Part A Reflection You have been supplied with Global Motor Manufacturers Australia Pty Ltd. Accounting documents as

Question:

Part A Reflection

You have been supplied with Global Motor Manufacturers Australia Pty Ltd. Accounting documents as part of an Audit Virtual Experience Program.

* Trial Balance (Appendix A)

* Variance Analysis (Appendix B)

* Meeting Minutes (Appendix C)

Write a reflective essay (700 words) about your experience analysing the appendices, addressing three key questions:

- Comment on the auditor’s techniques/approaches to the risk assessment phase of the audit.

- What did you learn from the program about the risk assessment phase of an audit?

- Suggest techniques/approaches/areas where the auditor could do better with the risk assessment phase? You address this question by referring to the learning materials and at least two academic articles on the risk assessment.

Please use an essay format for your discussion. Textbooks such as Moroney, et al. (2020), or websites do not qualify as an academic article. APA 6th is required with an appropriate reference list.

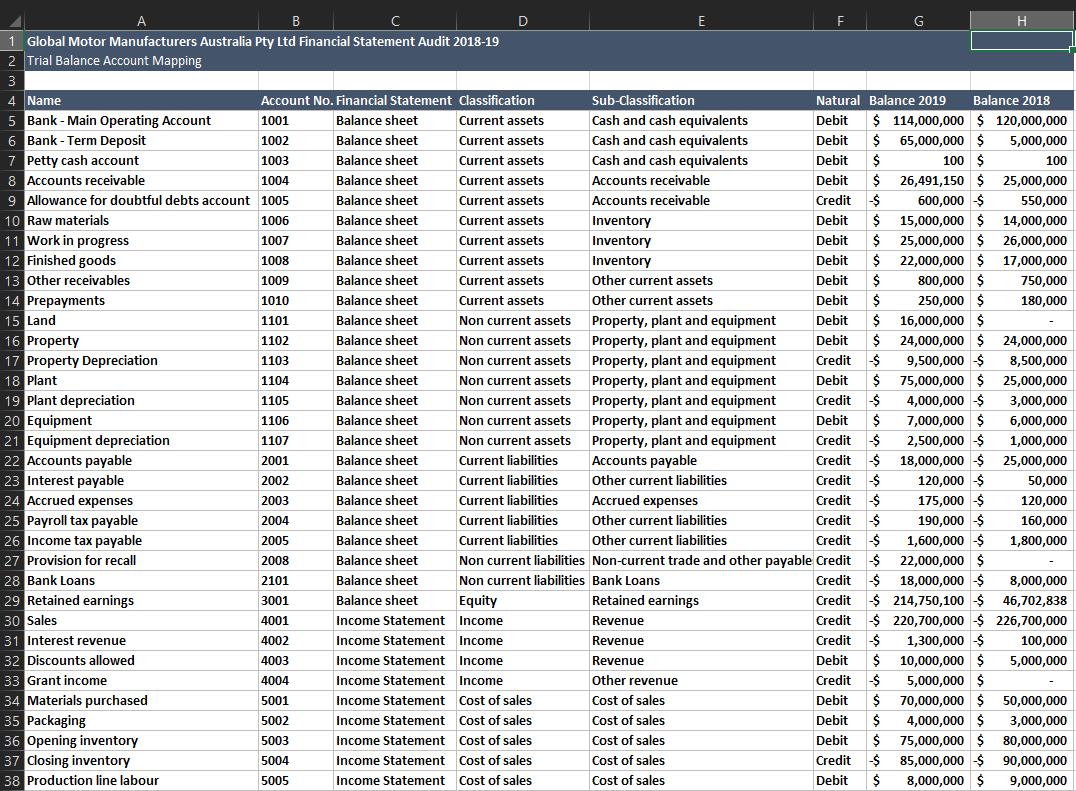

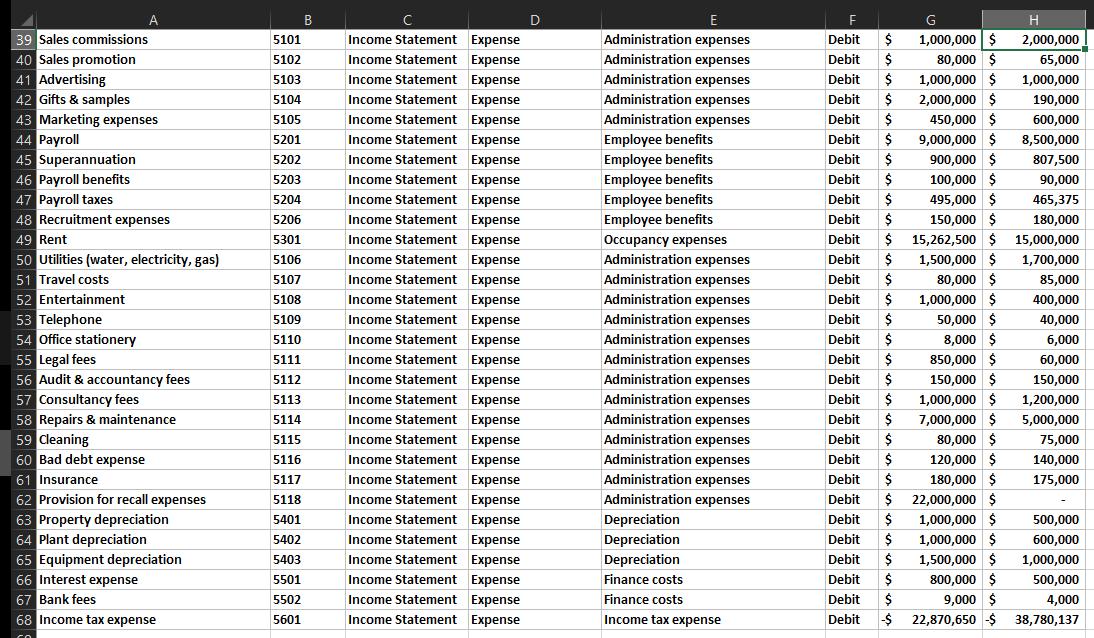

APPENDIX A - TRIAL BALANCE, MAPPING (PART A)

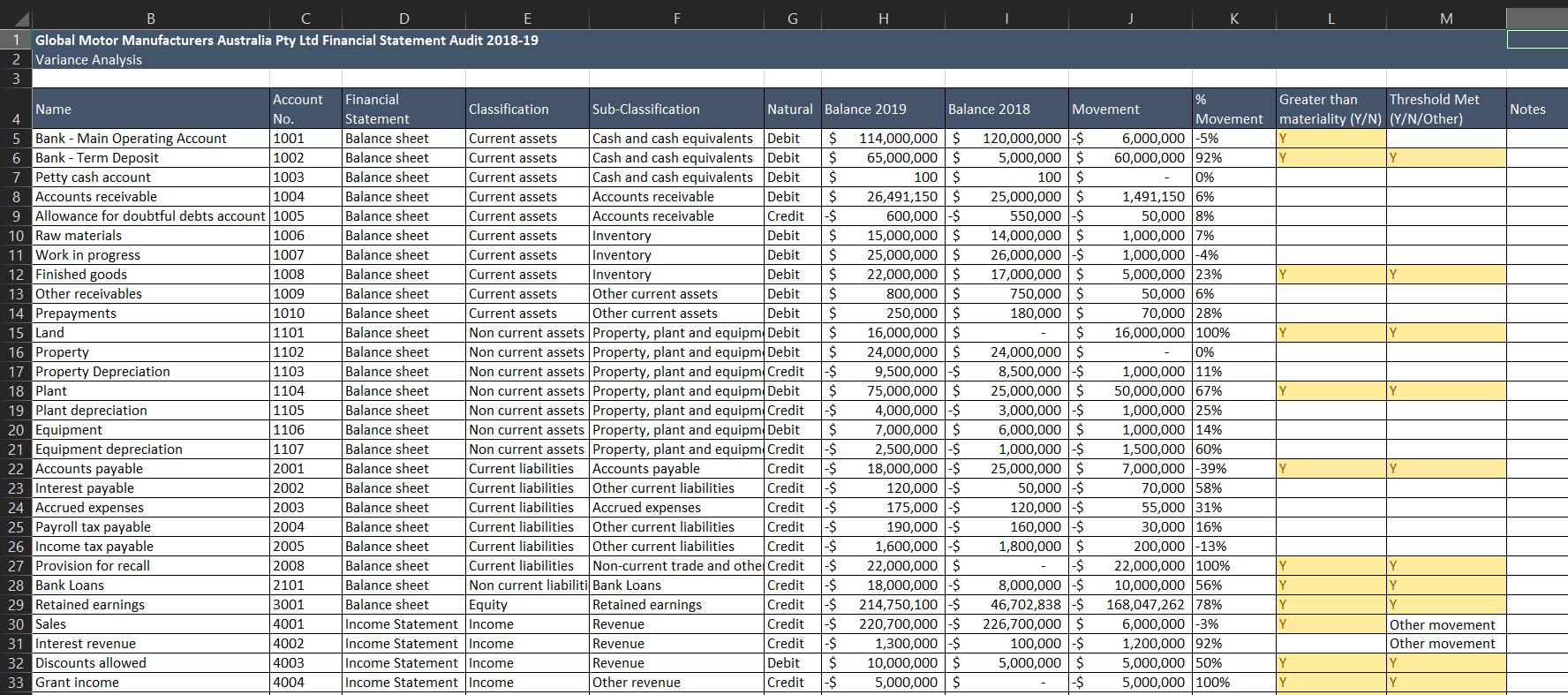

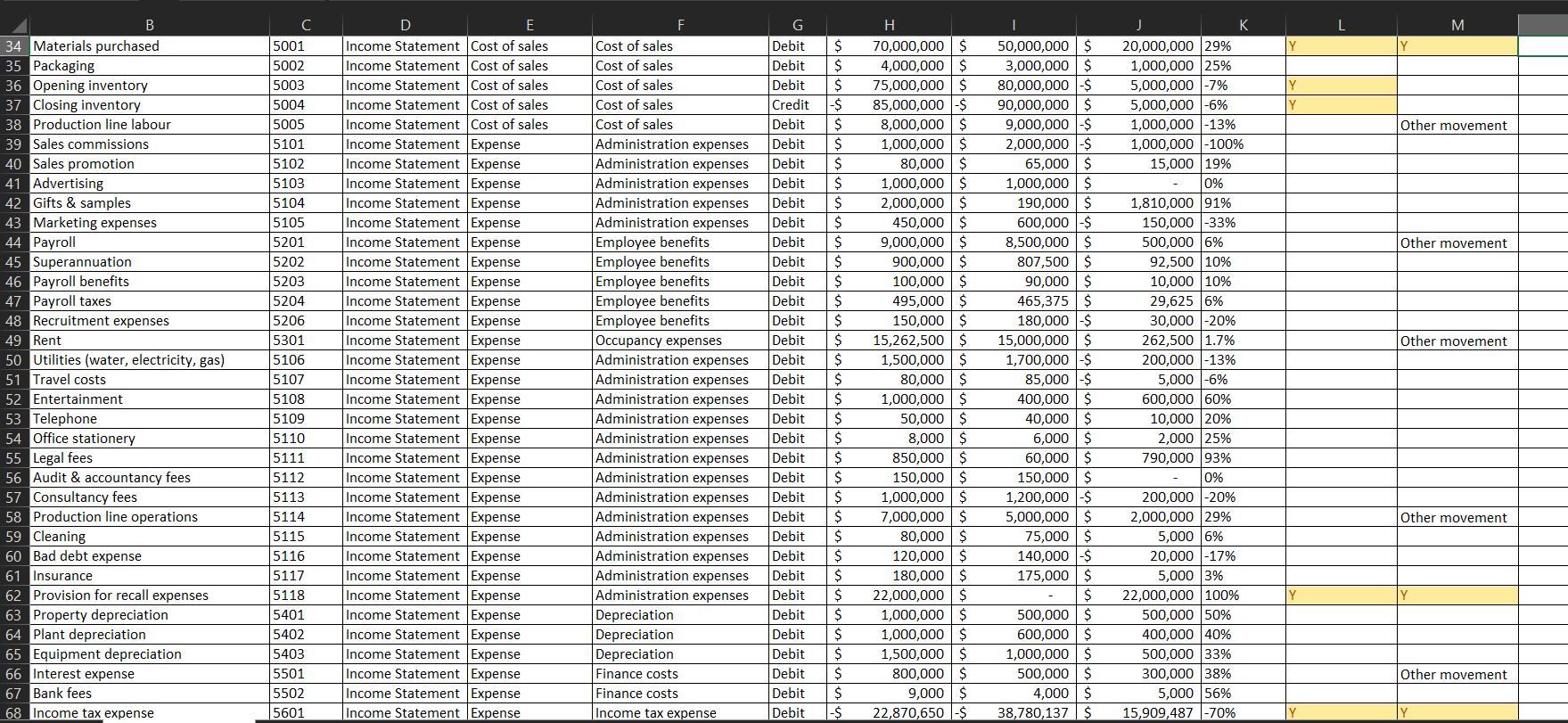

APPENDIX B – VARIANCE ANALYSIS (PART A)

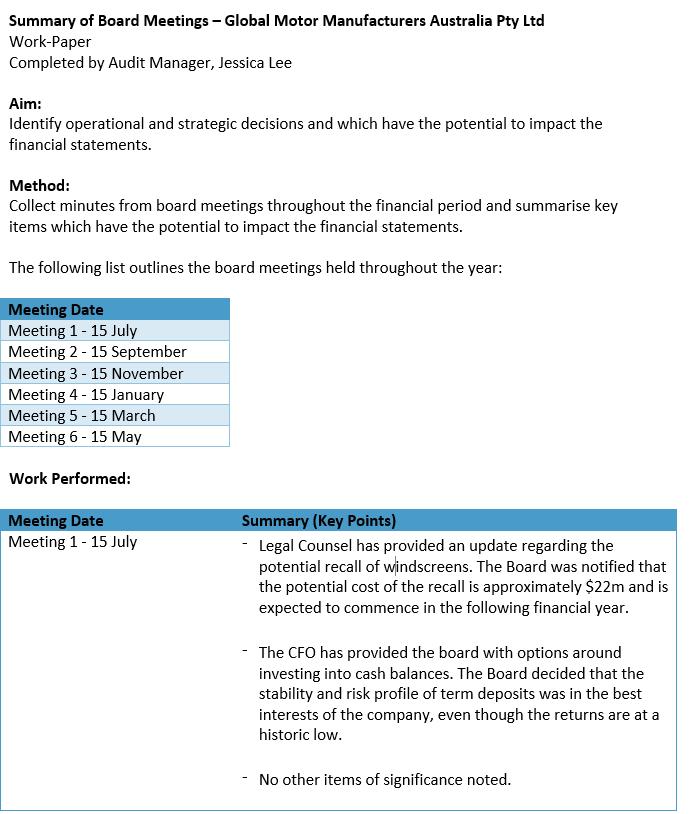

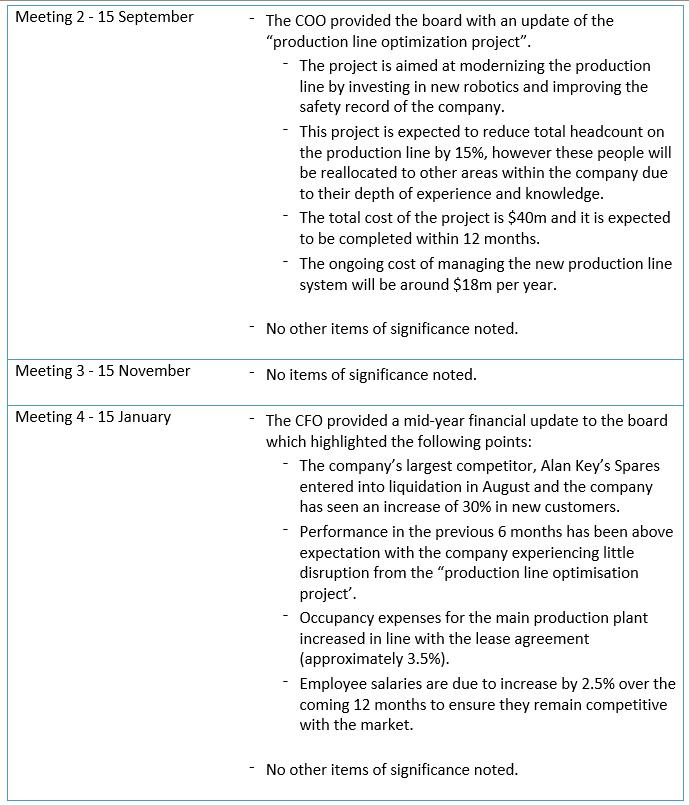

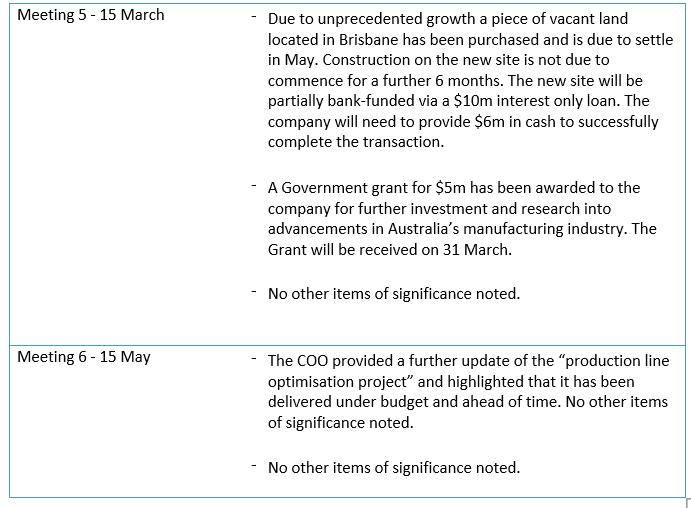

APPENDIX C – MEETING MINUTES (PART A)

Expert Answer:

Title A Reflective Analysis of the Risk Assessment Phase in the Audit of Global Motor Manufacturers Australia Pty Ltd Introduction The audit process is a critical component of ensuring the integrity o... View the full answer

Auditing a business risk appraoch

ISBN: 978-0324375589

6th Edition

Authors: larry e. rittenberg, bradley j. schwieger, karla m. johnston