Consider a European down-and-out call option where the terminal payoff depends on the payoff state variable S

Question:

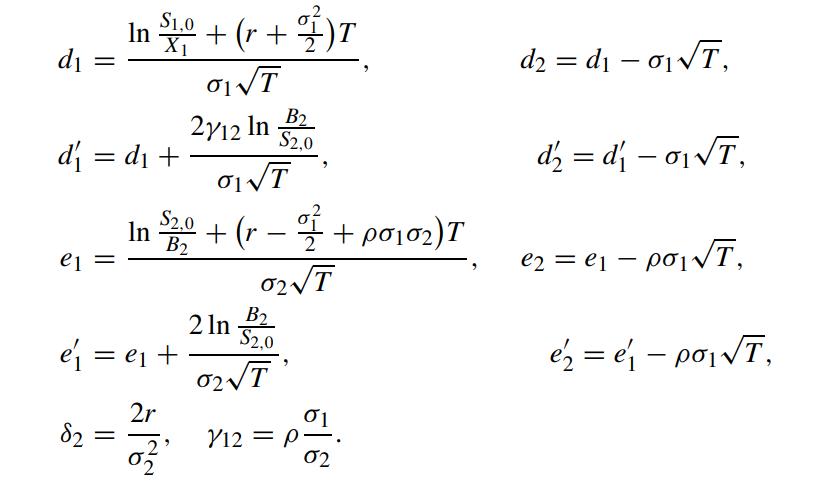

Consider a European down-and-out call option where the terminal payoff depends on the payoff state variable S1 and knock-out occurs when the barrier state variable S2 breaches the downstream barrier B2. Assume that under the risk neutral measure Q, the dynamics of S1,t and S2,t are given by

Let X1 denote the option’s strike price. Show that the price of this down-andout call with an external barrier is given by (Kwok, Wu and Yu, 1998)

Let X1 denote the option’s strike price. Show that the price of this down-andout call with an external barrier is given by (Kwok, Wu and Yu, 1998)

![call price = erTEQ[(S1,7 X)1(Sr>X(m>B]] 82-1+2/12 B2 - 5.0 [N2(d, 42; p) - (2)-1 = $2.0 N, 41;P)] N( er X[N](https://dsd5zvtm8ll6.cloudfront.net/images/question_images/1700/4/8/2/447655b4d8f3fb521700482443513.jpg)

where

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

Answered By

Rodrigo Louie Rey

I started tutoring in college and have been doing it for about eight years now. I enjoy it because I love to help others learn and expand their understanding of the world. I thoroughly enjoy the "ah-ha" moments that my students have. Interests I enjoy hiking, kayaking, and spending time with my family and friends. Ideal Study Location I prefer to tutor in a quiet place so that my students can focus on what they are learning.

1+ Reviews

10+ Question Solved

Related Book For

Question Posted: