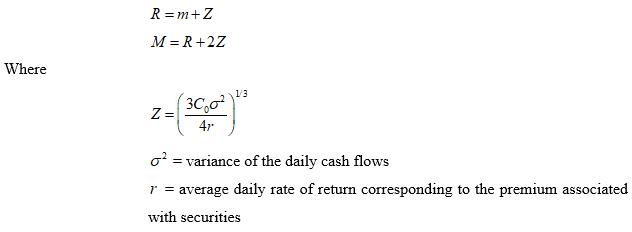

The Miller-Orr model in finance addresses the problem of managing its cash position by purchasing or selling

Question:

For example, if the premium is 4%, r = 0.04/365. To apply the model, note that we do not need to know the actual demand for cash, only the daily variance. Essentially, the Miller–Orr model determines the decision rule that minimizes the expected costs of making the cash-security transactions and the expected opportunity costs of maintaining the cash balance based on the variance of the cash requirements. Suppose that the daily requirements are normally distributed with a mean of 0 and variance of $60,000. Assume a transaction cost equal to $35, with an interest rate premium of 4%, and a required minimum balance of $7,500. Develop a spreadsheet implementation for this model. Apply Monte Carlo simulation to simulate the cash balance over the next year (365 days). Your simulation should apply the decision rule that if the cash balance for the current day is less than or equal to the minimum level, sell securities to bring the balance up to the return point. Otherwise, if the cash balance exceeds the upper limit, buy enough securities (i.e., subtract an amount of cash) to bring the balance back down to the return point. If neither of these conditions hold, there is no transaction and the balance for the next day is simply the current value plus the net requirement. Show the cash balance results on a line chart.

Monte Carlo simulationMonte Carlo simulation is a technique used to understand the impact of risk and uncertainty in financial, project management, cost, and other forecasting models. A Monte Carlo simulator helps one visualize most or all of the potential outcomes to...

Step by Step Answer:

RmZ MR2Z Transaction cost 3500 Interest rate premium on securities 4 Variance of cash flows daily 60000 Required minimum cash balance 7500 Return point 993130 Upper limit 1479389 day transaction cash ...View the full answer

Statistics Data Analysis And Decision Modeling

ISBN: 9780132744287

5th Edition

Authors: James R. Evans