The following budget information for the year ending December 31, 2011, pertains to Rust Manufacturing Company's operations:

Question:

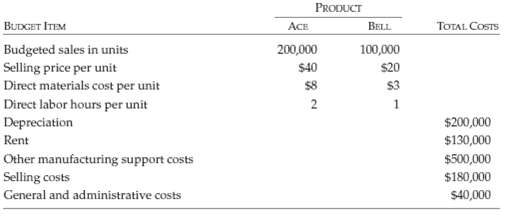

The following budget information for the year ending December 31, 2011, pertains to Rust Manufacturing Company's operations:

The following information is also provided:1. Rust has no beginning inventory. Production is planned so that it will equal the number of units sold.2. The cost of direct labor is $5 per hour.3. Depreciation and rent are fixed costs within the relevant range of production. Additional costs would be incurred for extra machinery and factory space if production is increased beyond current available capacity.4. Rust allocates depreciation proportional to machinery use and rent proportional to factory space. Budgeted usage is as follows:ACE BELLMachinery 70% 30%Factory space 60%40%5. Other manufacturing support costs include variable costs equal to 10% of direct labor cost and also include various fixed costs. None of the miscellaneous fixed manufacturing support costs depend on the level of activity, although support costs attributable to a specific product are avoidable if that product's production ceases. The fixed-cost portion of other manufacturing support costs is allocated between Ace and Bell on the basis of a percentage of budgeted direct labor cost. 6. Rust's selling and general and administrative costs are committed in the intermediate term.7. Rust allocates selling costs on the basis of number of units sold at Ace and Bell.8. Rust allocates general and administrative costs on the basis of sales revenue.Required(a) Prepare a schedule, using separate columns for Ace and Bell, showing budgeted sales, variable costs, contribution margin, fixed costs, and pretax operating profit for the year ending December 31, 2011.(b) Calculate the contribution margin per unit and the pretax operating profit per unit for Ace and for Bell.(c) Calculate the effect on pretax operating profit resulting from a 10% decrease in sales and production of each product.(d) What may be a problem with the aboveanalysis?

Contribution MarginContribution margin is an important element of cost volume profit analysis that managers carry out to assess the maximum number of units that are required to be at the breakeven point. Contribution margin is the profit before fixed cost and taxes...

Step by Step Answer:

a Rust Manufacturing Co BUDGET FOR ACE AND BELL For the Year Ending December 31 2011 Ace Bell Sales 1 8000000 2000000 Variable costs Direct materials ...View the full answer

Management Accounting Information for Decision-Making and Strategy Execution

ISBN: 978-0137024971

6th Edition

Authors: Anthony A. Atkinson, Robert S. Kaplan, Ella Mae Matsumura, S. Mark Young