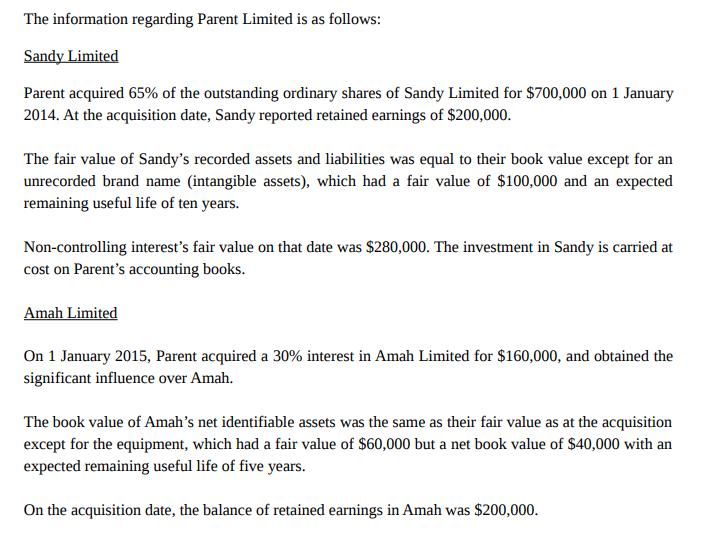

The information regarding Parent Limited is as follows: Sandy Limited Parent acquired 65% of the outstanding...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

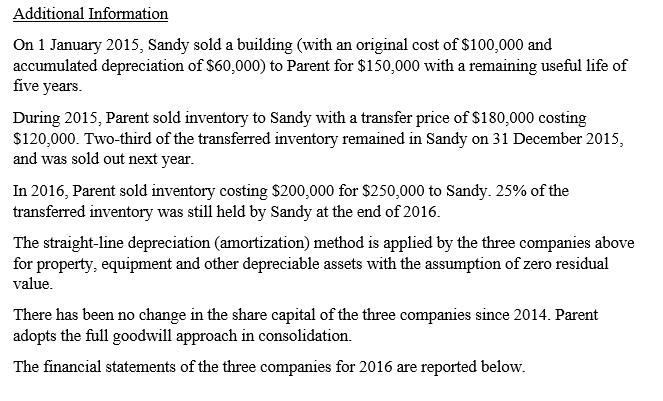

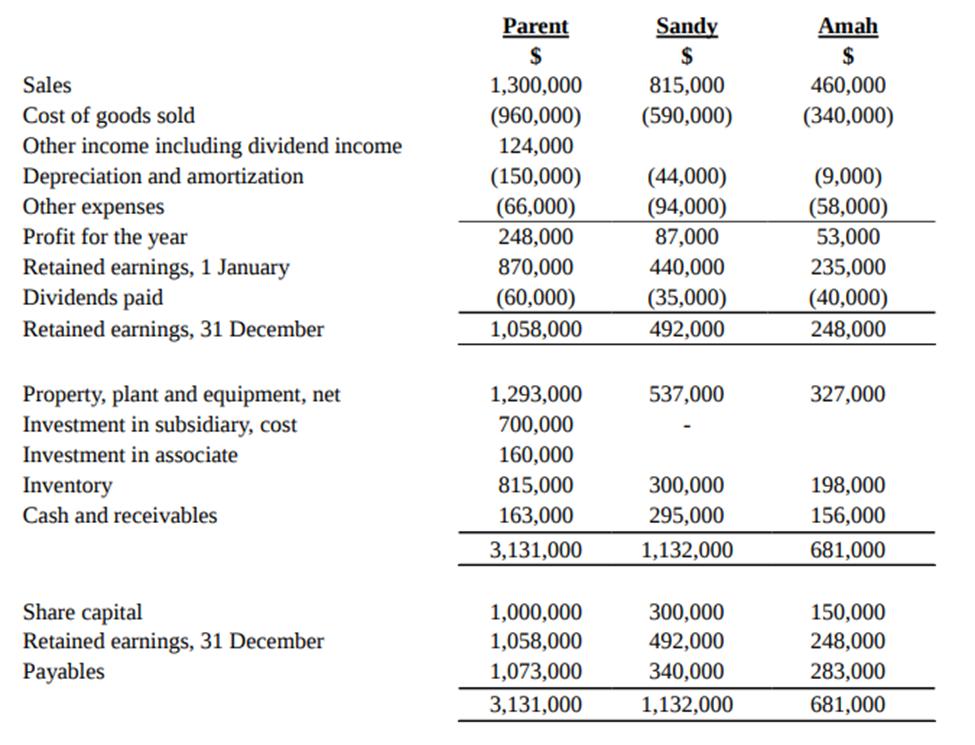

The information regarding Parent Limited is as follows: Sandy Limited Parent acquired 65% of the outstanding ordinary shares of Sandy Limited for $700,000 on 1 January 2014. At the acquisition date, Sandy reported retained earnings of $200,000. The fair value of Sandy's recorded assets and liabilities was equal to their book value except for an unrecorded brand name (intangible assets), which had a fair value of $100,000 and an expected remaining useful life of ten years. Non-controlling interest's fair value on that date was $280,000. The investment in Sandy is carried at cost on Parent's accounting books. Amah Limited On 1 January 2015, Parent acquired a 30% interest in Amah Limited for $160,000, and obtained the significant influence over Amah. The book value of Amah's net identifiable assets was the same as their fair value as at the acquisition except for the equipment, which had a fair value of $60,000 but a net book value of $40,000 with an expected remaining useful life of five years. On the acquisition date, the balance of retained earnings in Amah was $200,000. Additional Information On 1 January 2015, Sandy sold a building (with an original cost of $100,000 and accumulated depreciation of $60,000) to Parent for $150,000 with a remaining useful life of five years. During 2015, Parent sold inventory to Sandy with a transfer price of $180,000 costing $120,000. Two-third of the transferred inventory remained in Sandy on 31 December 2015, and was sold out next year. In 2016, Parent sold inventory costing $200,000 for $250,000 to Sandy. 25% of the transferred inventory was still held by Sandy at the end of 2016. The straight-line depreciation (amortization) method is applied by the three companies above for property, equipment and other depreciable assets with the assumption of zero residual value. There has been no change in the share capital of the three companies since 2014. Parent adopts the full goodwill approach in consolidation. The financial statements of the three companies for 2016 are reported below. Sales Cost of goods sold Other income including dividend income Depreciation and amortization Other expenses Profit for the year Retained earnings, 1 January Dividends paid Retained earnings, 31 December Property, plant and equipment, net Investment in subsidiary, cost Investment in associate Inventory Cash and receivables Share capital Retained earnings, 31 December Payables Parent $ 1,300,000 (960,000) 124,000 (150,000) (66,000) 248,000 870,000 (60,000) 1,058,000 1,293,000 700,000 160,000 815,000 163,000 3,131,000 1,000,000 1,058,000 1,073,000 3,131,000 Sandy $ 815,000 (590,000) (44,000) (94,000) 87,000 440,000 (35,000) 492,000 537,000 300,000 295,000 1,132,000 300,000 492,000 340,000 1,132,000 Amah $ 460,000 (340,000) (9,000) (58,000) 53,000 235,000 (40,000) 248,000 327,000 198,000 156,000 681,000 150,000 248,000 283,000 681,000 Required (ignore taxation): Prepare the consolidation worksheet for the year ended 31 December 2016 for Parent Limited by using the worksheet in the answer booklet. The information regarding Parent Limited is as follows: Sandy Limited Parent acquired 65% of the outstanding ordinary shares of Sandy Limited for $700,000 on 1 January 2014. At the acquisition date, Sandy reported retained earnings of $200,000. The fair value of Sandy's recorded assets and liabilities was equal to their book value except for an unrecorded brand name (intangible assets), which had a fair value of $100,000 and an expected remaining useful life of ten years. Non-controlling interest's fair value on that date was $280,000. The investment in Sandy is carried at cost on Parent's accounting books. Amah Limited On 1 January 2015, Parent acquired a 30% interest in Amah Limited for $160,000, and obtained the significant influence over Amah. The book value of Amah's net identifiable assets was the same as their fair value as at the acquisition except for the equipment, which had a fair value of $60,000 but a net book value of $40,000 with an expected remaining useful life of five years. On the acquisition date, the balance of retained earnings in Amah was $200,000. Additional Information On 1 January 2015, Sandy sold a building (with an original cost of $100,000 and accumulated depreciation of $60,000) to Parent for $150,000 with a remaining useful life of five years. During 2015, Parent sold inventory to Sandy with a transfer price of $180,000 costing $120,000. Two-third of the transferred inventory remained in Sandy on 31 December 2015, and was sold out next year. In 2016, Parent sold inventory costing $200,000 for $250,000 to Sandy. 25% of the transferred inventory was still held by Sandy at the end of 2016. The straight-line depreciation (amortization) method is applied by the three companies above for property, equipment and other depreciable assets with the assumption of zero residual value. There has been no change in the share capital of the three companies since 2014. Parent adopts the full goodwill approach in consolidation. The financial statements of the three companies for 2016 are reported below. Sales Cost of goods sold Other income including dividend income Depreciation and amortization Other expenses Profit for the year Retained earnings, 1 January Dividends paid Retained earnings, 31 December Property, plant and equipment, net Investment in subsidiary, cost Investment in associate Inventory Cash and receivables Share capital Retained earnings, 31 December Payables Parent $ 1,300,000 (960,000) 124,000 (150,000) (66,000) 248,000 870,000 (60,000) 1,058,000 1,293,000 700,000 160,000 815,000 163,000 3,131,000 1,000,000 1,058,000 1,073,000 3,131,000 Sandy $ 815,000 (590,000) (44,000) (94,000) 87,000 440,000 (35,000) 492,000 537,000 300,000 295,000 1,132,000 300,000 492,000 340,000 1,132,000 Amah $ 460,000 (340,000) (9,000) (58,000) 53,000 235,000 (40,000) 248,000 327,000 198,000 156,000 681,000 150,000 248,000 283,000 681,000 Required (ignore taxation): Prepare the consolidation worksheet for the year ended 31 December 2016 for Parent Limited by using the worksheet in the answer booklet.

Expert Answer:

Related Book For

Financial Accounting

ISBN: 978-1118978085

IFRS 3rd edition

Authors: Jerry J. Weygandt, Paul D. Kimmel, Donald E. Kieso

Posted Date:

Students also viewed these accounting questions

-

On 1 January 2019 a company that prepares accounts to 31 December enters into a five-year lease of a machine from a developer. Lease payments are 50,000 per annual, payable at the end of the year....

-

Tuecke's Concrete acquired 20% of the outstanding ordinary shares of Drew, Ltd. on January 1, 2017, by paying 1,100,000 for 40,000 shares. Drew declared and paid a 0.50 per share cash dividend on...

-

Chen Inc. acquired 20% of the outstanding ordinary shares of Cho Corp. on December 31, 2010. The purchase price was 125,000,000 for 50,000 shares. Cho Corp. declared and paid an 80 per share cash...

-

The beam shown below is supported by a pin at A and a roller at B. The weight of the beam is 12 kN and a 15 kN force is applied 3 m to the right of A as shown. Determine the reaction forces at A and...

-

What role does return on investment and residual income play in responsibility accounting?

-

Silver Company makes a product that is very popular as a Mother s Day gift. Thus, peak sales occur in May of each year, as shown in the company s sales budget for the second quarter given below:...

-

How long does it take an ambulance to respond to a request for emergency medical aid? One of the goals of one study was to estimate the response time of ambulances using warning lights (Ho \&...

-

In February, a restaurant had a beginning inventory of $85,000, made purchases of $235,000 and had an ending inventory of $70,000. Employee meal costs for the month were $12,000. Food revenue for the...

-

RRumba Ltd is a small company based in St . Ann, Jamaica. They currently employ ten people.They are seeking to calculate their payroll costs for the month of December 2 0 2 3 . Sasha, the supervisor,...

-

A player plays a roulette game in a casino by betting on a single number each time. Because the wheel has 38 numbers, the probability that the player will win in a single play is 1/38. Each play of...

-

The arrival of customers at a teller counter follows Poisson distribition with a mean of 30 per hour and teller's service time follows exponential distribition with a mean of 1 minute. Determine the...

-

Consider a relation PC (P, C) which indicates that person P is a parent of person C. Furthermore, assume that there are two unary relations Male(P) and Female(P) that specify the gender of a person...

-

Often, it is just as important to review actual examples as opposed to just reviewing "how it is done" or "why you should do it". So I hope you will spend a few minutes reviewing this example of an...

-

As part of a weight reduction program, a man designs a monthly exercise program consisting of bicycling, jogging, and swimming. He would like to exercise at most 40 hours, devote at most 8 hours to...

-

Find the third derivative of the function f(x)=x-3x4

-

An accounting firm has just contacted your consulting business for assistance. They want to hire someone to do accounting and payroll. The bookstore is downstairs, while the office is upstairs in an...

-

1. 2. 3. Total asset = 10,00,000; Non-current asset = 6,00,000; Shareholders fund = 4,00,000; Reserve & surplus = 1,00,000; Non-current liability = 3,00,000 Current Ratio will be: a) 1:2 c) 4:3 b)...

-

Explain what is meant by vicarious liability and when it is available?

-

C. Free and G. Mann decide to merge their proprietorships into a partnership called Freemann Ltd. The statement of financial position for Mann shows:...

-

The following data, presented in alphabetical order, are taken from the records of Radar Industries Ltd. Accounts payable................................................................................

-

Sean Browne owns and manages a computer repair service, which had the following trial balance on December 31, 2016 (the end of its fiscal year). Summarized transactions for January 2017 were as...

-

Which one of the following cannot be a true statement about an object: (a) It has zero velocity and a nonzero acceleration; (b) it has velocity in the x-direction and acceleration in the y-direction;...

-

The equation x = xo +vxot + axt 12 2 applies (a) to all kinematic problems, (b) only if you is zero, (c) to constant accelerations, (d) to negative times.

-

For an object in curvilinear motion, (a) the objects velocity components are constant, (b) the y-velocity component is necessarily greater than the x-velocity component, (c) there is an acceleration...

Study smarter with the SolutionInn App