1: Identify a specific CONTROL REPORTS , give a detailed description with an example, and explain how

Fantastic news! We've Found the answer you've been seeking!

Question:

1:

Identify a specific CONTROL REPORTS, give a detailed description with an example, and explain how it can be used to hold an individual, group, or organization accountable.

2:

Please complete the following from the textbook:

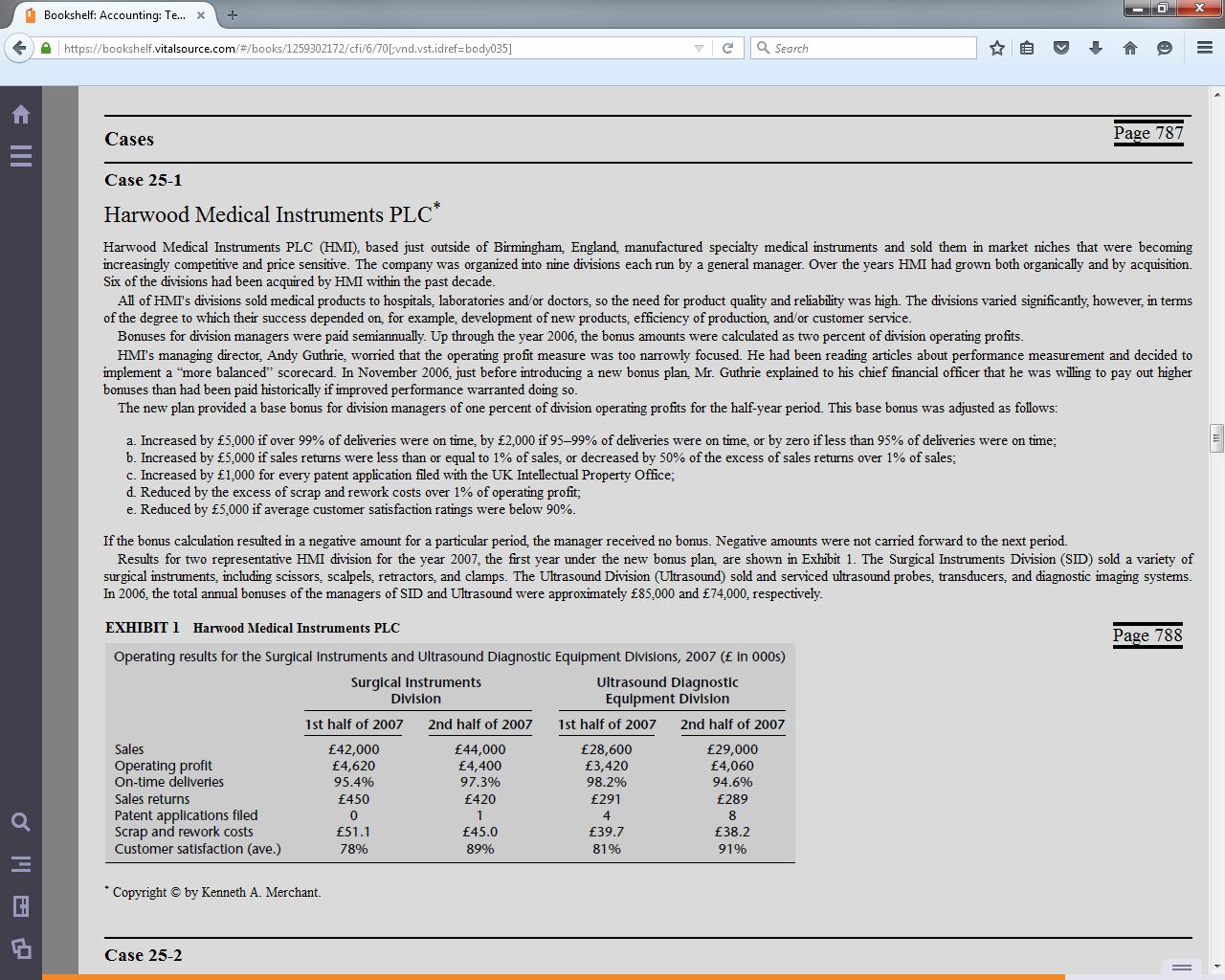

- Case 25.1 Harwood Medical Instruments PLC

This case asks you to evaluate a new bonus plan that was designed to specifically address the perceived shortcomings of a previous plan. In particular you should consider:

- The purpose of changing the system

- The calculated bonuses for the managers

- How well the new plan is working

Expert Answer:

Question No 1 Change is a systematic approach to managing all changes made to a product or system Th... View the full answer

Related Book For

Posted Date: