This question is an extension of Exercise 10.22. Consider the data file (m r o z) on

Question:

This question is an extension of Exercise 10.22. Consider the data file \(m r o z\) on working wives and the model \(\ln (W A G E)=\beta_{1}+\beta_{2} E D U C+\beta_{3} E X P E R+e\). Use the 428 observations on married women who participate in the labor force. Let the instrumental variable be MOTHEREDUC.

a. Write down in algebraic form the three moment conditions, like (10.16), that would lead to the IV/2SLS estimates of the model above.

b. Calculate the IV/2SLS estimates and residuals, \(\hat{e}_{I V}\). What is the sum of the IV residuals? What is \(\sum\) MOTHEREDUC \(_{i} \times \hat{e}_{I V, i}\) ? What is \(\sum E X P E R_{i} \times \hat{e}_{I V, i}\) ? Relate these results to the moment conditions in (a).

c. What is \(\sum E D U C_{i} \times \hat{e}_{I V, i}\) ? What is the sum of squared IV residuals? How do these two results compare with the corresponding OLS results in Exercise 10.22(b)?

d. Calculate the IV/2SLS fitted values FLWAGE \(=\hat{\beta}_{1}+\hat{\beta}_{2} E D U C+\hat{\beta}_{3} E X P E R\). What is the sample average of the fitted values? What is the sample average of \(\ln (W A G E), \overline{\ln (W A G E)}\) ?

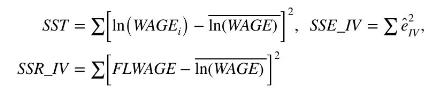

e. Find each of the following:

Compute \(S S R_{-} I V+S S E_{-} I V, R_{I V, 1}^{2}=S S R_{-} I V / S S T\), and \(R_{I V, 2}^{2}=1-S S E_{-} I V / S S T\). How do these values compare to those in Exercise 10.22(d)?

f. Does your IV/2SLS software report an \(R^{2}\) value. Is it either of the ones in (e)? Explain why the usual concept of \(R^{2}\) fails to hold for IV/2SLS estimation.

Data From Exercise 10.22:-

Consider the data file mroz on working wives and the model \(\ln (W A G E)=\beta_{1}+\beta_{2} E D U C+\) \(\beta_{3} E X P E R+e\). Use the 428 observations on married women who participate in the labor force.

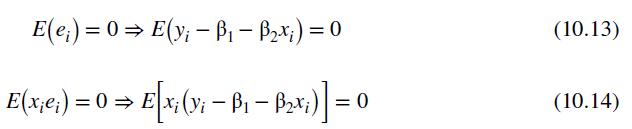

a. Write down in algebraic form the three moment conditions, like (10.13) and (10.14), that would lead to the OLS estimates of the model above.

b. Calculate the OLS estimates and residuals, \(\hat{e}_{i}\). What is the sum of the least squares residuals? What is the sum of squared least squares residuals? What is \(\sum E D U C_{i} \times \hat{e}_{i}\) ? What is \(\sum E X P E R_{i} \times \hat{e}_{i}\) ? Relate these results to the moment conditions in (a).

c. Calculate the fitted values \(\widehat{\ln (W A G E)}=b_{1}+b_{2} E D U C+b_{3} E X P E R\). What is the sample average of the fitted values? What is the sample average of \(\ln (W A G E), \overline{\ln (W A G E)}\) ?

d. Find each of the following:

Compute \(S S R+S S E, R^{2}=S S R / S S T\) and \(R^{2}=1-S S E / S S T\). Explain what these calculations show about measuring goodness-of-fit.

Data From Equation 10.13 and 10.14:-

Step by Step Answer:

Principles Of Econometrics

ISBN: 9781118452271

5th Edition

Authors: R Carter Hill, William E Griffiths, Guay C Lim