1. Travis Company had no beginning work in process inventory. Its total manufacturing costs for the year...

Question:

1. Travis Company had no beginning work in process inventory. Its total manufacturing costs for the year were $427,000. If cost of goods manufactured was $332,000 and cost of goods sold was $250,000, the amount of ending work in process inventory would have been:

a. $95,000.

b. $82,000.

c. $127,000.

d. $105,000.

2. McDonnell Industries estimated manufacturing overhead for the year at $290,000. Manufacturing overhead for the year was underapplied by $12,000. The company applied $235,000 to work in process. The amount of actual overhead would have been:

a. $278,000.

b. $247,000.

c. None of these.

d. $223,000.

3. The Winchester Company estimates for the 2014 accounting period that its overhead costs will amount to $595,000 and that it will work 85,000 direct labor hours. If actual overhead costs for the year amounted to $599,000 and actual labor hours amounted to 87,000, then overhead would be:

a. Over applied by $14,000.

b. Over applied by $10,000.

c. Under applied by $4,000.

d. Under applied by $10,000.

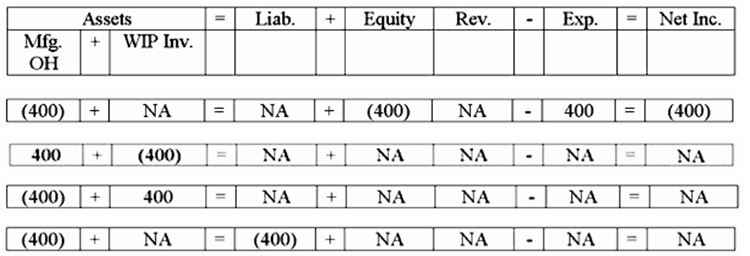

4. Ferguson Company recognized $400 of estimated manufacturing overhead costs at the end of the month. How does this transaction affect the financial statements?

5. Select the incorrect statement regarding service companies.

a. Service companies may have raw material costs.

b. Service companies do not maintain a finished goods account.

c. Understanding the cost of providing a service is just as important as knowing the cost of making a product.

d. Service companies accumulate their service costs in a work in process account similar to manufacturers.

6. Paying for factory utilities is a(n):

a. Asset source transaction.

b. Claims exchange transaction.

c. asset exchange transaction.

d. Asset use transaction.

7. All of the following are reasons to assign estimated overhead to inventory except:

a. Managers need cost information as soon as possible after production.

b. Managers need to know if production costs are higher than expected as soon as possible.

c. Managers need to use estimated overhead to control earnings.

d. Management reduces the distortions that would come from actual monthly overhead.

8. Product costs are expensed as cost of goods sold:

When production is complete.

a. At the start of production.

b. When the related revenue is collected.

c. When the related products are sold.

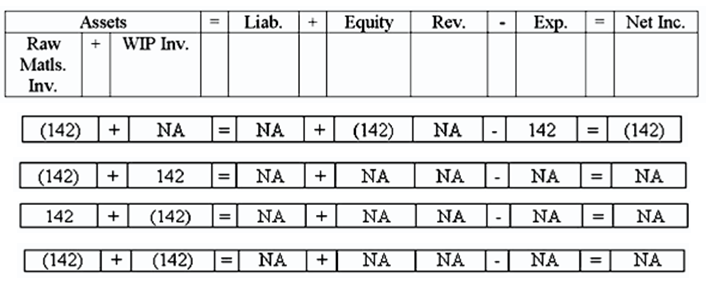

9. Orlando Company placed $142 of raw materials into production. How would this transaction affect the company's financial statements?

10. Which of the following correctly computes cost of goods manufactured?

10. Which of the following correctly computes cost of goods manufactured?

a. None of these.

b. Beginning work in process + Direct materials used + Direct labor + Overhead - Ending work in process

c. Beginning work in process + Cost of goods sold - Ending finished goods

d. Beginning work in process + Direct materials used + Direct labor + Overhead

11. A credit to the raw materials account represents:

a. Raw materials available for use.

b. Raw materials purchased.

c. None of these.

d. raw materials added to production.

12. Grimes Company sold 2,500 units that had cost $12,000 to produce. The recording of the sale would include an increase to:

a. Cost of goods sold.

b. Manufacturing overhead.

c. Finished goods.

d. Cost of goods manufactured.

Expert Answer:

1 a 95000 The calculation of ending work in process Beginning WIP Manufacturing cost ... View the full answer

Essentials of Marketing

ISBN: 978-0078028885

13th edition

Authors: William D. Perreault, Joseph P. Cannon