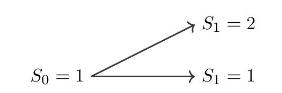

a) Consider the following binary one-step model (left(S_{t}ight)_{t=0,1,2}) with interest rate (r=0) and (mathbb{P}left(S_{1}=2ight)=1 / 3). b)

Question:

a) Consider the following binary one-step model \(\left(S_{t}ight)_{t=0,1,2}\) with interest rate \(r=0\) and \(\mathbb{P}\left(S_{1}=2ight)=1 / 3\).

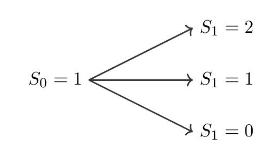

b) Consider the following ternary one-step model with \(r=0, \mathbb{P}\left(S_{1}=2ight)=1 / 4\) and \(\mathbb{P}\left(S_{1}=1ight)=1 / 9\).

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

a We denote the riskneutral measure by p P S 2 q P S 1 i Yes No Comment No loss is possible while a ...View the full answer

Answered By

Abigael martinez

I have been a tutor for over 3 years and have had the opportunity to work with students of all ages and backgrounds. I have a strong belief that all students have the ability to learn and succeed if given the right tools and support. I am patient and adaptable, and I take the time to get to know each student's individual learning style in order to best support their needs. I am confident in my ability to help students improve their grades and reach their academic goals.

1+ Reviews

10+ Question Solved

Related Book For

Introduction To Stochastic Finance With Market Examples

ISBN: 9781032288277

2nd Edition

Authors: Nicolas Privault

Question Posted: