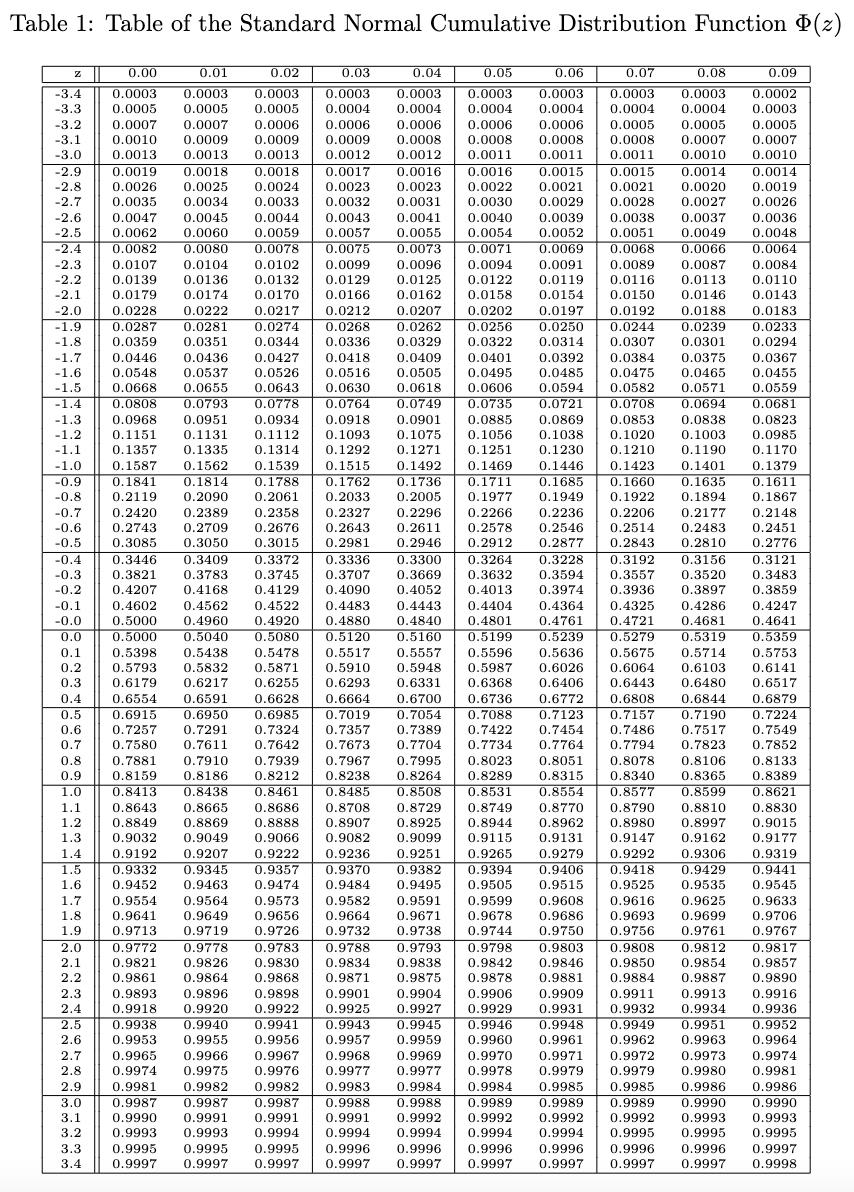

Use the Black-Scholes formula for calculations and show your steps. When evaluating N(z), use the values...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

Use the Black-Scholes formula for calculations and show your steps. When evaluating N(z), use the values in the attached N(z) table. a. What is the price of a $35 strike European call? Assume the current stock price is $38.50, the annual volatility is 0.25, the annualized continuously compounding interest rate is 6%, the stock pays no dividend, and the option expires in 45 days (assume 365 days a year). (6') b. What is the price of a $30 strike European put? Assume the current stock price is $28.50, the annual volatility is 0.32, the annualized continuously compounding interest rate is 0.04, the stock pays a 1.0% continuous dividend, and the option expires in 110 days. (Assume 365 days a year). (6¹) c. Interpret the N(d₁) values you obtained in a. and b. (3') Table 1: Table of the Standard Normal Cumulative Distribution Function Þ(z) 0.00 0.01 0.06 0.02 0.03 0.0003 0.0003 0.0003 0.0003 0.0005 0.0005 0.0005 0.0004 0.0007 0.0006 0.04 0.05 0.0003 0.0003 0.0003 0.0004 0.0006 0.0007 0.0006 0.0009 0.0010 0.0009 0.0009 0.0008 0.0008 0.0013 0.0013 0.0013. 0.0012 0.0012 0.0011 z -3.4 -3.3 -3.2 -3.1 -3.0 -2.9 20 -2.8 -2.7 -2.6 -2.5 -2.4 -2.3 -2.2 -2.1 -2.0 24.0 -1.9 -1.5 -1.8 -1.7 -1.6 TE -1.5 → -1.4 -1.3 -1.2 -1.1 -1.0 -1.0 -0.9 -0.8 -0.7 -0.6 -0.5 -0.4 -0.3 -0.2 02 -0.1 -0.0 0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2 12 1.3 11 1.4 1.5 1.6 1.7 1.8 10 1.9 2.6 2.0 2.7 2.1 2.8 2.0 2.9 2.3 3.0 3.1 3.2 3.3 3.4 0.0019 0.0018 0.0026 0.0025 0.0035 0.0021 0.0034 0.0017 0.0047 0.0018 0.0017 0.0016 0.0016 0.0024 0.0023 0.0023 0.0022 0.0033 0.0032 0.0021 0.0031 0.0030 0.0044 0.0043 00041 0.0040 0.0059 0.0059 0.0057 0.0055 0.0054 0.0082 0.0080 0.0078 0.0075 0.0073 0.0071 0.0102 0.0099 0.0096 0.0094 0.0122 0.0132 0.0129 0.0125 0.0170 0.0166 0.0162 0.0158 0.0202 0.0202 0.0197 0.0192 0.0192 0.0256 0.0250 0.0244 0.0307 0.0015 0.0045 0.0062 0.0060 0.0107 0.0104 0.0139 0.0136 0.0179 0.0174 0:011 0.0228 0.0222 0.0220 0.0287 0.0359 0.0000 0.0217 0.0222 0.0241 0.0212 0:0416 0.0281 0.0274 0.0268 0.0351 1.0991 0.0427 0026 0.0537 0.0526 0.0516 OOGEE 0.0613 0.0655 0.0643 OROD 0.0793 0.0446 0.0436 0.0940 0.0450 0.0548 0.0668 0 0630 0.0630 0.0778 0.0764 0.0808 0.0968 0.0951 0.0934 0.0918 1101 0.1151 0.1131 0.1112 0.1093 0.1357 0.1335 0.1314 0.1292 0.1515 0.1587 0.1562 0.1539 1.1962 0.1959 0.1901 0.1814 0.1788 0.1762 0.1736 1.1014 0.1841 0.2061 0.2119 0.2090 1.6118 0.2420 0.0344 COOLT 0.2389 0700 0742 0.2743 0.2709 0.3085 0.3050 0 2050 0.0336 .0530 0.2358 0.2676 0.3015 0.8413 0.8438 0.0410 0.0418 0.0410 0.2033 2099 0.8461 1.0490 0.0401 0.8665 0.8686 0.6628 10:0040 0.6985 0.7019 0.0207 00000 0.0262 0.6664 0:0004 0.7910 0.7939 0.7967 0000 0.8238 0100 0.8186 FOLOO 0.8212 0.3446 0.3409 0.3372 0.3821 0.3783 0.3745 0.4207 0.4168 1168 0.4129 0.4602 0.4562 0.4522 0.3336 0.3300 0.3707 0.3669 0.4090 0.4052 0.4483 0.4443 0.5000 0.4960 0.4920 0.4880 0.4840 0.5000 0.5040 0.5080 0.5120 0.5160 0.5398 0.5438 0.5478 0.5517 0.5557 0.5793 0.5832 0.5948 0.6179 0.5871 0.5910 0.6217 0.6255 0.6293 0.6331 0.6554 0.6700 0.7054 FORG 0.6591 0.6915 0.6950 0.6950 0.7257 0.7291 OFERO 0.7580 0.7611 0.7642 FORS 2010 0.7881 0.7324 0.7357 0.7389 0.7642 *1991 0.8159 0.07 0.0003 0.0004 0.0004 0.0004 0.0006 0.0006 0.0005 0.0008 0.0008 0.0011 0.0409 0.0409 0.0505 0.0401 0.0401 0.0322 0.0329 0:0529 1.0924 0.1469 1:1409 0.1711 0.0015 0.0015 0.0021 0.0029 0.0029 0.0039 0.0039 0.0052 0.0495 00000 0.0606 0.0618 0.0749 0.0901 0.1075 0.1271 0.1492 0.1492 0.6736 0:0790 0.7088 0.1068 0.7422 REG 0.7673 0.7704 0.7734 7067 0000 0.7995 0.8023 0.8264 9290 0.8289 0.0029 0.0038 0.0051 0.0069 0.0068 0.0091 0.0119 0.0154 0.0014 0.0314 CORDE 0.0735 0.0721 0.0885 0.0869 0.1056 0.1038 0.1251 0.1230 0.8531 0.0001 0.8749 0.1089 0.1685 0.2005 0.1977 0.1949 0.0501 0.0594 0.0392 0.0082 0.0485 0.0475 0.1446 BOTEZRO 0.0005 0.0007 0.0011 0.0010 0.0014 0.0021 0.0020 0.0029 0.0028 0.0027 0.6772 0.0172 0.2327 0.0643 0.2643 0.2611 0.2981 0.2946 0.2296 0.2266 -2290 1:2200 0.2578 0.2912 0.3264 0.3228 0.3192 0.3156 0.3632 0.3594 0.3557 0.3520 0.4013 0.3974 0.3936 0.3897 0.4325 0.4286 0.4761 0.4721 0.4681 0.4404 0.4364 0.4801 0.5199 0.5596 0.5636 0.5675 0.5987 0.6026 0.6064 0.6368 0.5239 0.5279 0.5319 0.0037 0.0049 0.0066 0.0089 0.0087 0.0116 0.0113 0.0150 0.0146 0.0188 0.0239 0.0301 0.0001 0.0384 0.000 0.7125 0.7123 COFFE 0.8554 0.0004 0.08 0.0003 0.0004 0.1423 1420 0.1660 OERO 0.0582 0.0571 0.0708 0.0694 0.0853 0.0838 0.1020 0.1003 0.1210 0.1190 0.0375 0.0579 0.0465 0.2236 0 DE AG 0.2546 0.2877 0.2843 0.2810 00514 0.2514 0.1401 0.1401 0.1922 0.1894 9.1944 0.1007 0.2206 0.2177 Det 0.2483 0.1635 0.105 0.5714 0.6103 0.6406 0.6443 0.6480 0.8078 0010 0.7157 0.7454 0.7486 0.7517 FRO 0.7764 0.7794 0.7823 GOOFS 0.8051 0.001 0.8315 0.6808 0.6844 0.0044 0.7190 0.7190 0.8106 0.8340 0.8365 5040 0.09 0.0002 0.0003 0.0005 0.0007 0.0010 0.8485 0.8508 .0400 0.8643 0.8708 0.8729 0.8577 0.8599 F90!! 0.0099 0.8770 0.8790 0.8810 08080 00010 0 2999 0.9860 2060 0.8849 0.8869 0.8888 0 2007 0.8907 08011 0.8925 0.8962 0.9131 0.9147 0.9162 0.9279 0.9292 0.9306 0.9406 0.9418 0.9429 0.8944 0.9032 0.9049 0.9066 0.9082 0.9099 0.9115 0.9192 0.9207 0.9222 0.9236 0.9251 0.9265 0.9332 0.9345 0.9357 0.9370 0.9382 0.9394 0.9452 0.9463 0.9474 0.9484 0.9495 0.9505 0.9554 0.9564 0.9573 0.9582 0.9591 0.9599 0.9641 0.9649 0.9656 0.9664 0.9671 0.9678 0.0712 0714 0.9744 Dies 0.9515 0.9525 0.9535 0.9608 0.9616 0.9625 0000 0.0761 0.9713 0.9719 0.9726 0.9732 0.9738 De 0.9686 0.9693 0.9699 0.9750 0.9756 0.9761 0.9803 0.9808 0.9812 0.9817 0.9612 2.0 0.9772 0.9778 0.9783 0.9788 0.0050 2.1 0921 0.9821 0.9826 0.9846 0.9850 0.9854 0.9857 2.2 22 0.9861 0.9864 0.9878 0.9881 0.9887 0.9890 0.9881 0.9884 0 9911 0.0000 0.9909 0.9911 0.9913 0.9932 0.9934 2.5 0.9949 0.9951 0.9962 0.9963 0.9793 0.9798 0.0980 0040 0.9830 0.9834 0.9838 0.9842 0.9868 0.9868 0.9871 0.9871 0.9875 2.3 23 0.9893 0.9896 0.9898 0.9898 0.9901 0.0001 0.9906 0.9904 2.4 0.9918 0.9920 0.9922 0.9925 0.9927 0.9929 0.9931 2.5 0.9938 0.9940 0.9941 0.9943 0.9945 0.9946 0.9948 0.9953 0.9956 0.9955 0.9957 0.9959 0.9960 0.9961 0.9965 0.9966 0.9967 0.9968 0.9969 0.9970 0.9971 0.9972 0.9972 0.9974 0.9975 0.9976 0.9977 0.9977 0.9978 0.9979 0.9979 0.9981 0.9982 0.9982 0.9983 0.9984 0.9984 0.9985 0.9985 0.9964 0.99€ 0.9987 0.9988 0.9988 0.9989 0.9989 0.9989 0.9990 0.9991 0.9991 0.9991 0.9992 0.9992 0.9992 0.9993 0.9993 0.9994 0.9994 0.9994 0.9994 0.9994 0.9995 0.9995 0.9995 0.9995 0.9996 0.9996 0.9996 0.9996 0.9996 0.9996 0.9997 0.9997 0.9997 0.9997 0.9997 0.9997 0.9997 0.9997 0.9987 0.9987 0.9992 0.9993 0.9995 0.9997 0.9973 0.9980 0.9986 0.9990 0.0014 0.0019 0.0026 0.0026 0.0036 0.0048 0.0064 0.0084 0.0110 0.0143 0.0183 0:0109 0.0233 0.0294 0.0494 0.0367 0.0455 0.0559 0.0681 0.0823 0.0985 0.1170 0.1379 1919 0.1611 ·1011 0.1867 0.2148 0.4120 0.2451 0.2776 0.3121 0.3483 0.3859 0.4247 0.4641 0.5359 0.8133 0 2290 0.8389 0.8621 0.8830 0.8980 0.8997 0.9015 2007 0.9177 0.5753 0.6141 0.6517 0.6879 0.7224 0.7549 0.7852 0.9319 0.9441 0.9545 0.9633 0.9706 0.9767 0.9916 0.9936 0.9952 0.9964 0.9974 0.9981 19001 0.9986 9900 0.9990 0.9993 0.9995 0.9997 0.9998 Use the Black-Scholes formula for calculations and show your steps. When evaluating N(z), use the values in the attached N(z) table. a. What is the price of a $35 strike European call? Assume the current stock price is $38.50, the annual volatility is 0.25, the annualized continuously compounding interest rate is 6%, the stock pays no dividend, and the option expires in 45 days (assume 365 days a year). (6') b. What is the price of a $30 strike European put? Assume the current stock price is $28.50, the annual volatility is 0.32, the annualized continuously compounding interest rate is 0.04, the stock pays a 1.0% continuous dividend, and the option expires in 110 days. (Assume 365 days a year). (6¹) c. Interpret the N(d₁) values you obtained in a. and b. (3') Table 1: Table of the Standard Normal Cumulative Distribution Function Þ(z) 0.00 0.01 0.06 0.02 0.03 0.0003 0.0003 0.0003 0.0003 0.0005 0.0005 0.0005 0.0004 0.0007 0.0006 0.04 0.05 0.0003 0.0003 0.0003 0.0004 0.0006 0.0007 0.0006 0.0009 0.0010 0.0009 0.0009 0.0008 0.0008 0.0013 0.0013 0.0013. 0.0012 0.0012 0.0011 z -3.4 -3.3 -3.2 -3.1 -3.0 -2.9 20 -2.8 -2.7 -2.6 -2.5 -2.4 -2.3 -2.2 -2.1 -2.0 24.0 -1.9 -1.5 -1.8 -1.7 -1.6 TE -1.5 → -1.4 -1.3 -1.2 -1.1 -1.0 -1.0 -0.9 -0.8 -0.7 -0.6 -0.5 -0.4 -0.3 -0.2 02 -0.1 -0.0 0.0 0.1 0.2 0.3 0.4 0.5 0.6 0.7 0.8 0.9 1.0 1.1 1.2 12 1.3 11 1.4 1.5 1.6 1.7 1.8 10 1.9 2.6 2.0 2.7 2.1 2.8 2.0 2.9 2.3 3.0 3.1 3.2 3.3 3.4 0.0019 0.0018 0.0026 0.0025 0.0035 0.0021 0.0034 0.0017 0.0047 0.0018 0.0017 0.0016 0.0016 0.0024 0.0023 0.0023 0.0022 0.0033 0.0032 0.0021 0.0031 0.0030 0.0044 0.0043 00041 0.0040 0.0059 0.0059 0.0057 0.0055 0.0054 0.0082 0.0080 0.0078 0.0075 0.0073 0.0071 0.0102 0.0099 0.0096 0.0094 0.0122 0.0132 0.0129 0.0125 0.0170 0.0166 0.0162 0.0158 0.0202 0.0202 0.0197 0.0192 0.0192 0.0256 0.0250 0.0244 0.0307 0.0015 0.0045 0.0062 0.0060 0.0107 0.0104 0.0139 0.0136 0.0179 0.0174 0:011 0.0228 0.0222 0.0220 0.0287 0.0359 0.0000 0.0217 0.0222 0.0241 0.0212 0:0416 0.0281 0.0274 0.0268 0.0351 1.0991 0.0427 0026 0.0537 0.0526 0.0516 OOGEE 0.0613 0.0655 0.0643 OROD 0.0793 0.0446 0.0436 0.0940 0.0450 0.0548 0.0668 0 0630 0.0630 0.0778 0.0764 0.0808 0.0968 0.0951 0.0934 0.0918 1101 0.1151 0.1131 0.1112 0.1093 0.1357 0.1335 0.1314 0.1292 0.1515 0.1587 0.1562 0.1539 1.1962 0.1959 0.1901 0.1814 0.1788 0.1762 0.1736 1.1014 0.1841 0.2061 0.2119 0.2090 1.6118 0.2420 0.0344 COOLT 0.2389 0700 0742 0.2743 0.2709 0.3085 0.3050 0 2050 0.0336 .0530 0.2358 0.2676 0.3015 0.8413 0.8438 0.0410 0.0418 0.0410 0.2033 2099 0.8461 1.0490 0.0401 0.8665 0.8686 0.6628 10:0040 0.6985 0.7019 0.0207 00000 0.0262 0.6664 0:0004 0.7910 0.7939 0.7967 0000 0.8238 0100 0.8186 FOLOO 0.8212 0.3446 0.3409 0.3372 0.3821 0.3783 0.3745 0.4207 0.4168 1168 0.4129 0.4602 0.4562 0.4522 0.3336 0.3300 0.3707 0.3669 0.4090 0.4052 0.4483 0.4443 0.5000 0.4960 0.4920 0.4880 0.4840 0.5000 0.5040 0.5080 0.5120 0.5160 0.5398 0.5438 0.5478 0.5517 0.5557 0.5793 0.5832 0.5948 0.6179 0.5871 0.5910 0.6217 0.6255 0.6293 0.6331 0.6554 0.6700 0.7054 FORG 0.6591 0.6915 0.6950 0.6950 0.7257 0.7291 OFERO 0.7580 0.7611 0.7642 FORS 2010 0.7881 0.7324 0.7357 0.7389 0.7642 *1991 0.8159 0.07 0.0003 0.0004 0.0004 0.0004 0.0006 0.0006 0.0005 0.0008 0.0008 0.0011 0.0409 0.0409 0.0505 0.0401 0.0401 0.0322 0.0329 0:0529 1.0924 0.1469 1:1409 0.1711 0.0015 0.0015 0.0021 0.0029 0.0029 0.0039 0.0039 0.0052 0.0495 00000 0.0606 0.0618 0.0749 0.0901 0.1075 0.1271 0.1492 0.1492 0.6736 0:0790 0.7088 0.1068 0.7422 REG 0.7673 0.7704 0.7734 7067 0000 0.7995 0.8023 0.8264 9290 0.8289 0.0029 0.0038 0.0051 0.0069 0.0068 0.0091 0.0119 0.0154 0.0014 0.0314 CORDE 0.0735 0.0721 0.0885 0.0869 0.1056 0.1038 0.1251 0.1230 0.8531 0.0001 0.8749 0.1089 0.1685 0.2005 0.1977 0.1949 0.0501 0.0594 0.0392 0.0082 0.0485 0.0475 0.1446 BOTEZRO 0.0005 0.0007 0.0011 0.0010 0.0014 0.0021 0.0020 0.0029 0.0028 0.0027 0.6772 0.0172 0.2327 0.0643 0.2643 0.2611 0.2981 0.2946 0.2296 0.2266 -2290 1:2200 0.2578 0.2912 0.3264 0.3228 0.3192 0.3156 0.3632 0.3594 0.3557 0.3520 0.4013 0.3974 0.3936 0.3897 0.4325 0.4286 0.4761 0.4721 0.4681 0.4404 0.4364 0.4801 0.5199 0.5596 0.5636 0.5675 0.5987 0.6026 0.6064 0.6368 0.5239 0.5279 0.5319 0.0037 0.0049 0.0066 0.0089 0.0087 0.0116 0.0113 0.0150 0.0146 0.0188 0.0239 0.0301 0.0001 0.0384 0.000 0.7125 0.7123 COFFE 0.8554 0.0004 0.08 0.0003 0.0004 0.1423 1420 0.1660 OERO 0.0582 0.0571 0.0708 0.0694 0.0853 0.0838 0.1020 0.1003 0.1210 0.1190 0.0375 0.0579 0.0465 0.2236 0 DE AG 0.2546 0.2877 0.2843 0.2810 00514 0.2514 0.1401 0.1401 0.1922 0.1894 9.1944 0.1007 0.2206 0.2177 Det 0.2483 0.1635 0.105 0.5714 0.6103 0.6406 0.6443 0.6480 0.8078 0010 0.7157 0.7454 0.7486 0.7517 FRO 0.7764 0.7794 0.7823 GOOFS 0.8051 0.001 0.8315 0.6808 0.6844 0.0044 0.7190 0.7190 0.8106 0.8340 0.8365 5040 0.09 0.0002 0.0003 0.0005 0.0007 0.0010 0.8485 0.8508 .0400 0.8643 0.8708 0.8729 0.8577 0.8599 F90!! 0.0099 0.8770 0.8790 0.8810 08080 00010 0 2999 0.9860 2060 0.8849 0.8869 0.8888 0 2007 0.8907 08011 0.8925 0.8962 0.9131 0.9147 0.9162 0.9279 0.9292 0.9306 0.9406 0.9418 0.9429 0.8944 0.9032 0.9049 0.9066 0.9082 0.9099 0.9115 0.9192 0.9207 0.9222 0.9236 0.9251 0.9265 0.9332 0.9345 0.9357 0.9370 0.9382 0.9394 0.9452 0.9463 0.9474 0.9484 0.9495 0.9505 0.9554 0.9564 0.9573 0.9582 0.9591 0.9599 0.9641 0.9649 0.9656 0.9664 0.9671 0.9678 0.0712 0714 0.9744 Dies 0.9515 0.9525 0.9535 0.9608 0.9616 0.9625 0000 0.0761 0.9713 0.9719 0.9726 0.9732 0.9738 De 0.9686 0.9693 0.9699 0.9750 0.9756 0.9761 0.9803 0.9808 0.9812 0.9817 0.9612 2.0 0.9772 0.9778 0.9783 0.9788 0.0050 2.1 0921 0.9821 0.9826 0.9846 0.9850 0.9854 0.9857 2.2 22 0.9861 0.9864 0.9878 0.9881 0.9887 0.9890 0.9881 0.9884 0 9911 0.0000 0.9909 0.9911 0.9913 0.9932 0.9934 2.5 0.9949 0.9951 0.9962 0.9963 0.9793 0.9798 0.0980 0040 0.9830 0.9834 0.9838 0.9842 0.9868 0.9868 0.9871 0.9871 0.9875 2.3 23 0.9893 0.9896 0.9898 0.9898 0.9901 0.0001 0.9906 0.9904 2.4 0.9918 0.9920 0.9922 0.9925 0.9927 0.9929 0.9931 2.5 0.9938 0.9940 0.9941 0.9943 0.9945 0.9946 0.9948 0.9953 0.9956 0.9955 0.9957 0.9959 0.9960 0.9961 0.9965 0.9966 0.9967 0.9968 0.9969 0.9970 0.9971 0.9972 0.9972 0.9974 0.9975 0.9976 0.9977 0.9977 0.9978 0.9979 0.9979 0.9981 0.9982 0.9982 0.9983 0.9984 0.9984 0.9985 0.9985 0.9964 0.99€ 0.9987 0.9988 0.9988 0.9989 0.9989 0.9989 0.9990 0.9991 0.9991 0.9991 0.9992 0.9992 0.9992 0.9993 0.9993 0.9994 0.9994 0.9994 0.9994 0.9994 0.9995 0.9995 0.9995 0.9995 0.9996 0.9996 0.9996 0.9996 0.9996 0.9996 0.9997 0.9997 0.9997 0.9997 0.9997 0.9997 0.9997 0.9997 0.9987 0.9987 0.9992 0.9993 0.9995 0.9997 0.9973 0.9980 0.9986 0.9990 0.0014 0.0019 0.0026 0.0026 0.0036 0.0048 0.0064 0.0084 0.0110 0.0143 0.0183 0:0109 0.0233 0.0294 0.0494 0.0367 0.0455 0.0559 0.0681 0.0823 0.0985 0.1170 0.1379 1919 0.1611 ·1011 0.1867 0.2148 0.4120 0.2451 0.2776 0.3121 0.3483 0.3859 0.4247 0.4641 0.5359 0.8133 0 2290 0.8389 0.8621 0.8830 0.8980 0.8997 0.9015 2007 0.9177 0.5753 0.6141 0.6517 0.6879 0.7224 0.7549 0.7852 0.9319 0.9441 0.9545 0.9633 0.9706 0.9767 0.9916 0.9936 0.9952 0.9964 0.9974 0.9981 19001 0.9986 9900 0.9990 0.9993 0.9995 0.9997 0.9998

