Show that the put-call parity relations between the prices of floating strike and fixed strike Asian options

Question:

Show that the put-call parity relations between the prices of floating strike and fixed strike Asian options at the start of the averaging period are given by

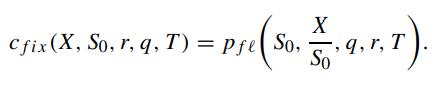

By combining the above put-call parity relations with the fixed-floating symmetry relation between cfℓ and pfix , deduce the following symmetry relation between cfix and pfℓ:

Fantastic news! We've Found the answer you've been seeking!

Step by Step Answer:

The putcall parity relations for floating and fixed strike Asian options can be derived as follows L...View the full answer

Answered By

Mugdha Sisodiya

My self Mugdha Sisodiya from Chhattisgarh India. I have completed my Bachelors degree in 2015 and My Master in Commerce degree in 2016. I am having expertise in Management, Cost and Finance Accounts. Further I have completed my Chartered Accountant and working as a Professional.

Since 2012 I am providing home tutions.

2+ Reviews

10+ Question Solved

Related Book For

Question Posted: