We discussed in the class that the value of a financial asset must be non-negative. The following

Question:

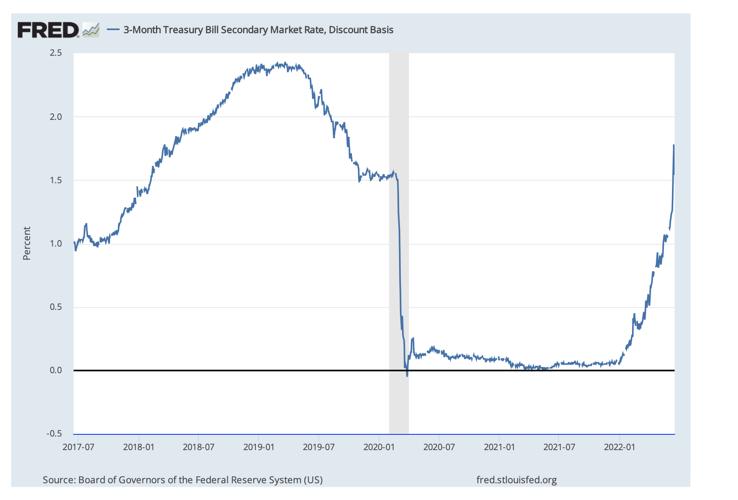

We discussed in the class that the value of a financial asset must be non-negative. The following figure shows the 90-day Treasury Bill Yield-to-Maturity (YTM) from the U.S.

Federal Reserve Bank of St. Louis. You can see that sometime during December 2020 interest rate became negative for a brief period of time. It is rate to see negative interest rate and it happened only a few times in history.Now consider a simple asset pricing model such as the Dividend Discounting Model (DDM)

with growth, where the price is a function of future dividend (D), interest rate (r) and

future cash-flow growth (g) and is given by: P0 = D1 . When the interest rate is negative, r−g

this model will give you a negative price which does not really make any economic sense. Does this mean that the Dividend Discounting Model (DDM) is an incorrect model of stock price?

How would you modify or build a new model of stock price so that the revised model would be robust to the phenomenon we observed on December 2020?

Expert Answer:

No the existence of negative interest rates does not necessarily mean that the Dividend Discounting ... View the full answer

Microeconomics An Intuitive Approach with Calculus

ISBN: 978-0538453257

1st edition

Authors: Thomas Nechyba