Assume a 1-year investment horizon for a portfolio manager considering US Treasury market strategies. The manager is

Question:

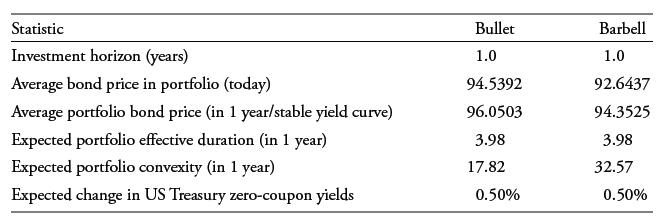

Assume a 1-year investment horizon for a portfolio manager considering US Treasury market strategies. The manager is considering two strategies to capitalize on an expected rise in US Treasury security zero-coupon yield levels of 50 bps in the next 12 months:

1. A bullet portfolio fully invested in 5-year zero-coupon notes currently priced at 94.5392.

2. A barbell portfolio: 62.97% is invested in 2-year zero-coupon notes priced at 98.7816, and 37.03% is invested in 10-year zero-coupon bonds priced at 83.7906.

Further assumptions for evaluating these portfolios are shown here:

Solve for the expected return over the 1-year investment horizon for each portfolio using the step-by-step estimation approach in Equation 1.

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Rolldown Return The sum of coupon income in and the price effect on bonds from rolling down the yiel...View the full answer

Answered By

Nazrin Ziad

I am a post graduate in Zoology with specialization in Entomology.I also have a Bachelor degree in Education.I posess more than 10 years of teaching as well as tutoring experience.I have done a project on histopathological analysis on alcohol treated liver of Albino Mice.

I can deal with every field under Biology from basic to advanced level.I can also guide you for your project works related to biological subjects other than tutoring.You can also seek my help for cracking competitive exams with biology as one of the subjects.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: