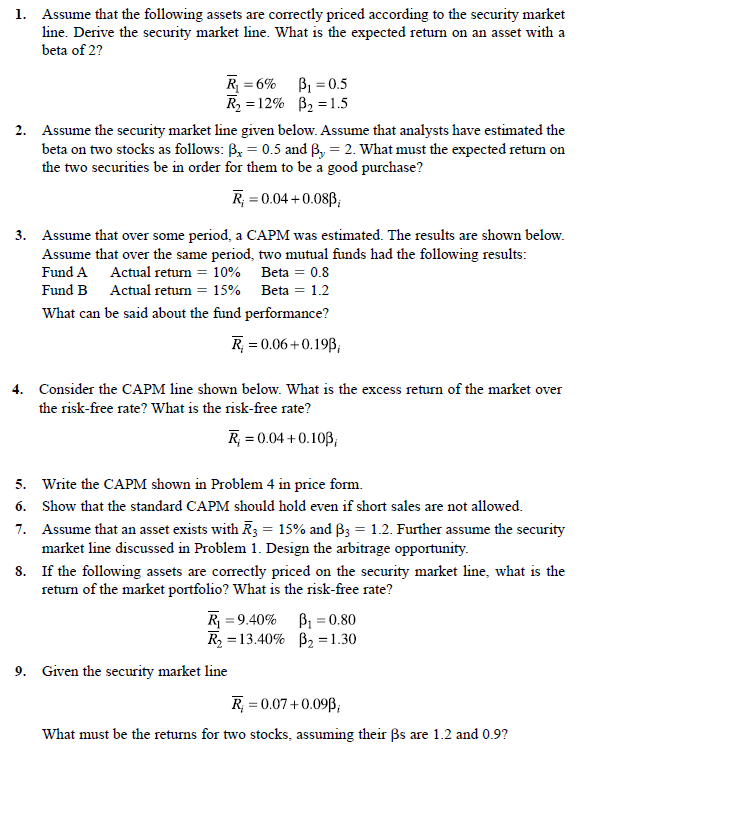

1. Assume that the following assets are correctly priced according to the security market line. Derive...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

Related Book For

Modern Portfolio Theory and Investment Analysis

ISBN: 978-1118469941

9th edition

Authors: Edwin Elton, Martin Gruber, Stephen Brown, William Goetzmann

Posted Date: