1. What is the debate highlighted in the paper? 2. What does consumer empowerment mean in...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

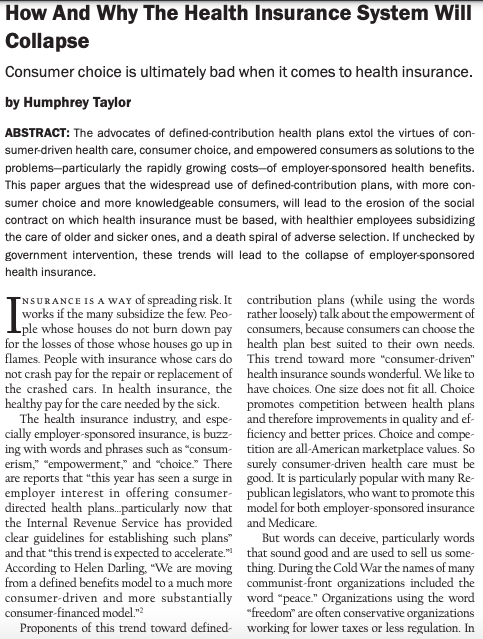

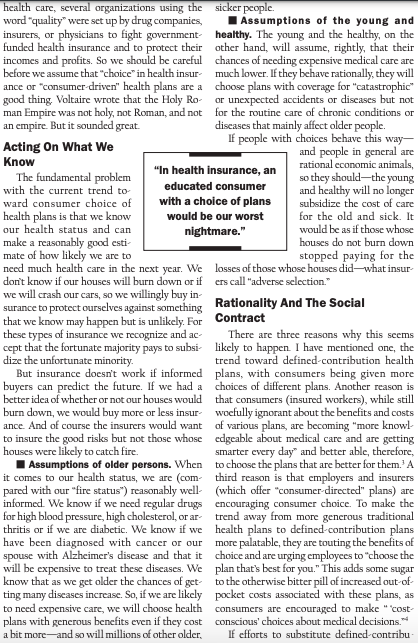

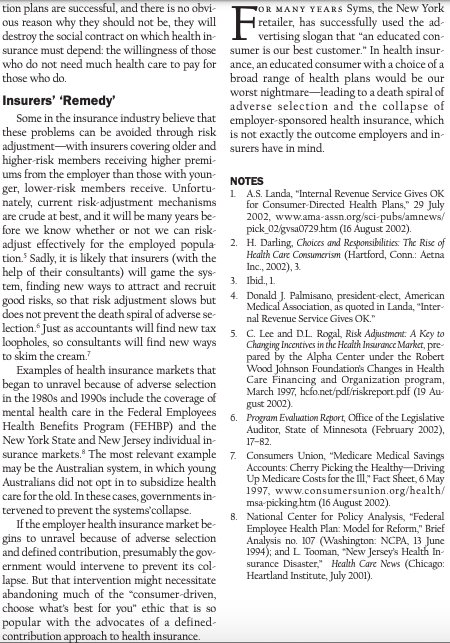

1. What is the debate highlighted in the paper? 2. What does consumer empowerment mean in the context this paper? Why is it deceptive? 3. What is a death spiral and why and how does it occur? How And Why The Health Insurance System Will Collapse Consumer choice is ultimately bad when it comes to health insurance. by Humphrey Taylor ABSTRACT: The advocates of defined-contribution health plans extol the virtues of con- sumer-driven health care, consumer choice, and empowered consumers as solutions to the problems-particularly the rapidly growing costs-of employer-sponsored health benefits. This paper argues that the widespread use of defined-contribution plans, with more con- sumer choice and more knowledgeable consumers, will lead to the erosion of the social contract on which health insurance must be based, with healthier employees subsidizing the care of older and sicker ones, and a death spiral of adverse selection. If unchecked by government intervention, these trends will lead to the collapse of employer-sponsored health insurance. NSURANCE IS A WAY of risk. It works if the many subsidize the few. Peo- ple whose do not burn down pay for the losses of those whose houses go up in flames. People with insurance whose cars do not crash pay for the repair or replacement of the crashed cars. In health insurance, the healthy pay for the care needed by the sick. contribution plans (while using the words rather loosely) talk about the empowerment of consumers, because consumers can choose the health plan best suited to their own needs. This trend toward more "consumer-driven" health insurance sounds wonderful. We like to have choices. One size does not fit all. Choice promotes competition between health plans The health insurance industry, and espe- and therefore improvements in quality and ef- cially employer-sponsored insurance, is buzz ficiency and better prices. Choice and compe- ing with words and phrases such as "consum-tition are all-American marketplace values. So erism," "empowerment," and "choice." There are reports that "this year has seen a surge in employer interest in offering consumer- directed health plans... particularly now that the Internal Revenue Service has provided clear guidelines for establishing such plans" and that "this trend is expected to accelerate." According to Helen Darling. "We are moving from a defined benefits model to a much more consumer-driven and more substantially consumer-financed model."2 Proponents of this trend toward defined surely consumer-driven health care must be good. It is particularly popular with many Re- publican legislators, who want to promote this model for both employer-sponsored insurance and Medicare. But words can deceive, particularly words that sound good and are used to sell us some- thing. During the Cold War the names of many communist-front organizations included the word "peace." Organizations using the word "freedom" are often conservative organizations working for lower taxes or less regulation. In health care, several organizations using the word "quality" were set up by drug companies, insurers, or physicians to fight government funded health insurance and to protect their incomes and profits. So we should be careful before we assume that "choice" in health insur- ance or "consumer-driven" health plans are a good thing. Voltaire wrote that the Holy Ro- man Empire was not holy, not Roman, and not an empire. But it sounded great. Acting On What We Know The fundamental problem with the current trend to- ward consumer choice of health plans is that we know our health status and can make a reasonably good esti- mate of how likely we are to need much health care in the next year. We don't know if our houses will burn down or if we will crash our cars, so we willingly buy in surance to protect ourselves against something that we know may happen but is unlikely. For these types of insurance we recognize and ac- cept that the fortunate majority pays to subsi- dize the unfortunate minority. "In health insurance, an educated consumer with a choice of plans would be our worst nightmare." But insurance doesn't work if informed buyers can predict the future. If we had a better idea of whether or not our houses would burn down, we would buy more or less insur- ance. And of course the insurers would want to insure the good risks but not those whose houses were likely to catch fire. sicker people. Assumptions of the young and healthy. The young and the healthy, on the other hand, will assume, rightly, that their chances of needing expensive medical care are much lower. If they behave rationally, they will choose plans with coverage for "catastrophic" or unexpected accidents or diseases but not for the routine care of chronic conditions or diseases that mainly affect older people. If people with choices behave this way- and people in general are rational economic animals, so they should the young and healthy will no longer subsidize the cost of care for the old and sick. It would be as if those whose houses do not burn down stopped paying for the losses of those whose houses did-what insur ers call "adverse selection." I Assumptions of older persons. When it comes to our health status, we are (com- pared with our "fire status") reasonably well informed. We know if we need regular drugs for high blood pressure, high cholesterol, or ar thritis or if we are diabetic. We know if we have been diagnosed with cancer or our spouse with Alzheimer's disease and that it will be expensive to treat these diseases. We know that as we get older the chances of get ting many diseases increase. So, if we are likely to need expensive care, we will choose health plans with generous benefits even if they cost a bit more and so will millions of other older. Rationality And The Social Contract There are three reasons why this seems likely to happen. I have mentioned one, the trend toward defined-contribution health plans, with consumers being given more choices of different plans. Another reason is that consumers (insured workers), while still woefully ignorant about the benefits and costs of various plans, are becoming "more knowl- edgeable about medical care and are getting smarter every day and better able, therefore, to choose the plans that are better for them. A third reason is that employers and insurers (which offer "consumer-directed" plans) are encouraging consumer choice. To make the trend away from more generous traditional health plans to defined-contribution plans more palatable, they are touting the benefits of choice and are urging employees to "choose the plan that's best for you." This adds some sugar to the otherwise bitter pill of increased out-of- pocket costs associated with these plans, as consumers are encouraged to make "cost- conscious' choices about medical decisions. If efforts to substitute defined contribu- tion plans are successful, and there is no obvi- ous reason why they should not be, they will destroy the social contract on which health in- surance must depend: the willingness of those who do not need much health care to pay for those who do. F OR MANY YEARS Syms, the New York retailer, has successfully used the ad- vertising slogan that "an educated con- sumer is our best customer." In health insur- ance, an educated consumer with a choice of a broad range of health plans would be our worst nightmare-leading to a death spiral of adverse selection and the collapse of employer-sponsored health insurance, which is not exactly the outcome employers and in- surers have in mind. Insurers' 'Remedy' Some in the insurance industry believe that these problems can be avoided through risk adjustment with insurers covering older and higher-risk members receiving higher premi- ums from the employer than those with youn- ger, lower-risk members receive. Unfortu- nately, current risk-adjustment mechanisms are crude at best, and it will be many years be- fore we know whether or not we can risk- adjust effectively for the employed popula 2. tion. Sadly, it is likely that insurers (with the help of their consultants) will game the sys- tem, finding new ways to attract and recruit good risks, so that risk adjustment slows but does not prevent the death spiral of adverse se- lection. Just as accountants will find new tax loopholes, so consultants will find new ways to skim the cream. NOTES 1. A.S. Landa, "Internal Revenue Service Gives OK for Consumer-Directed Health Plans," 29 July 2002, www.ama-assn.org/sci-pubs/amnews/ pick_02/gvsa0729.htm (16 August 2002). H. Darling, Choices and Responsibilities: The Rise of Health Care Consumerism (Hartford, Conn.: Actna Inc., 2002), 3. Ibid., 1. 3. 4. Donald J. Palmisano, president-elect, American Medical Association, as quoted in Landa, "Inter- nal Revenue Service Gives OK." 5. C. Lee and D.L. Rogal, Risk Adjustment: A Key to Changing Incentives in the Health Insurance Market, pre- pared by the Alpha Center under the Robert Wood Johnson Foundation's Changes in Health Care Financing and Organization program, March 1997, hcfo.net/pdf/riskreport.pdf (19 Au- gust 2002). 6. Examples of health insurance markets that began to unravel because of adverse selection in the 1980s and 1990s include the coverage of mental health care in the Federal Employees Health Benefits Program (FEHBP) and the New York State and New Jersey individual in- surance markets. The most relevant example may be the Australian system, in which young Australians did not opt in to subsidize health care for the old. In these cases, governments in- tervened to prevent the systems collapse. Program Evaluation Report, Office of the Legislative Auditor, State of Minnesota (February 2002), 17-82. 7. If the employer health insurance market be- gins to unravel because of adverse selection and defined contribution, presumably the gov ernment would intervene to prevent its col- lapse. But that intervention might necessitate abandoning much of the "consumer-driven, choose what's best for you" ethic that is so popular with the advocates of a defined- contribution approach to health insurance. Consumers Union, "Medicare Medical Savings Accounts: Cherry Picking the Healthy Driving Up Medicare Costs for the Ill," Fact Sheet, 6 May 1997, www.consumersunion.org/health/ msa-picking htm (16 August 2002). 8. National Center for Policy Analysis, "Federal Employee Health Plan: Model for Reform," Brief Analysis no. 107 (Washington: NCPA, 13 June 1994); and L. Tooman, "New Jersey's Health In- surance Disaster, Health Care News (Chicago: Heartland Institute, July 2001). 1. What is the debate highlighted in the paper? 2. What does consumer empowerment mean in the context this paper? Why is it deceptive? 3. What is a death spiral and why and how does it occur? How And Why The Health Insurance System Will Collapse Consumer choice is ultimately bad when it comes to health insurance. by Humphrey Taylor ABSTRACT: The advocates of defined-contribution health plans extol the virtues of con- sumer-driven health care, consumer choice, and empowered consumers as solutions to the problems-particularly the rapidly growing costs-of employer-sponsored health benefits. This paper argues that the widespread use of defined-contribution plans, with more con- sumer choice and more knowledgeable consumers, will lead to the erosion of the social contract on which health insurance must be based, with healthier employees subsidizing the care of older and sicker ones, and a death spiral of adverse selection. If unchecked by government intervention, these trends will lead to the collapse of employer-sponsored health insurance. NSURANCE IS A WAY of risk. It works if the many subsidize the few. Peo- ple whose do not burn down pay for the losses of those whose houses go up in flames. People with insurance whose cars do not crash pay for the repair or replacement of the crashed cars. In health insurance, the healthy pay for the care needed by the sick. contribution plans (while using the words rather loosely) talk about the empowerment of consumers, because consumers can choose the health plan best suited to their own needs. This trend toward more "consumer-driven" health insurance sounds wonderful. We like to have choices. One size does not fit all. Choice promotes competition between health plans The health insurance industry, and espe- and therefore improvements in quality and ef- cially employer-sponsored insurance, is buzz ficiency and better prices. Choice and compe- ing with words and phrases such as "consum-tition are all-American marketplace values. So erism," "empowerment," and "choice." There are reports that "this year has seen a surge in employer interest in offering consumer- directed health plans... particularly now that the Internal Revenue Service has provided clear guidelines for establishing such plans" and that "this trend is expected to accelerate." According to Helen Darling. "We are moving from a defined benefits model to a much more consumer-driven and more substantially consumer-financed model."2 Proponents of this trend toward defined surely consumer-driven health care must be good. It is particularly popular with many Re- publican legislators, who want to promote this model for both employer-sponsored insurance and Medicare. But words can deceive, particularly words that sound good and are used to sell us some- thing. During the Cold War the names of many communist-front organizations included the word "peace." Organizations using the word "freedom" are often conservative organizations working for lower taxes or less regulation. In health care, several organizations using the word "quality" were set up by drug companies, insurers, or physicians to fight government funded health insurance and to protect their incomes and profits. So we should be careful before we assume that "choice" in health insur- ance or "consumer-driven" health plans are a good thing. Voltaire wrote that the Holy Ro- man Empire was not holy, not Roman, and not an empire. But it sounded great. Acting On What We Know The fundamental problem with the current trend to- ward consumer choice of health plans is that we know our health status and can make a reasonably good esti- mate of how likely we are to need much health care in the next year. We don't know if our houses will burn down or if we will crash our cars, so we willingly buy in surance to protect ourselves against something that we know may happen but is unlikely. For these types of insurance we recognize and ac- cept that the fortunate majority pays to subsi- dize the unfortunate minority. "In health insurance, an educated consumer with a choice of plans would be our worst nightmare." But insurance doesn't work if informed buyers can predict the future. If we had a better idea of whether or not our houses would burn down, we would buy more or less insur- ance. And of course the insurers would want to insure the good risks but not those whose houses were likely to catch fire. sicker people. Assumptions of the young and healthy. The young and the healthy, on the other hand, will assume, rightly, that their chances of needing expensive medical care are much lower. If they behave rationally, they will choose plans with coverage for "catastrophic" or unexpected accidents or diseases but not for the routine care of chronic conditions or diseases that mainly affect older people. If people with choices behave this way- and people in general are rational economic animals, so they should the young and healthy will no longer subsidize the cost of care for the old and sick. It would be as if those whose houses do not burn down stopped paying for the losses of those whose houses did-what insur ers call "adverse selection." I Assumptions of older persons. When it comes to our health status, we are (com- pared with our "fire status") reasonably well informed. We know if we need regular drugs for high blood pressure, high cholesterol, or ar thritis or if we are diabetic. We know if we have been diagnosed with cancer or our spouse with Alzheimer's disease and that it will be expensive to treat these diseases. We know that as we get older the chances of get ting many diseases increase. So, if we are likely to need expensive care, we will choose health plans with generous benefits even if they cost a bit more and so will millions of other older. Rationality And The Social Contract There are three reasons why this seems likely to happen. I have mentioned one, the trend toward defined-contribution health plans, with consumers being given more choices of different plans. Another reason is that consumers (insured workers), while still woefully ignorant about the benefits and costs of various plans, are becoming "more knowl- edgeable about medical care and are getting smarter every day and better able, therefore, to choose the plans that are better for them. A third reason is that employers and insurers (which offer "consumer-directed" plans) are encouraging consumer choice. To make the trend away from more generous traditional health plans to defined-contribution plans more palatable, they are touting the benefits of choice and are urging employees to "choose the plan that's best for you." This adds some sugar to the otherwise bitter pill of increased out-of- pocket costs associated with these plans, as consumers are encouraged to make "cost- conscious' choices about medical decisions. If efforts to substitute defined contribu- tion plans are successful, and there is no obvi- ous reason why they should not be, they will destroy the social contract on which health in- surance must depend: the willingness of those who do not need much health care to pay for those who do. F OR MANY YEARS Syms, the New York retailer, has successfully used the ad- vertising slogan that "an educated con- sumer is our best customer." In health insur- ance, an educated consumer with a choice of a broad range of health plans would be our worst nightmare-leading to a death spiral of adverse selection and the collapse of employer-sponsored health insurance, which is not exactly the outcome employers and in- surers have in mind. Insurers' 'Remedy' Some in the insurance industry believe that these problems can be avoided through risk adjustment with insurers covering older and higher-risk members receiving higher premi- ums from the employer than those with youn- ger, lower-risk members receive. Unfortu- nately, current risk-adjustment mechanisms are crude at best, and it will be many years be- fore we know whether or not we can risk- adjust effectively for the employed popula 2. tion. Sadly, it is likely that insurers (with the help of their consultants) will game the sys- tem, finding new ways to attract and recruit good risks, so that risk adjustment slows but does not prevent the death spiral of adverse se- lection. Just as accountants will find new tax loopholes, so consultants will find new ways to skim the cream. NOTES 1. A.S. Landa, "Internal Revenue Service Gives OK for Consumer-Directed Health Plans," 29 July 2002, www.ama-assn.org/sci-pubs/amnews/ pick_02/gvsa0729.htm (16 August 2002). H. Darling, Choices and Responsibilities: The Rise of Health Care Consumerism (Hartford, Conn.: Actna Inc., 2002), 3. Ibid., 1. 3. 4. Donald J. Palmisano, president-elect, American Medical Association, as quoted in Landa, "Inter- nal Revenue Service Gives OK." 5. C. Lee and D.L. Rogal, Risk Adjustment: A Key to Changing Incentives in the Health Insurance Market, pre- pared by the Alpha Center under the Robert Wood Johnson Foundation's Changes in Health Care Financing and Organization program, March 1997, hcfo.net/pdf/riskreport.pdf (19 Au- gust 2002). 6. Examples of health insurance markets that began to unravel because of adverse selection in the 1980s and 1990s include the coverage of mental health care in the Federal Employees Health Benefits Program (FEHBP) and the New York State and New Jersey individual in- surance markets. The most relevant example may be the Australian system, in which young Australians did not opt in to subsidize health care for the old. In these cases, governments in- tervened to prevent the systems collapse. Program Evaluation Report, Office of the Legislative Auditor, State of Minnesota (February 2002), 17-82. 7. If the employer health insurance market be- gins to unravel because of adverse selection and defined contribution, presumably the gov ernment would intervene to prevent its col- lapse. But that intervention might necessitate abandoning much of the "consumer-driven, choose what's best for you" ethic that is so popular with the advocates of a defined- contribution approach to health insurance. Consumers Union, "Medicare Medical Savings Accounts: Cherry Picking the Healthy Driving Up Medicare Costs for the Ill," Fact Sheet, 6 May 1997, www.consumersunion.org/health/ msa-picking htm (16 August 2002). 8. National Center for Policy Analysis, "Federal Employee Health Plan: Model for Reform," Brief Analysis no. 107 (Washington: NCPA, 13 June 1994); and L. Tooman, "New Jersey's Health In- surance Disaster, Health Care News (Chicago: Heartland Institute, July 2001).

Expert Answer:

Answer rating: 100% (QA)

1 Debate Highlighted The debate highlighted in the paper revolves around the impact of consumerdriven health care particularly the widespread use of d... View the full answer

Related Book For

Posted Date:

Students also viewed these economics questions

-

BIO Corporation is a private corporation and as such has no public price for its stock. BIO has 750,000 shares of stock outstanding and its recent net earnings were $1,575,000. It competes against...

-

Pepsin is the principal digestive enzyme of gastric juice. A 1.40 g sample of pepsin is dissolved in enough water to make 4.50 mL of solution. The osmotic pressure of the solution is found to be...

-

The following data were accumulated for use in reconciling the bank account of Mathers Co. for July: 1. Cash balance according to the company's records at July 31, $32,110. 2. Cash balance according...

-

Murray Inc. manufactures bicycle frames in two departments: Cutting and Welding. Murray uses the weighted average method. Manufacturing costs are added uniformly throughout the process. The following...

-

Two blocks are tied together by a cord draped over a pulley (Figure P8.43). (a) At first, the block on the table does not slip. How does the tension in the cord compare with the gravitational force...

-

Sulfuric acid is the chemical produced in the United States with the highest volume of production. In one of the earliest processes used to make it, an ore containing iron pyrites (FeS 2 ) is roasted...

-

please Draw a deployment diagram of your system convert this photoComponent diagram. to deployment diagram in software engineering please draw and explain this . Patient Registration (Signup/login)...

-

Make a complexity analysis of string searching algorithms and identify which one performs efficiently in worst case. Also justify your answer.

-

The capital structure of a publicly traded company contains a single debt issue with the following characteristics: Fixed coupon-paying bond issue (semiannual pay) Par value: $80 million Coupon rate:...

-

A regulatory specialist may be tasked with presenting regulatory information on provider and patient rights in a way that all department employees and patients will understand the importance of...

-

The graph to the right depicts an economy, Home, which produces flowers and soybeans. Its production possibilities frontier is shown as TT. One of Home's isovalue lines is also shown as VV. Home...

-

Required: Calculate the covariance Invest 50% of your money in Asset A and 50% in B State of the economy Boom Bust Probability A return B return 0,4 20% 15% 0,6 -10% 9%

-

Being able to identify, create, and mess up arguments teaches so many useful lessons in thinking that we're going to give it the time it needs. Please answer the following questions fully and...

-

Explain briefly the 7-S framework for project management?

-

Give codons for the following amino acids: (a) Th (b) Asp (c) Thr

-

What aspects of complexity are assisted by the use of computer-aided project planning and which are not?

-

Describe the major elements of cost in a proposal to: (a) Implement a new computer system for the administration of a college or university (b) Construct a new theme park (c) Introduce a new range of...

-

Why is getting scope sign-off so important?

-

Using the economic balance sheet approach, the Laws economic net worth is closest to: A. $925,000. B. $1,425,000. C. $1,675,000. Raye uses a costbenefit approach to rebalancing and recommends that...

-

Using an economic balance sheet, which of the Laws current financial assets is most concerning from an asset allocation perspective? A. Equities B. Real estate C. Fixed income Raye uses a costbenefit...

-

To address his concern regarding the previous advisers asset allocation approach, Raye should assess the Laws portfolio using: A. a homogeneous and mutually exclusive asset classbased risk analysis....

Study smarter with the SolutionInn App