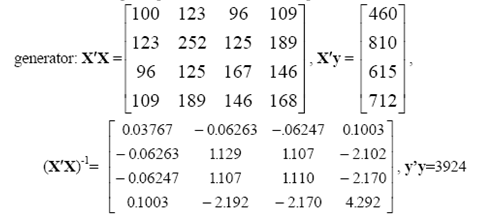

The following sample moments for x = [1, x1, x2, x3] were computed from 100 observations produced

Question:

The following sample moments for x = [1, x1, x2, x3] were computed from 100 observations produced using a random number generator:?

The true model underlying these data is y = x1 + x2 + x3 + ε.

a. Compute the simple correlations among the regressors.

b. Compute the ordinary least squares coefficients in the regression of y on a constant x1, x2, and x3.

c. Compute the ordinary least squares coefficients in the regression of y on a constant x1 and x2, on a constant x1 and x3, and on a constant x2 and x3.

d. Compute the variance inflation factor associated with each variable.

e. The regressors are obviously collinear. Which is the problem variable?

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The sample means are 1100 times the elements in the first column of XX The sample covarian...View the full answer

Answered By

Susan Juma

I'm available and reachable 24/7. I have high experience in helping students with their assignments, proposals, and dissertations. Most importantly, I'm a professional accountant and I can handle all kinds of accounting and finance problems.

15+ Reviews

45+ Question Solved

Related Book For

Question Posted: