Proud Corporation acquired 80 percent of Spirited Companys voting stock on January 1, 20X3, at underlying book

Question:

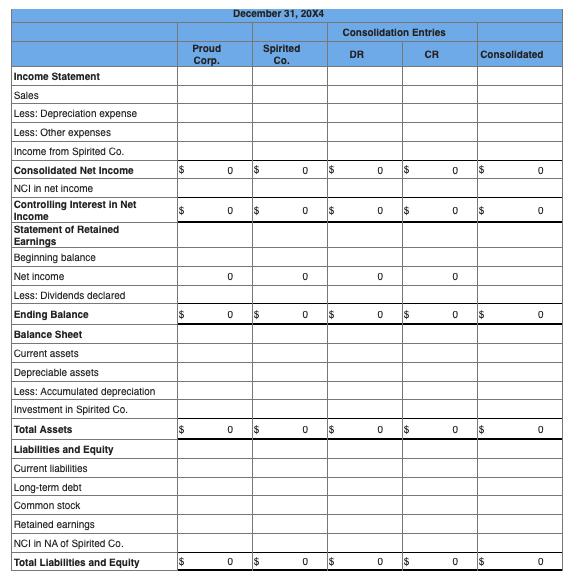

Proud Corporation acquired 80 percent of Spirited Company’s voting stock on January 1, 20X3, at underlying book value. The fair value of the noncontrolling interest was equal to 20 percent of the book value of Spirited at that date. Assume that the accumulated depreciation on depreciable assets was $48,000 on the acquisition date. Proud uses the equity method in accounting for its ownership of Spirited. On December 31, 20X4, the trial balances of the two companies are as follows:

| Proud Corporation | Spirited Company | |||||||||||||||

| Item | Debit | Credit | Debit | Credit | ||||||||||||

| Current Assets | $ | 235,000 | $ | 154,000 | ||||||||||||

| Depreciable Assets | 502,000 | 315,000 | ||||||||||||||

| Investment in Spirited Company | 121,440 | |||||||||||||||

| Depreciation Expense | 22,000 | 12,000 | ||||||||||||||

| Other Expenses | 143,000 | 88,000 | ||||||||||||||

| Dividends Declared | 52,000 | 22,200 | ||||||||||||||

| Accumulated Depreciation | $ | 195,000 | $ | 72,000 | ||||||||||||

| Current Liabilities | 68,000 | 48,000 | ||||||||||||||

| Long-Term Debt | 101,240 | 197,200 | ||||||||||||||

| Common Stock | 181,000 | 80,000 | ||||||||||||||

| Retained Earnings | 265,000 | 50,000 | ||||||||||||||

| Sales | 230,000 | 144,000 | ||||||||||||||

| Income from Spirited Company | 35,200 | |||||||||||||||

| $ | 1,075,440 | $ | 1,075,440 | $ | 591,200 | $ | 591,200 | |||||||||

Required:

a. Prepare all consolidation entries required on December 31, 20X4, to prepare consolidated financial statements. (If no entry is required for a transaction/event, select "No journal entry required" in the first account field.)

b. Prepare a three-part consolidation worksheet as of December 31, 20X4. (Values in the first two columns (the "parent" and "subsidiary" balances) that are to be deducted should be indicated with a minus sign, while all values in the "Consolidation Entries" columns should be entered as positive values. For accounts where multiple adjusting entries are required, combine all debit entries into one amount and enter this amount in the debit column of the worksheet. Similarly, combine all credit entries into one amount and enter this amount in the credit column of the worksheet.)

Please help me complete the figures in part A, and the consolidation worksheet.

Expert Answer:

Event Accounts Debit Credit 1 Common stock 80000 Retained earnings 50000 Income from Spirited Compan... View the full answer

Advanced Financial Accounting

ISBN: 978-0078025624

10th edition

Authors: Theodore E. Christensen, David M. Cottrell, Richard E. Baker