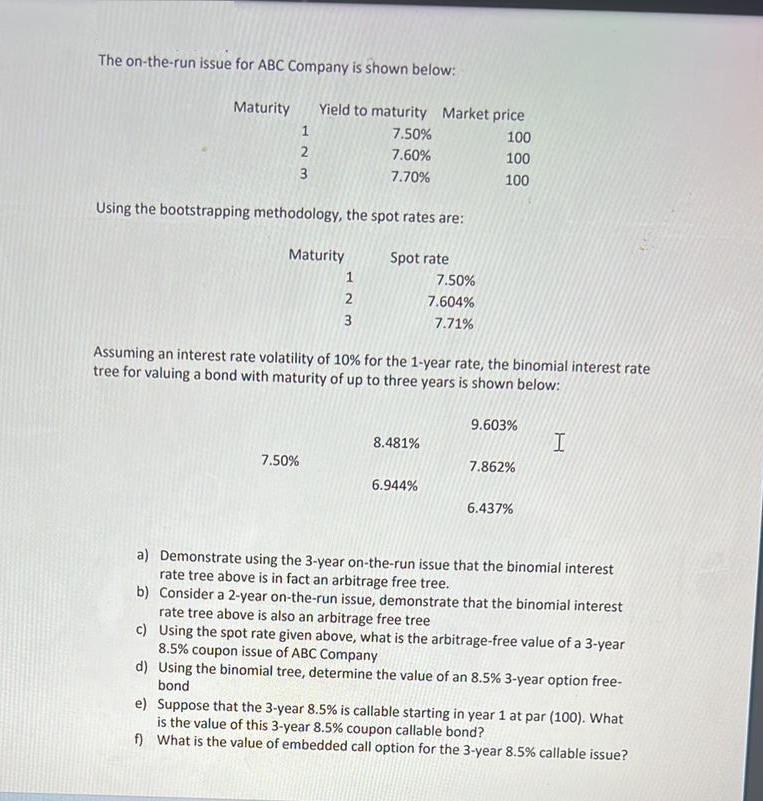

The on-the-run issue for ABC Company is shown below: Maturity 123 Yield to maturity Market price...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Posted Date: