Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten

Question:

Daniela Ibarra is a senior analyst in the fixed-income department of a large wealth management firm. Marten Koning is a junior analyst in the same department, and David Lok is a member of the credit research team.

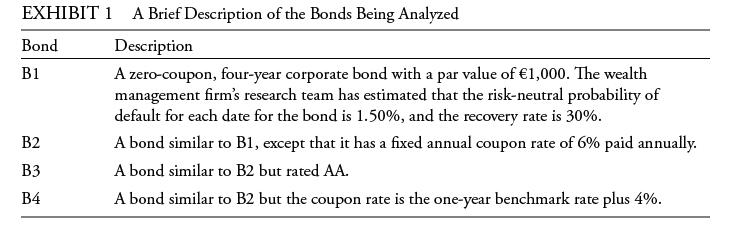

The firm invests in a variety of bonds. Ibarra is presently analyzing a set of bonds with some similar characteristics, such as four years until maturity and a par value of €1,000. Exhibit 1 includes details of these bonds.

Ibarra asks Koning to assist her with analyzing the bonds. She wants him to perform the analysis with the assumptions that there is no interest rate volatility and that the government bond yield curve is flat at 3%.

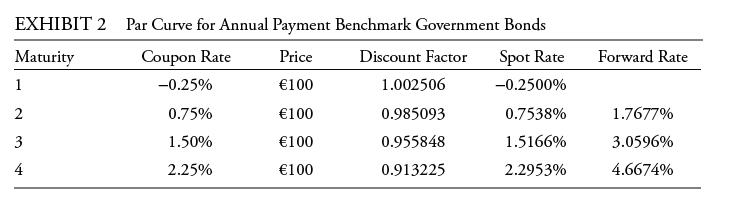

Ibarra performs the analysis assuming an upward-sloping yield curve and volatile interest rates. Exhibit 2 provides the data on annual payment benchmark government bonds.

She uses these data to construct a binomial interest rate tree based on an assumption of future interest rate volatility of 20%.

Answer the first five questions (1–5) based on the assumptions made by Marten Koning, the junior analyst. Answer Questions 8–12 based on the assumptions made by Daniela Ibarra, the senior analyst.

All calculations in this problem set are carried out on spreadsheets to preserve precision. The rounded results are reported in the solutions.

The issuer of the floating-rate note, B4, is in the energy industry. Ibarra believes that oil prices are likely to increase significantly in the next year, which will lead to an improvement in the firm’s financial health and a decline in the probability of default from 1.50% in Year 1 to 0.50% in Years 2, 3, and 4. Based on these expectations, which of the following statements is correct?

A. The CVA will decrease to €22.99.

B. The note’s fair value will increase to €1,177.26.

C. The value of the FRN, assuming no default, will increase to €1,173.55.

Step by Step Answer: