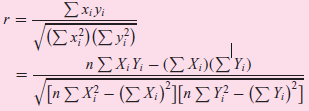

R. A. Fisher has derived the sampling distribution of the correlation coefficient defined in Eq. (3.5.13). xy

Question:

If it is assumed that the variables X and Y are jointly normally distributed, that is, if they come from a bivariate normal distribution , then under the assumption that the population correlation coefficient Ï is zero, it can be shown that t = r ˆš(n €“ 2)/ ˆš (1 ˆ’ r2) follows Student€™s t distribution with n ˆ’ 2 df.** Show that this t value is identical with the t value given in Eq. (5.3.2) under the null hypothesis that β2 = 0. Hence establish that under the same null hypothesis F = t2.

Eq (5.3.2) : t = (β̂2 €“ β2) ˆšÎ£xi2 / σ̂

DistributionThe word "distribution" has several meanings in the financial world, most of them pertaining to the payment of assets from a fund, account, or individual security to an investor or beneficiary. Retirement account distributions are among the most...

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Under the hyp...View the full answer

Answered By

Joseph Mwaura

I have been teaching college students in various subjects for 9 years now. Besides, I have been tutoring online with several tutoring companies from 2010 to date. The 9 years of experience as a tutor has enabled me to develop multiple tutoring skills and see thousands of students excel in their education and in life after school which gives me much pleasure. I have assisted students in essay writing and in doing academic research and this has helped me be well versed with the various writing styles such as APA, MLA, Chicago/ Turabian, Harvard. I am always ready to handle work at any hour and in any way as students specify. In my tutoring journey, excellence has always been my guiding standard.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: