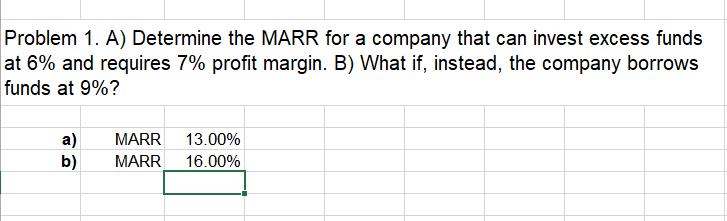

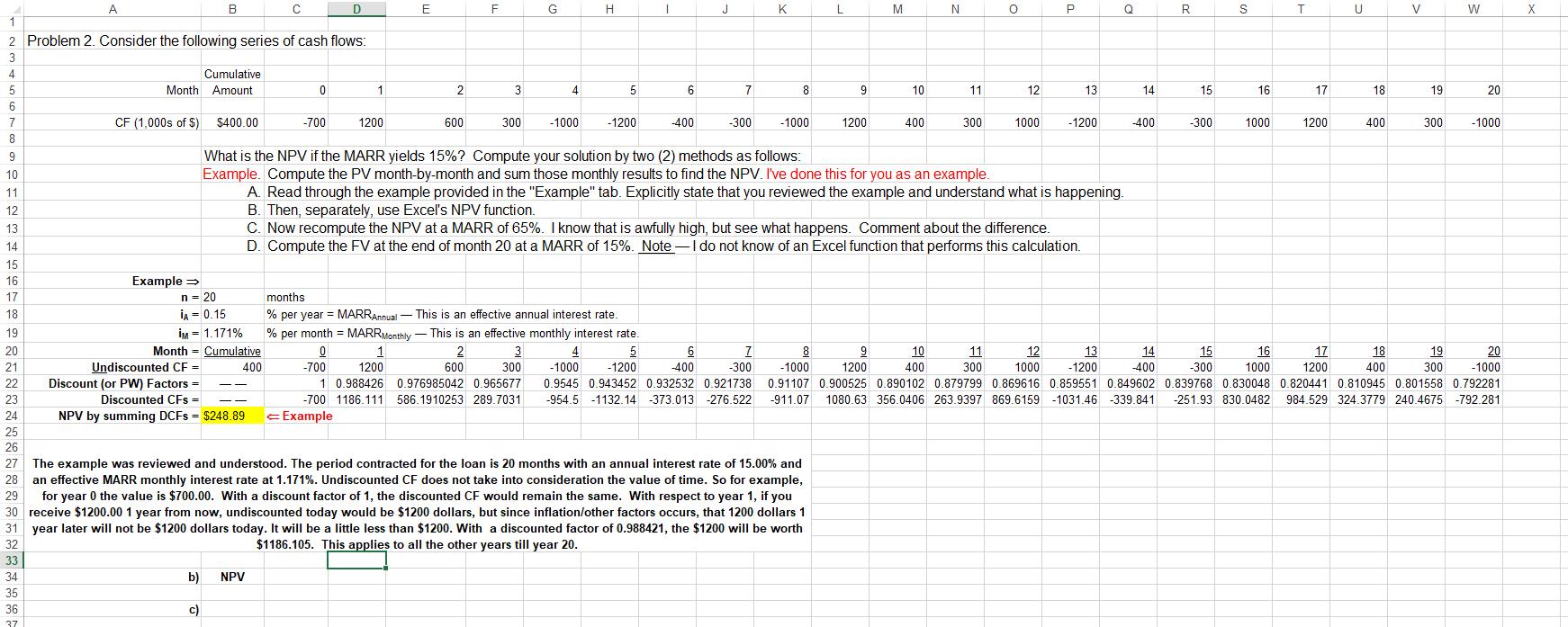

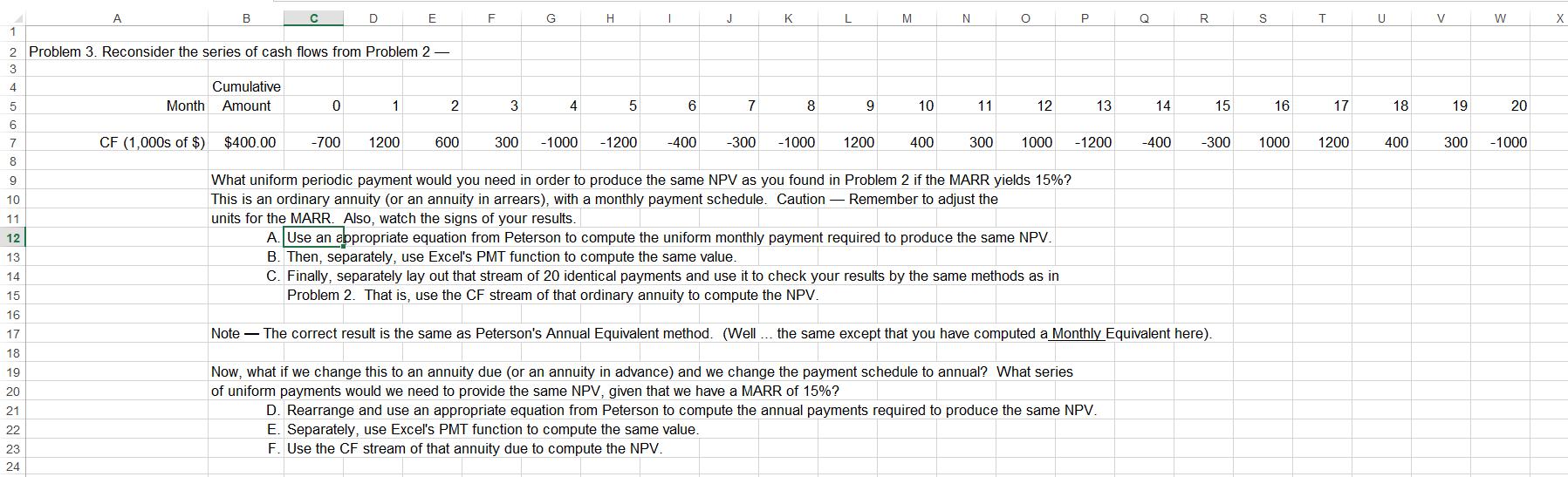

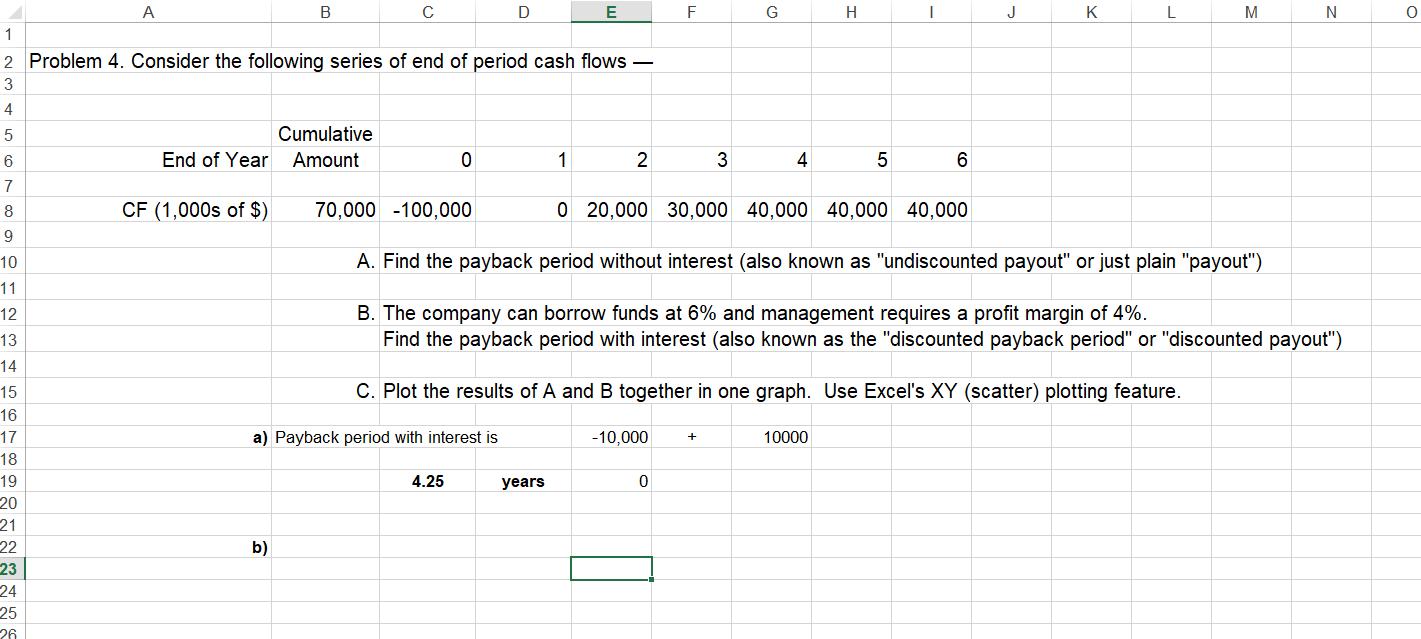

Problem 1. A) Determine the MARR for a company that can invest excess funds at 6%...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Problem 1. A) Determine the MARR for a company that can invest excess funds at 6% and requires 7% profit margin. B) What if, instead, the company borrows funds at 9%? a) MARR 13.00% b) MARR 16.00% 4 5 6 7 8 9 10 11 12 13 14 1 2 Problem 2. Consider the following series of cash flows: 3 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 32 33 A 34 35 36 37 B Example → C —— 0 b) NPV c) D -700 n = 20 IA = 0.15 İM = 1.171% Month Cumulative Undiscounted CF = 400 Discount (or PW) Factors = Discounted CFs = NPV by summing DCFs = $248.89 = Example 1 E 1200 2 F 600 Cumulative Month Amount CF (1,000s of $) $400.00 What is the NPV if the MARR yields 15%? Compute your solution by two (2) methods as follows: Example. Compute the PV month-by-month and sum those monthly results to find the NPV. I've done this for you as an example. A. Read through the example provided in the "Example" tab. Explicitly state that you reviewed the example and understand what is happening. B. Then, separately, use Excel's NPV function. 3 G 300 4 H -1000 5 I -1200 6 J -400 7 -300 K months % per year = MARRAnnual - This is an effective annual interest rate. % per month = MARR Monthly This is an effective monthly interest rate. 0 -700 1 1200 2 600 3 300 4 5 6 7 -1000 -1200 -400 -300 1 0.988426 0.976985042 0.965677 0.9545 0.943452 0.932532 0.921738 -700 1186.111 586.1910253 289.7031 -954.5 -1132.14 -373.013 -276.522 8 The example was reviewed and understood. The period contracted for the loan is 20 months with an annual interest rate of 15.00% and an effective MARR monthly interest rate at 1.171%. Undiscounted CF does not take into consideration the value of time. So for example, for year 0 the value is $700.00. With a discount factor of 1, the discounted CF would remain the same. With respect to year 1, if you 30 receive $1200.00 1 year from now, undiscounted today would be $1200 dollars, but since inflation/other factors occurs, that 1200 dollars 1 31 year later will not be $1200 dollars today. It will be a little less than $1200. With a discounted factor of 0.988421, the $1200 will be worth $1186.105. This applies to all the other years till year 20. -1000 L 9 M 1200 10 400 N 11 10 400 300 O C. Now recompute the NPV at a MARR of 65%. I know that is awfully high, but see what happens. Comment about the difference. D. Compute the FV at the end of month 20 at a MARR of 15%. Note- I do not know of an Excel function that performs this calculation. 12 11 300 1000 P 12 1000 13 -1200 Q 14 -400 R 14 -400 15 -300 S 15 -300 16 1000 T 16 1000 17 1200 U 17 1200 18 19 20 13 -1200 300 -1000 8 9 -1000 1200 0.91107 0.900525 0.890102 0.879799 0.869616 0.859551 0.849602 0.839768 0.830048 0.820441 0.810945 0.801558 0.792281 -911.07 1080.63 356.0406 263.9397 869.6159 -1031.46 -339.841 -251.93 830.0482 984.529 324.3779 240.4675 -792.281 400 V 18 400 19 300 W 20 -1000 X 4 5 6 7 8 A 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 B 1 2 Problem 3. Reconsider the series of cash flows from Problem 2- - 3 Cumulative Month Amount D 0 - 1 E 1200 2 F 600 3 G 4 300 -1000 H 5 -1200 I 6 J 7 K 8 -400 -300 -1000 L 9 CF (1,000s of $) $400.00 -700 What uniform periodic payment would you need in order to produce the same NPV as you found in Problem 2 if the MARR yields 15%? This is an ordinary annuity (or an annuity in arrears), with a monthly payment schedule. Caution - Remember to adjust the units for the MARR. Also, watch the signs of your results. A. Use an appropriate equation from Peterson to compute the uniform monthly payment required to produce the same NPV. B. Then, separately, use Excel's PMT function to compute the same value. C. Finally, separately lay out that stream of 20 identical payments and use it to check your results by the same methods as in Problem 2. That is, use the CF stream of that ordinary annuity to compute the NPV. 1200 M 10 400 N 11 O 12 300 1000 P 13 -1200 14 Now, what if we change this to an annuity due (or an annuity in advance) and we change the payment schedule to annual? What series of uniform payments would we need to provide the same NPV, given that we have a MARR of 15%? D. Rearrange and use an appropriate equation from Peterson to compute the annual payments required to produce the same NPV. E. Separately, use Excel's PMT function to compute the same value. F. Use the CF stream of that annuity due to compute the NPV. R Note The correct result is the same as Peterson's Annual Equivalent method. (Well... the same except that you have computed a Monthly Equivalent here). 15 -400 -300 S 16 1000 T 17 1200 U 18 400 V 19 W 20 300 -1000 X 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 A 22 23 24 25 26 1 2 Problem 4. Consider the following series of end of period cash flows - 3 B Cumulative End of Year Amount CF (1,000s of $) C b) 0 70,000 -100,000 D a) Payback period with interest 4.25 E 1 years 2 F -10,000 3 0 G 4 + H 0 20,000 30,000 40,000 40,000 40,000 5 - C. Plot the results of A and B together in one graph. Use Excel's XY (scatter) plotting feature. 10000 6 A. Find the payback period without interest (also known as "undiscounted payout" or just plain "payout") B. The company can borrow funds at 6% and management requires a profit margin of 4%. Find the payback period with interest (also known as the "discounted payback period" or "discounted payout") J K L M N O 4 5 6 7 8 9 10 A 11 12 B C D E F G H J K L M 1 2 Problem 5. Your company buys a truck for $17,000. To make this purchase, your company takes a loan at 11% APR for 60 months. 3 What schedule of monthly principal, interest and total payments must your company make, month-by-month and cumulative, to service the loan over its life? Provide the amortization schedule (using excel functions or A. equations from Peterson). N If your company had taken the loan for only 48 months instead of the 60 months, what would be the differences in the monthly total payment and the cumulative interest payments compared with the 60 month loan that you actually got? Provide the amortization schedule (using excel functions or equations from B. Peterson). O H Problem 1. A) Determine the MARR for a company that can invest excess funds at 6% and requires 7% profit margin. B) What if, instead, the company borrows funds at 9%? a) MARR 13.00% b) MARR 16.00% 4 5 6 7 8 9 10 11 12 13 14 1 2 Problem 2. Consider the following series of cash flows: 3 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 32 33 A 34 35 36 37 B Example → C —— 0 b) NPV c) D -700 n = 20 IA = 0.15 İM = 1.171% Month Cumulative Undiscounted CF = 400 Discount (or PW) Factors = Discounted CFs = NPV by summing DCFs = $248.89 = Example 1 E 1200 2 F 600 Cumulative Month Amount CF (1,000s of $) $400.00 What is the NPV if the MARR yields 15%? Compute your solution by two (2) methods as follows: Example. Compute the PV month-by-month and sum those monthly results to find the NPV. I've done this for you as an example. A. Read through the example provided in the "Example" tab. Explicitly state that you reviewed the example and understand what is happening. B. Then, separately, use Excel's NPV function. 3 G 300 4 H -1000 5 I -1200 6 J -400 7 -300 K months % per year = MARRAnnual - This is an effective annual interest rate. % per month = MARR Monthly This is an effective monthly interest rate. 0 -700 1 1200 2 600 3 300 4 5 6 7 -1000 -1200 -400 -300 1 0.988426 0.976985042 0.965677 0.9545 0.943452 0.932532 0.921738 -700 1186.111 586.1910253 289.7031 -954.5 -1132.14 -373.013 -276.522 8 The example was reviewed and understood. The period contracted for the loan is 20 months with an annual interest rate of 15.00% and an effective MARR monthly interest rate at 1.171%. Undiscounted CF does not take into consideration the value of time. So for example, for year 0 the value is $700.00. With a discount factor of 1, the discounted CF would remain the same. With respect to year 1, if you 30 receive $1200.00 1 year from now, undiscounted today would be $1200 dollars, but since inflation/other factors occurs, that 1200 dollars 1 31 year later will not be $1200 dollars today. It will be a little less than $1200. With a discounted factor of 0.988421, the $1200 will be worth $1186.105. This applies to all the other years till year 20. -1000 L 9 M 1200 10 400 N 11 10 400 300 O C. Now recompute the NPV at a MARR of 65%. I know that is awfully high, but see what happens. Comment about the difference. D. Compute the FV at the end of month 20 at a MARR of 15%. Note- I do not know of an Excel function that performs this calculation. 12 11 300 1000 P 12 1000 13 -1200 Q 14 -400 R 14 -400 15 -300 S 15 -300 16 1000 T 16 1000 17 1200 U 17 1200 18 19 20 13 -1200 300 -1000 8 9 -1000 1200 0.91107 0.900525 0.890102 0.879799 0.869616 0.859551 0.849602 0.839768 0.830048 0.820441 0.810945 0.801558 0.792281 -911.07 1080.63 356.0406 263.9397 869.6159 -1031.46 -339.841 -251.93 830.0482 984.529 324.3779 240.4675 -792.281 400 V 18 400 19 300 W 20 -1000 X 4 5 6 7 8 A 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 B 1 2 Problem 3. Reconsider the series of cash flows from Problem 2- - 3 Cumulative Month Amount D 0 - 1 E 1200 2 F 600 3 G 4 300 -1000 H 5 -1200 I 6 J 7 K 8 -400 -300 -1000 L 9 CF (1,000s of $) $400.00 -700 What uniform periodic payment would you need in order to produce the same NPV as you found in Problem 2 if the MARR yields 15%? This is an ordinary annuity (or an annuity in arrears), with a monthly payment schedule. Caution - Remember to adjust the units for the MARR. Also, watch the signs of your results. A. Use an appropriate equation from Peterson to compute the uniform monthly payment required to produce the same NPV. B. Then, separately, use Excel's PMT function to compute the same value. C. Finally, separately lay out that stream of 20 identical payments and use it to check your results by the same methods as in Problem 2. That is, use the CF stream of that ordinary annuity to compute the NPV. 1200 M 10 400 N 11 O 12 300 1000 P 13 -1200 14 Now, what if we change this to an annuity due (or an annuity in advance) and we change the payment schedule to annual? What series of uniform payments would we need to provide the same NPV, given that we have a MARR of 15%? D. Rearrange and use an appropriate equation from Peterson to compute the annual payments required to produce the same NPV. E. Separately, use Excel's PMT function to compute the same value. F. Use the CF stream of that annuity due to compute the NPV. R Note The correct result is the same as Peterson's Annual Equivalent method. (Well... the same except that you have computed a Monthly Equivalent here). 