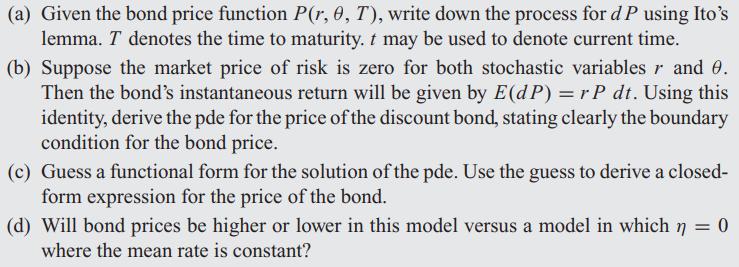

In this problem we extend the Vasicek model to allow the mean rate to become stochastic.

Question:

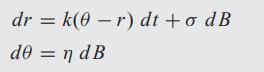

In this problem we extend the Vasicek model to allow the mean rate θ to become stochastic. Think of a situation in which the Federal Reserve makes minor adjustments to short-term market rates to manage the temperature of the economy. The model comprises the following two equations:

The Brownian motion d B is the same for both the interest rate r and its mean level θ. Answer the following questions:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Such a stochastic mean model of interest rates is studied in Balduz...View the full answer

Answered By

Grace Igiamoh-Livingwater

I am a qualified statistics lecturer and researcher with an excellent interpersonal writing and communication skills. I have seven years tutoring and lecturing experience in statistics. I am an expert in the use of computer software tools and statistical packages like Microsoft Office Word, Advanced Excel, SQL, Power Point, SPSS, STATA and Epi-Info.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: