On January 1, 2011, Koosib acquired 80% of the shares (cum div.) of Turtle for $202,000. At

Question:

On January 1, 2011, Koosib acquired 80% of the shares (cum div.) of Turtle for $202,000. At this date, the equity of Turtle consisted of:

Share capital€”100,000 shares........ $100,000

Retained earnings ............. 90,000

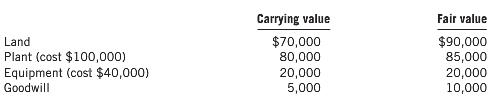

The carrying amounts and fair values of Turtle€™s assets were as follows:

Koosib uses the partial goodwill method.

Both plant and equipment were expected to have a further ï¬ve-year life, with beneï¬ts being received evenly over those periods. The plant was sold on July 1, 2013. At January 1, 2011, Turtle had not recorded an internally generated trademark that Koosib considered to have a fair value of $50,000. This intangible asset was considered to have an indeï¬nite useful life. Both companies pay tax at a rate of 30%.

Additional information:

1. The following proï¬ts were recorded by Turtle:

For the 2011 period $20,000

For the 2012 period 25,000

For the 2013 period 30,000

2. In March 2010, the dividend payable of $5,000 on hand at January 1, 2010, was paid by Turtle.

3. Other dividends declared or paid since January 1, 2011, are:

€¢ $8,000 dividend declared in December 2011, paid in February 2012

€¢ $6,000 dividend declared in December 2012, paid in February 2013

€¢ $5,000 dividend paid in June 2013

€¢ $8,000 dividend declared in December 2013, expected to be paid in February 2014

Required

(a) Prepare the adjustments for the preparation of the consolidated ï¬nancial statements of Koosib and its subsidiary,

Turtle, at December 31, 2013.

(b) Assume Koosib uses the full goodwill method and the value of the non-controlling interest at January 1, 2011, was $49,250. Prepare the adjustments that would differ from those in part (a) above.

A dividend is a distribution of a portion of company’s earnings, decided and managed by the company’s board of directors, and paid to the shareholders. Dividends are given on the shares. It is a token reward paid to the shareholders for their...

Step by Step Answer:

Acquisition Analysis as at January 1 2011 a Adjustments for the preparation of the consolidated financial statements of Koosib as at December 31 2013 3 years after acquisition Fair value adjustments C...View the full answer