A US-based portfolio manager plans to invest in Australian zero-coupon bonds denominated in Australian dollars (AUD). He

Question:

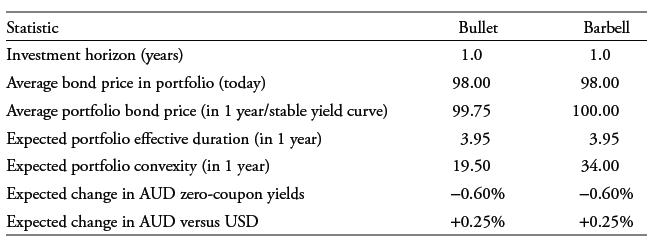

A US-based portfolio manager plans to invest in Australian zero-coupon bonds denominated in Australian dollars (AUD). He projects that over the next 12 months, the Australian zero-coupon yield curve will experience a downward parallel shift of 60 bps and that AUD will appreciate 0.25% against USD. The manager is weighing bullet and barbell strategies using the following data:

Solve for the expected return over the 1-year investment horizon for each portfolio using the step-by-step estimation approach in Equation 1.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Rolldown Return The sum of coupon income in and the price effect on bonds from rolling down the yiel...View the full answer

Answered By

SWAPNIL PURKAIT

Since boyhood I was interested in making people learn things which I know, my first opening being as a tutor started from Standard X.

Chemistry is something more than that of a wonder to me, I guess to you guys also. I had been teaching Chemistry since my graduation and now have experience of above three years.

My first success came that day when one of my students did the best in his school. Your success defines my success. I have helped students a lot and I will try my best to give you the best. Thank you.

0 Reviews

10+ Question Solved

Related Book For

Question Posted: