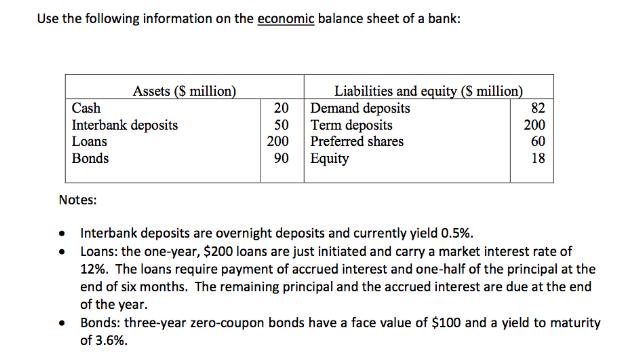

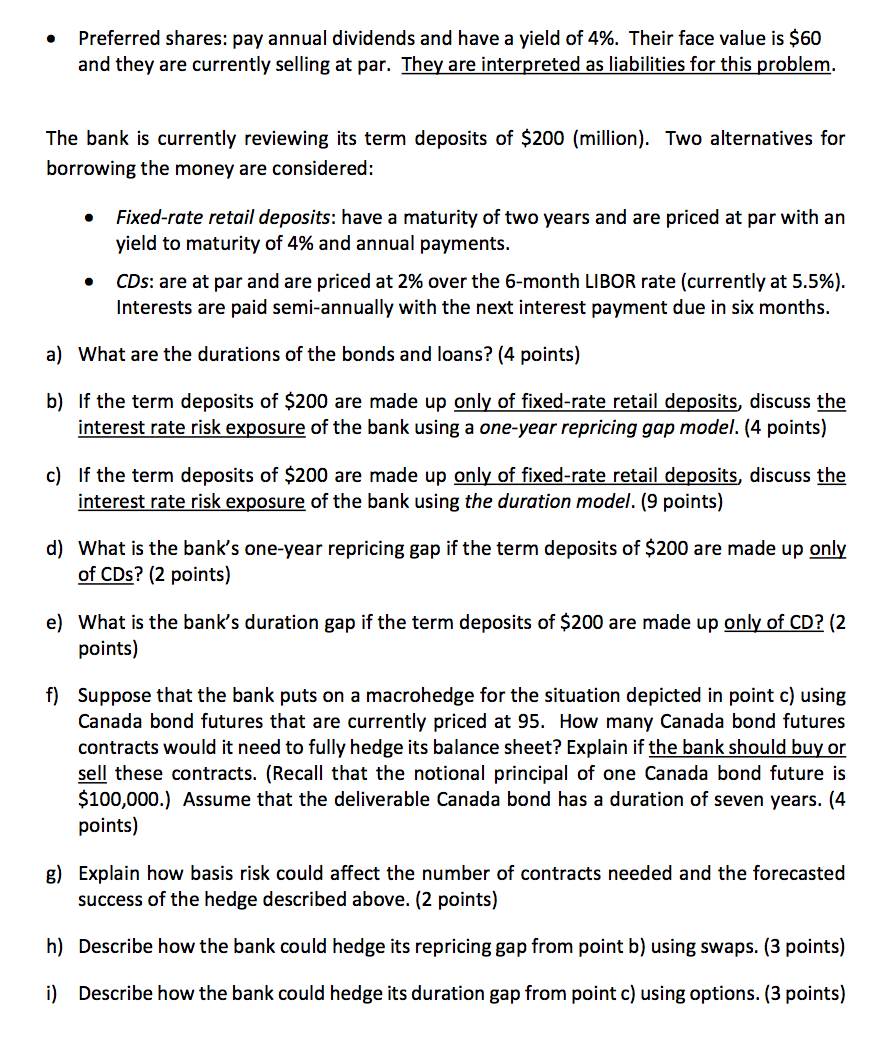

Use the following information on the economic balance sheet of a bank: Assets ($ million) Cash...

Fantastic news! We've Found the answer you've been seeking!

Question:

Expert Answer:

a To calculate the durations of the bonds and loans we can use the formula Duration PVTPriceDelta y 1 Bonds Duration of the bonds 1003900036 833 years ... View the full answer

Related Book For

Money Banking and Financial Markets

ISBN: 978-1259746741

5th edition

Authors: Stephen Cecchetti, Kermit Schoenholtz

Posted Date: