You have recently been hired as the management accountant for ABC Manufacturing Technologies, Inc. The company produces

Question:

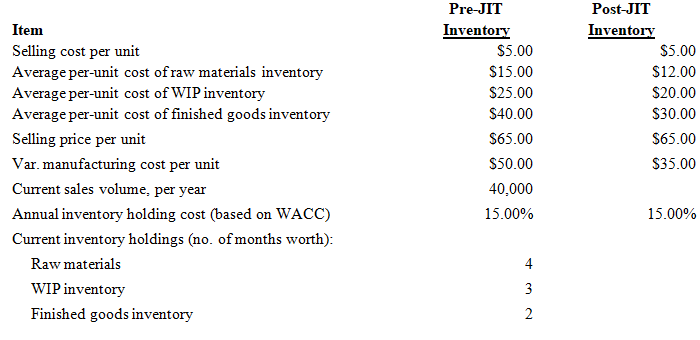

You have recently been hired as the management accountant for ABC Manufacturing Technologies, Inc. The company produces a broad line of subassemblies that are used in the production of flat-screen TVs and other electronic equipment. Competitive pressures, principally from abroad, have caused the company to reexamine its competitive strategy and associated management accounting and control systems. More to the point, the company feels a pressing need to adopt JIT manufacturing, to improve the quality of its outputs (in response to ever-increasing demands by consumers of electronic products), and to better manage its cost structure. A year ago ABC acquired, via a five-year lease, new manufacturing equipment, the annual cost of which is $500,000. To support the move to JIT, however, ABC would have to acquire new, computer-controlled manufacturing equipment, the leasing cost of which is estimated at $2 million per year for four years. If the company were to break its existing lease it would incur a one-time penalty of $240,000. The replacement equipment is expected to provide significant decreases in variable manufacturing cost per unit, from $50 to $35. This reduction is attributed to faster set-up times with the new machine, faster processing speed, a reduction in material waste, and a reduction in direct labor expenses (because of increased automation). In addition, improvements in manufacturing cycle time and improvements in product quality are expected to increase annual sales (in units) by approximately 30 percent (based on a current volume of 40,000 units).

Additional financial information regarding each decision alternative (existing equipment versus replacement equipment) is as follows:

Annual leasing cost, computer-controlled manufacturing equipment = | $2,000,000 | |

One-time penalty for breaking existing lease = | $240,000 | |

Existing lease payment per year, manufacturing equipment = | $500,000 | |

Life of project (in years) = | 4 | |

Projected increase in annual sales demand, after new program = | 30.00% | |

Projected decrease in all inventory holdings after new program = | 50.00% | |

The increased automation, including computer-based manufacturing controls, associated with the replacement equipment will greatly reduce the need for inventory holdings. The annual inventory-holding cost, based on the company’s weighted-average cost of capital, is 15 percent. Based on engineering estimates provided to ABC by the lessor company, all inventory holdings (raw materials, WIP, and finished goods) can safely be cut in half from current levels. Currently, ABC holds, on average, four months of raw materials inventory, three months of WIP inventory, and two months of finished goods inventory—all of which are based on production requirements.

Required

1. Essentially, how is a JIT manufacturing system different from a conventional system?

2. What is an appropriate role for management accounting regarding the adoption by a company of a JIT manufacturing system?

3. Based on the information presented above, determine the annual financial benefit (including reduction in inventory carrying costs) associated with the proposed move by the company to JIT.

4. Based on an analysis of financial considerations alone, should the company in this situation make the switch to JIT? Why or why not?

5. What qualitative factors might bear on the decision at hand?

Step by Step Answer:

1 A JIT manufacturing approach is considerably different from a conventional manufacturing system Under JIT an output is produced only when demanded by the customer internal or external At the core of ...View the full answer

Cost management a strategic approach

ISBN: 978-0073526942

5th edition

Authors: Edward J. Blocher, David E. Stout, Gary Cokins