15 -400 -300 S 16 1000 T 17 1200 U 18 400 V 19 W 20 300 -1000 X 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 A 22 23 24 25 26 1 2 Problem 4. Consider the following series of end of period cash flows - 3 B Cumulative End of Year Amount CF (1,000s of $) C b) 0 70,000 -100,000 D a) Payback period with interest 4.25 E 1 years 2 F -10,000 3 0 G 4 + H 0 20,000 30,000 40,000 40,000 40,000 5 - C. Plot the results of A and B together in one graph. Use Excel's XY (scatter) plotting feature. 10000 6 A. Find the payback period without interest (also known as "undiscounted payout" or just plain "payout") B. The company can borrow funds at 6% and management requires a profit margin of 4%. Find the payback period with interest (also known as the "discounted payback period" or "discounted payout") J K L M N O 4 5 6 7 8 9 10 A 11 12 B C D E F G H J K L M 1 2 Problem 5. Your company buys a truck for $17,000. To make this purchase, your company takes a loan at 11% APR for 60 months. 3 What schedule of monthly principal, interest and total payments must your company make, month-by-month and cumulative, to service the loan over its life? Provide the amortization schedule (using excel functions or A. equations from Peterson). N If your company had taken the loan for only 48 months instead of the 60 months, what would be the differences in the monthly total payment and the cumulative interest payments compared with the 60 month loan that you actually got? Provide the amortization schedule (using excel functions or equations from B. Peterson). O H Problem 1. A) Determine the MARR for a company that can invest excess funds at 6% and requires 7% profit margin. B) What if, instead, the company borrows funds at 9%? a) MARR 13.00% b) MARR 16.00% 4 5 6 7 8 9 10 11 12 13 14 1 2 Problem 2. Consider the following series of cash flows: 3 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 32 33 A 34 35 36 37 B Example → C —— 0 b) NPV c) D -700 n = 20 IA = 0.15 İM = 1.171% Month Cumulative Undiscounted CF = 400 Discount (or PW) Factors = Discounted CFs = NPV by summing DCFs = $248.89 = Example 1 E 1200 2 F 600 Cumulative Month Amount CF (1,000s of $) $400.00 What is the NPV if the MARR yields 15%? Compute your solution by two (2) methods as follows: Example. Compute the PV month-by-month and sum those monthly results to find the NPV. I've done this for you as an example. A. Read through the example provided in the "Example" tab. Explicitly state that you reviewed the example and understand what is happening. B. Then, separately, use Excel's NPV function. 3 G 300 4 H -1000 5 I -1200 6 J -400 7 -300 K months % per year = MARRAnnual - This is an effective annual interest rate. % per month = MARR Monthly This is an effective monthly interest rate. 0 -700 1 1200 2 600 3 300 4 5 6 7 -1000 -1200 -400 -300 1 0.988426 0.976985042 0.965677 0.9545 0.943452 0.932532 0.921738 -700 1186.111 586.1910253 289.7031 -954.5 -1132.14 -373.013 -276.522 8 The example was reviewed and understood. The period contracted for the loan is 20 months with an annual interest rate of 15.00% and an effective MARR monthly interest rate at 1.171%. Undiscounted CF does not take into consideration the value of time. So for example, for year 0 the value is $700.00. With a discount factor of 1, the discounted CF would remain the same. With respect to year 1, if you 30 receive $1200.00 1 year from now, undiscounted today would be $1200 dollars, but since inflation/other factors occurs, that 1200 dollars 1 31 year later will not be $1200 dollars today. It will be a little less than $1200. With a discounted factor of 0.988421, the $1200 will be worth $1186.105. This applies to all the other years till year 20. -1000 L 9 M 1200 10 400 N 11 10 400 300 O C. Now recompute the NPV at a MARR of 65%. I know that is awfully high, but see what happens. Comment about the difference. D. Compute the FV at the end of month 20 at a MARR of 15%. Note- I do not know of an Excel function that performs this calculation. 12 11 300 1000 P 12 1000 13 -1200 Q 14 -400 R 14 -400 15 -300 S 15 -300 16 1000 T 16 1000 17 1200 U 17 1200 18 19 20 13 -1200 300 -1000 8 9 -1000 1200 0.91107 0.900525 0.890102 0.879799 0.869616 0.859551 0.849602 0.839768 0.830048 0.820441 0.810945 0.801558 0.792281 -911.07 1080.63 356.0406 263.9397 869.6159 -1031.46 -339.841 -251.93 830.0482 984.529 324.3779 240.4675 -792.281 400 V 18 400 19 300 W 20 -1000 X 4 5 6 7 8 A 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 B 1 2 Problem 3. Reconsider the series of cash flows from Problem 2- - 3 Cumulative Month Amount D 0 - 1 E 1200 2 F 600 3 G 4 300 -1000 H 5 -1200 I 6 J 7 K 8 -400 -300 -1000 L 9 CF (1,000s of $) $400.00 -700 What uniform periodic payment would you need in order to produce the same NPV as you found in Problem 2 if the MARR yields 15%? This is an ordinary annuity (or an annuity in arrears), with a monthly payment schedule. Caution - Remember to adjust the units for the MARR. Also, watch the signs of your results. A. Use an appropriate equation from Peterson to compute the uniform monthly payment required to produce the same NPV. B. Then, separately, use Excel's PMT function to compute the same value. C. Finally, separately lay out that stream of 20 identical payments and use it to check your results by the same methods as in Problem 2. That is, use the CF stream of that ordinary annuity to compute the NPV. 1200 M 10 400 N 11 O 12 300 1000 P 13 -1200 14 Now, what if we change this to an annuity due (or an annuity in advance) and we change the payment schedule to annual? What series of uniform payments would we need to provide the same NPV, given that we have a MARR of 15%? D. Rearrange and use an appropriate equation from Peterson to compute the annual payments required to produce the same NPV. E. Separately, use Excel's PMT function to compute the same value. F. Use the CF stream of that annuity due to compute the NPV. R Note The correct result is the same as Peterson's Annual Equivalent method. (Well... the same except that you have computed a Monthly Equivalent here). 15 -400 -300 S 16 1000 T 17 1200 U 18 400 V 19 W 20 300 -1000 X 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 A 22 23 24 25 26 1 2 Problem 4. Consider the following series of end of period cash flows - 3 B Cumulative End of Year Amount CF (1,000s of $) C b) 0 70,000 -100,000 D a) Payback period with interest 4.25 E 1 years 2 F -10,000 3 0 G 4 + H 0 20,000 30,000 40,000 40,000 40,000 5 - C. Plot the results of A and B together in one graph. Use Excel's XY (scatter) plotting feature. 10000 6 A. Find the payback period without interest (also known as "undiscounted payout" or just plain "payout") B. The company can borrow funds at 6% and management requires a profit margin of 4%. Find the payback period with interest (also known as the "discounted payback period" or "discounted payout") J K L M N O 4 5 6 7 8 9 10 A 11 12 B C D E F G H J K L M 1 2 Problem 5. Your company buys a truck for $17,000. To make this purchase, your company takes a loan at 11% APR for 60 months. 3 What schedule of monthly principal, interest and total payments must your company make, month-by-month and cumulative, to service the loan over its life? Provide the amortization schedule (using excel functions or A. equations from Peterson). N If your company had taken the loan for only 48 months instead of the 60 months, what would be the differences in the monthly total payment and the cumulative interest payments compared with the 60 month loan that you actually got? Provide the amortization schedule (using excel functions or equations from B. Peterson). O H Problem 1. A) Determine the MARR for a company that can invest excess funds at 6% and requires 7% profit margin. B) What if, instead, the company borrows funds at 9%? a) MARR 13.00% b) MARR 16.00% 4 5 6 7 8 9 10 11 12 13 14 1 2 Problem 2. Consider the following series of cash flows: 3 15 16 17 18 19 20 21 22 23 24 25 26 27 28 29 32 33 A 34 35 36 37 B Example → C —— 0 b) NPV c) D -700 n = 20 IA = 0.15 İM = 1.171% Month Cumulative Undiscounted CF = 400 Discount (or PW) Factors = Discounted CFs = NPV by summing DCFs = $248.89 = Example 1 E 1200 2 F 600 Cumulative Month Amount CF (1,000s of $) $400.00 What is the NPV if the MARR yields 15%? Compute your solution by two (2) methods as follows: Example. Compute the PV month-by-month and sum those monthly results to find the NPV. I've done this for you as an example. A. Read through the example provided in the "Example" tab. Explicitly state that you reviewed the example and understand what is happening. B. Then, separately, use Excel's NPV function. 3 G 300 4 H -1000 5 I -1200 6 J -400 7 -300 K months % per year = MARRAnnual - This is an effective annual interest rate. % per month = MARR Monthly This is an effective monthly interest rate. 0 -700 1 1200 2 600 3 300 4 5 6 7 -1000 -1200 -400 -300 1 0.988426 0.976985042 0.965677 0.9545 0.943452 0.932532 0.921738 -700 1186.111 586.1910253 289.7031 -954.5 -1132.14 -373.013 -276.522 8 The example was reviewed and understood. The period contracted for the loan is 20 months with an annual interest rate of 15.00% and an effective MARR monthly interest rate at 1.171%. Undiscounted CF does not take into consideration the value of time. So for example, for year 0 the value is $700.00. With a discount factor of 1, the discounted CF would remain the same. With respect to year 1, if you 30 receive $1200.00 1 year from now, undiscounted today would be $1200 dollars, but since inflation/other factors occurs, that 1200 dollars 1 31 year later will not be $1200 dollars today. It will be a little less than $1200. With a discounted factor of 0.988421, the $1200 will be worth $1186.105. This applies to all the other years till year 20. -1000 L 9 M 1200 10 400 N 11 10 400 300 O C. Now recompute the NPV at a MARR of 65%. I know that is awfully high, but see what happens. Comment about the difference. D. Compute the FV at the end of month 20 at a MARR of 15%. Note- I do not know of an Excel function that performs this calculation. 12 11 300 1000 P 12 1000 13 -1200 Q 14 -400 R 14 -400 15 -300 S 15 -300 16 1000 T 16 1000 17 1200 U 17 1200 18 19 20 13 -1200 300 -1000 8 9 -1000 1200 0.91107 0.900525 0.890102 0.879799 0.869616 0.859551 0.849602 0.839768 0.830048 0.820441 0.810945 0.801558 0.792281 -911.07 1080.63 356.0406 263.9397 869.6159 -1031.46 -339.841 -251.93 830.0482 984.529 324.3779 240.4675 -792.281 400 V 18 400 19 300 W 20 -1000 X 4 5 6 7 8 A 9 10 11 12 13 14 15 16 17 18 19 20 21 22 23 24 B 1 2 Problem 3. Reconsider the series of cash flows from Problem 2- - 3 Cumulative Month Amount D 0 - 1 E 1200 2 F 600 3 G 4 300 -1000 H 5 -1200 I 6 J 7 K 8 -400 -300 -1000 L 9 CF (1,000s of $) $400.00 -700 What uniform periodic payment would you need in order to produce the same NPV as you found in Problem 2 if the MARR yields 15%? This is an ordinary annuity (or an annuity in arrears), with a monthly payment schedule. Caution - Remember to adjust the units for the MARR. Also, watch the signs of your results. A. Use an appropriate equation from Peterson to compute the uniform monthly payment required to produce the same NPV. B. Then, separately, use Excel's PMT function to compute the same value. C. Finally, separately lay out that stream of 20 identical payments and use it to check your results by the same methods as in Problem 2. That is, use the CF stream of that ordinary annuity to compute the NPV. 1200 M 10 400 N 11 O 12 300 1000 P 13 -1200 14 Now, what if we change this to an annuity due (or an annuity in advance) and we change the payment schedule to annual? What series of uniform payments would we need to provide the same NPV, given that we have a MARR of 15%? D. Rearrange and use an appropriate equation from Peterson to compute the annual payments required to produce the same NPV. E. Separately, use Excel's PMT function to compute the same value. F. Use the CF stream of that annuity due to compute the NPV. R Note The correct result is the same as Peterson's Annual Equivalent method. (Well... the same except that you have computed a Monthly Equivalent here). 15 -400 -300 S 16 1000 T 17 1200 U 18 400 V 19 W 20 300 -1000 X 4 5 6 7 8 9 10 11 12 13 14 15 16 17 18 19 20 21 A 22 23 24 25 26 1 2 Problem 4. Consider the following series of end of period cash flows - 3 B Cumulative End of Year Amount CF (1,000s of $) C b) 0 70,000 -100,000 D a) Payback period with interest 4.25 E 1 years 2 F -10,000 3 0 G 4 + H 0 20,000 30,000 40,000 40,000 40,000 5 - C. Plot the results of A and B together in one graph. Use Excel's XY (scatter) plotting feature. 10000 6 A. Find the payback period without interest (also known as "undiscounted payout" or just plain "payout") B. The company can borrow funds at 6% and management requires a profit margin of 4%. Find the payback period with interest (also known as the "discounted payback period" or "discounted payout") J K L M N O 4 5 6 7 8 9 10 A 11 12 B C D E F G H J K L M 1 2 Problem 5. Your company buys a truck for $17,000. To make this purchase, your company takes a loan at 11% APR for 60 months. 3 What schedule of monthly principal, interest and total payments must your company make, month-by-month and cumulative, to service the loan over its life? Provide the amortization schedule (using excel functions or A. equations from Peterson). N If your company had taken the loan for only 48 months instead of the 60 months, what would be the differences in the monthly total payment and the cumulative interest payments compared with the 60 month loan that you actually got? Provide the amortization schedule (using excel functions or equations from B. Peterson). O H

Expert Answer:

Answer rating: 100% (QA)

Answers A MARR is an abbreviation for Minimum Acceptable ... View the full answer

Related Book For

Construction accounting and financial management

ISBN: 978-0135017111

2nd Edition

Authors: Steven j. Peterson

Posted Date:

Students also viewed these finance questions

-

Question 2. This question uses the simple regression model to study the influence of the independent variable on the profit rate, for each research study (A, B, C). We will assess the applicability...

-

write a CNC Program to perform threading operation on a CNC lathe machine on a mild steel sample 2cm diameter. write Program in absolute mode. assume if any other information required

-

Ninety four cities provided information on vacancy rates (in percent) in local apartments in the following frequency distribution. The sample mean and the sample standard deviation are 8% and 4.0%,...

-

Court Casuals has 100,000 shares of common stock outstanding as of the beginning of the year and has the following transactions affecting stockholders' equity during the year. May 18 Issues 25,000...

-

You have been reading about the Madison Computer Company (MCC), which currently retains 90 percent of its earnings ($5 a share this year). It earns an ROE of almost 30 percent. a. Assuming a required...

-

Recall from Section 3.4.2 that a matrix is said to be sparse if most of its entries are zero. More 1. 2. formally, assume a m x n matrix A has sparsity coefficient (A) < < 1, where y(A) = d(A)/s(A),...

-

What is transfer of training? What role does transfer of training play in e-learning?

-

Humid air is to be conditioned in a constant pressure process at 1 atm from 39oC dry bulb and 50 percent relative humidity to 17oC dry bulb and 10.8oC wet bulb. The air is first passed over cooling...

-

The exchange rate between euros and dollars is currently 0.83 euros per dollar. Inflation is expected to be 1% in Europe and 2% in the US. If relative purchasing power parity holds, what is the...

-

CASE #3 SUPPLY CHAIN MANAGEMENT LEARNING OBJECTIVES 1 Definition and main terms of Supply Chain Management in organization. 2 Definition of Supply Chain Manager and description of the main duties...

-

The list price of an industrial machine is 84,500.00 subject to a 10% discount. What additional discount should be given to bring down the price to 70,000.00?

-

What is the purpose of a trustee?

-

What do we call the quantity force distance, and what quantity does it change?

-

How do the cash management practices of large and small businesses differ?

-

What are the two primary factors that affect a loans interest rate?

-

Identify a new fintech startup and describe its business model. What new services or features does it provide to its customers? How does it earn its revenue? How does it differ from traditional...

-

A particle of mass m is placed in a simple harmonic oscillator (SHO) potential. a) Write down a statevector ) which maximizes the expectation value in position, (x), and is constructed as a linear...

-

Give an example of transitory income. What effect does this income have on the marginal propensity to consume?

-

At what periodic interest rate is a $4,000 cash receipt occurring at the beginning of year 1 equivalent to ten annual $750 cash disbursements? The first cash disbursement occurs at the end of year 1,...

-

A supplier has offered your company a 1% discount for all bills that are paid 15 days after they are billed. The bills would normally be due 45 days after they are billed. What is the return on...

-

What activities are involved in managing the companys cash flows?

-

1. Describe the bases of power held by Dr. Jamie Thompson. Describe the bases of power held by Dr. Elizabeth Clarke. 2. What activities and people have contributed to Jaime Thompsons power? What...

-

What is the current in the wire in Figure Q22.1? 1.0 VR + 1.0-1.0V + FIGURE Q22.1

-

Electroconvulsive therapy is a last-line treatment for certain mental disorders. In this treatment, an electric current is passed directly through the brain, inducing seizures. The total charge that...

Study smarter with the SolutionInn App