Ian Stoddart was reviewing his companys 2013 year-end financial estimates, and he was not satisfied with the

Question:

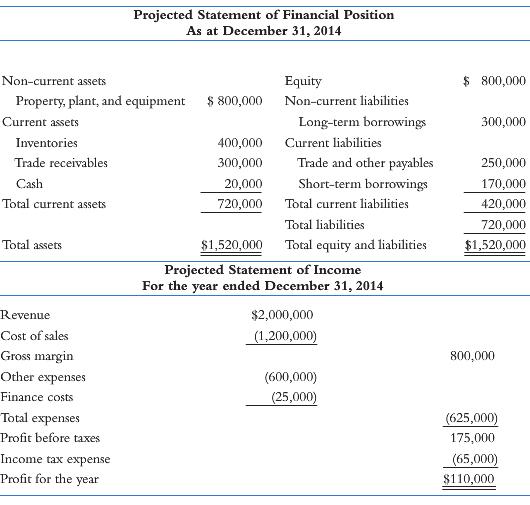

Ian Stoddart was reviewing his company’s 2013 year-end financial estimates, and he was not satisfied with the overall performance. He asked his management team to prepare their detailed operational plans for 2014 and provide their operating budgets to the controller so that he could consolidate the budgets and present, in the latter part of November, the company’s financial projections for 2014.

As he pointed out to his team, “The financial projections should be better than the year-end 2013 estimates. We have to achieve four basic financial objectives related to liquidity, solvency, and productivity, and our return on revenue (profitability) should be at least 4% and return on total assets more than 6%.

“The specific objectives for 2014 that I have in mind are as follows:

• Regarding liquidity, our current ratio should not be less than 1.5 times.

• For solvency, our debt-to-total-assets ratio should be maintained at no more that 50% and times-interest-earned should be more than 5.0 times.

• The productivity of our total assets should be 1.5 times, the average collection period for our trade receivables should be maintained at less than 45 days, and our inventory turnover should be more than 4 times;

• With respect to profitability, our return on revenue should be at least 4% and return on total assets over 6%.”

During the second week of November, the controller presented the projected 2014 financial statements to the management committee.

Should Ian Stoddart be satisfied with the 2014 financial projections?

Financial StatementsFinancial statements are the standardized formats to present the financial information related to a business or an organization for its users. Financial statements contain the historical information as well as current period’s financial...

Step by Step Answer:

Liquidity Projections Objectives Current ratio superior performance Current assets 720000 17 times 1...View the full answer