Micro Credit?

-

(a) Define the term " goodwill " and distinguish between internally generated goodwill and goodwill acquired in a business combination. (b) Identify the main features of goodwill which distinguish it...

-

A company adopts international standards for the first time when preparing its financial statements for the year to 30 June 2018. These financial statements show comparative figures for the previous...

-

(a) Define the term "investment property". Explain why it is not generally appropriate to charge depreciation in relation to such a property. (b) Give three examples of properties (land or buildings)...

-

Describe a commercial banks assets and liabilities.

-

Financial intermediaries can manage the problems of adverse selection and moral hazard. a. They can reduce adverse selection by collecting information on borrowers and screening them to check their...

-

Define bank capital and key measures of bank profits and returns.

Study smarter with the SolutionInn App