The current price of stock ABC is 40. Stock ABC pays dividends continuously at a rate proportional

Question:

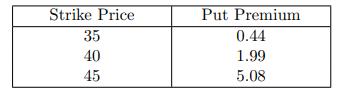

The current price of stock ABC is 40. Stock ABC pays dividends continuously at a rate proportional to its price. The dividend yield is 3%. The continuously compounded risk-free interest rate is 6%.

The following table shows the premiums of two-year put options on stock ABC of various strike prices:

Let S(2) be the price of stock ABC two years from now.

Determine the range of values of S(2) for which a 35-45 long bull spread outperforms a 40-strike long straddle, both of which are on stock ABC and expire in two years.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

To determine the range of values of S2 for which a 3545 long bull spread outperforms a 40strike lo...View the full answer

Answered By

Fahmin Arakkal

Tutoring and Contributing expert question and answers to teachers and students.

Primarily oversees the Heat and Mass Transfer contents presented on websites and blogs.

Responsible for Creating, Editing, Updating all contents related Chemical Engineering in

latex language

8+ Reviews

22+ Question Solved

Related Book For

Question Posted: