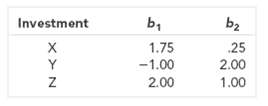

The following question illustrates the APT. Imagine that there are only two pervasive macroeconomic factors. Investments X,

Question:

The following question illustrates the APT. Imagine that there are only two pervasive macroeconomic factors. Investments X, Y, and Z have the following sensitivities to these two factors:

We assume that the expected risk premium is 4 percent on factor 1 and 8 percent on actor 2. Treasury bills obviously offer zero risk premium.

a. According to the APT, what is the risk premium on each of the three stocks?

b. Suppose you buy $200 of X and $50 of Y and sell $150 of Z. What is the sensitivity of your portfolio to each of the two factors? What is the expected risk premium?

c. Suppose you buy $80 of X and $60 of Y and sell $40 of Z. What is the sensitivity of your portfolio to each of the two factors? What is the expected risk premium?

d. Finally, suppose you buy $160 of X and $20 of Y and sell $80 of Z. What is your portfolio's sensitivity now to each of the two factors? And what is the expected risk premium?

e. Suggest two possible ways that you could construct a fund that has a sensitivity of .5 to factor 1 only. Now compare the risk premiums on each of these two investments.

f. Suppose that the APT did not hold and that X offered a risk premium of 8 percent, Y offered a premium of 14 percent, and Z offered a premium of 16 percent. Devise an investment that has zero sensitivity to each factor and that has a positive risk premium.

PortfolioA portfolio is a grouping of financial assets such as stocks, bonds, commodities, currencies and cash equivalents, as well as their fund counterparts, including mutual, exchange-traded and closed funds. A portfolio can also consist of non-publicly...

Step by Step Answer:

Let r x be the risk premium on investment X let xx be the portfolio weight of X and similarly for Investments Y and Z respectively a r x 175004 025008 ...View the full answer

Principles of Corporate Finance

ISBN: 978-0072869460

7th edition

Authors: Richard A. Brealey, Stewart C. Myers