Expert Answer:

Answer rating: 100% (QA)

a Price of a 35 strike European call Step 1 Calculate d1 d1 ln385035 006 02522 453650254536505 06404 ... View the full answer

Related Book For

Principles of Corporate Finance

ISBN: 978-0077404895

10th Edition

Authors: Richard A. Brealey, Stewart C. Myers, Franklin Allen

Posted Date:

Students also viewed these finance questions

-

Use information from Table 15.5. a. What is the price of a bond that pays one unit of the S&P index in 2 years? b. What quarterly dollar coupon is required if the bond is to sell at par? c. What...

-

Use information from Table 15.5. a. What is the price of a bond that pays one unit of the S&P index in 2 years? b. What quarterly dollar coupon is required if the bond is to sell at par? c. What...

-

What is the price of the following split coupon bond if comparable yields are 12 percent? Principal........ $1,000 Maturity........ 12 years Annual coupon........ 0% ($0) for years 13 10% ($100) for...

-

Use the method of separation of variables to find the product solution of the PDES: (a) u + Uy=3u (b) xu = 2yuy

-

How do firms determine what type of information is useful for a given decision? Is it possible for firms to have too much information? While a look at a firms Web site provides us with lots of...

-

An insulated cylinder fitted with a piston contains 0.1 kg of water at 100C, 90% quality. The piston is moved, compressing the water until it reaches a pressure of 1.2 MPa. How much work is...

-

1. Identify 3 students to play the roles of the employees. Ask these 3 individuals to read their roles below. 2. Identify 1 student to play the role of the president of the social enterprise (Taylor...

-

1. Interpret the computer output. What do the results presented above indicate? 2. Is the analytical approach used here appropriate? 3. Describe an alternative approach to the analysis of the...

-

On Wednesday, February 18, Jim Elsey, cost management specialist at Deere & Company in Moline, Illinois, received a call from Glen Lowery, sales manager in the Agricultural Products Division: Jim, I...

-

The 500-lb force is to be resolved into two components acting along the axis of the struts AB and AC. If the component of force along AC is required to be 300 lb, directed from A to C. determine the...

-

Suppose we want to find a student that qualifies for an internship. For each student, we input the name, the age of student and the final mark obtained for the examination in a while loop. To...

-

A river's current flows at 2.35 m/s [south]. If Alex can paddle their canoe at 3.14 m/s in still water and travels in a direction 13 north of west, what will their velocity be relative to an observer...

-

3 Two blocks of mass 2 kg and 4 kg are pushed by a horizontal force 12 N on a smooth horizontal table as shown in Fig. 3. 12 N 4 kg 2 kg smooth table Fig. 3 What is the acceleration of each of the...

-

Buyers of new cars shop for their preferred features - power seats, power steering, sunroof, ABS brakes and leather interior being a few examples. Several options combining some of these features are...

-

Write a function to convert an infix expression (2 (1 / 5 ) * 6 + 12 ) * 33 % 9) to postfix expression and display the result.

-

The table provides information on the production of a product. This product requires only one variable input, labor. The output for which worker shows the beginning of diminishing marginal returns?

-

Determine by direct integration the values of x for the two volumes obtained by passing a vertical cutting plane through the given shape of Fig. 5.21. The cutting plane is parallel to the base of the...

-

A common stock will pay a cash dividend of $4 next year. After that, the dividends are expected to increase indefinitely at 4% per year. If the discount rate is 14%, what is the PV of the stream of...

-

Construct a time line of the important events in the financial crisis that started in the summer of 2007. When do you think the crisis ended? You will probably want to review some of the entries...

-

Match each diagram, (a) and (b), with one of the following positions: Call buyer Call seller Put buyer Put seller Value of investment at maturity Value of investment at maturity Stock price 0...

-

Write a program in \(\mathrm{R}\) that simulates \(b\) samples of size \(n\) from a distribution that has distribution function \[F(x)= \begin{cases}0 & x For each sample, compute the sample quantile...

-

John bought 1,000 shares of Intel stock on October 18, 2015, for $30 per share plus a $750 commission he paid to his broker. On December 12, 2019, he sells the shares for $42.50 per share. He also...

-

Laura Li, a U.S. resident, worked for three months this summer in China. What type of tax authority may be especially useful in determining the tax consequences of her foreign income?

Study smarter with the SolutionInn App