(a) Make a chart similar to Fig. 6.9 showing the price of a put option using the...

Question:

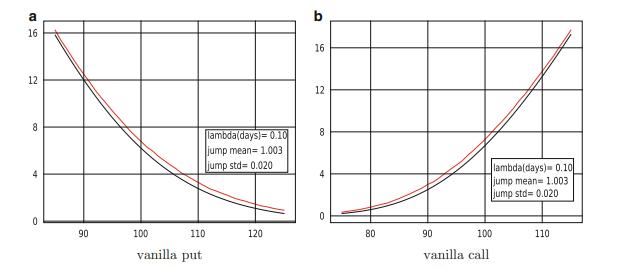

(a) Make a chart similar to Fig. 6.9 showing the price of a put option using the jump diffusion model with lognormal jumps for stock prices versus the GBM model. In order to compare the results with jump diffusion using N(μJ , σ2 J) jumps, find α and β to match the mean and variance,

![]()

(b) Do the same for calls.

Data Given in Figure 6.9

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

GOVIND BHAGWAT

Since Feb 2008, as a professional freelancer, I am engaged in consultancy, mentoring and tutoring in various finance and business related topics. Prior to that, I worked for more than 20 years in different managerial capacities with domestic and multinational companies. My prime responsibilities as a part of senior management were to be a problem solver specialist in finance and mentoring of team members. Imparting and sharing of knowledge & skills sets gives me a very enriching and fulfilling experience. This is the main philosophy of my overall career.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: