The current price of stock ABC is 40. Stock ABC pays dividends continuously at a rate proportional

Question:

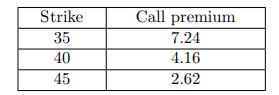

The current price of stock ABC is 40. Stock ABC pays dividends continuously at a rate proportional to its price. The dividend yield is 2%.

You are given the following premiums of one-year European call options on stock ABC for various strike prices:

The effective annual risk-free interest rate is 8%.

Let S(1) be the price of the stock one year from now.

Determine the range for S(1) such that a 35-strike short put produces a higher profit than a 45-strike short put, but a lower profit than a 40-strike short put.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Lets first calculate the implied volatilities of the call options using the BlackScholes model For each strike price we can set up the BlackScholes eq...View the full answer

Answered By

Antony Sang

I am a research and academic writer whose work is outstanding. I always have my customer's interests at heart. Time is an important factor in our day to day life so I am always time conscious. Plagiarism has never been my thing whatsoever. I give best Research Papers, Computer science and IT papers, Lab reports, Law, programming, Term papers, English and literature, History, Math, Accounting, Business Studies, Finance, Economics, Business Management, Chemistry, Biology, Physics, Anthropology, Sociology, Psychology, Nutrition, Creative Writing, Health Care, Nursing, and Articles.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: