Suppose that we have Y 1 ,, Y m N( 1 ,), Y m+ 1 ,

Question:

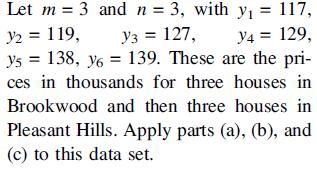

Suppose that we have Y1,…, Ym ∼ N(μ1,σ), Ym+1, …, Ym+n ∼ N(μ2, σ), and all m + n observations are independent. These are the assumptions of the pooled t procedure in Section 10.2. Let k = 1, x11 = .5, …, xm1 = .5, xm+1,1 = −.5, …, xm+n,1 = −.5. For convenience in inverting X′X assume m = n.

a. Obtain β̂0 and β̂1 from Equation (12.16). Let y̅1 be the mean of the first m observations and y̅2 be the mean of the next n observations.

Equation (12.16)

b. Find simple expressions for ŷ, SSE, se, and sβ̂1.

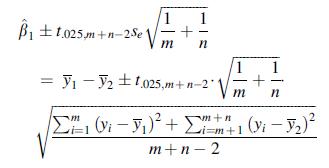

c. Use parts (a) and (b) to find a simple expression for the 95% CI for β̂1. Show that your formula is equivalent to

which is the pooled variance confidence interval discussed in Section 9.2.

d.

Step by Step Answer:

Modern Mathematical Statistics With Applications

ISBN: 9783030551551

3rd Edition

Authors: Jay L. Devore, Kenneth N. Berk, Matthew A. Carlton