Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

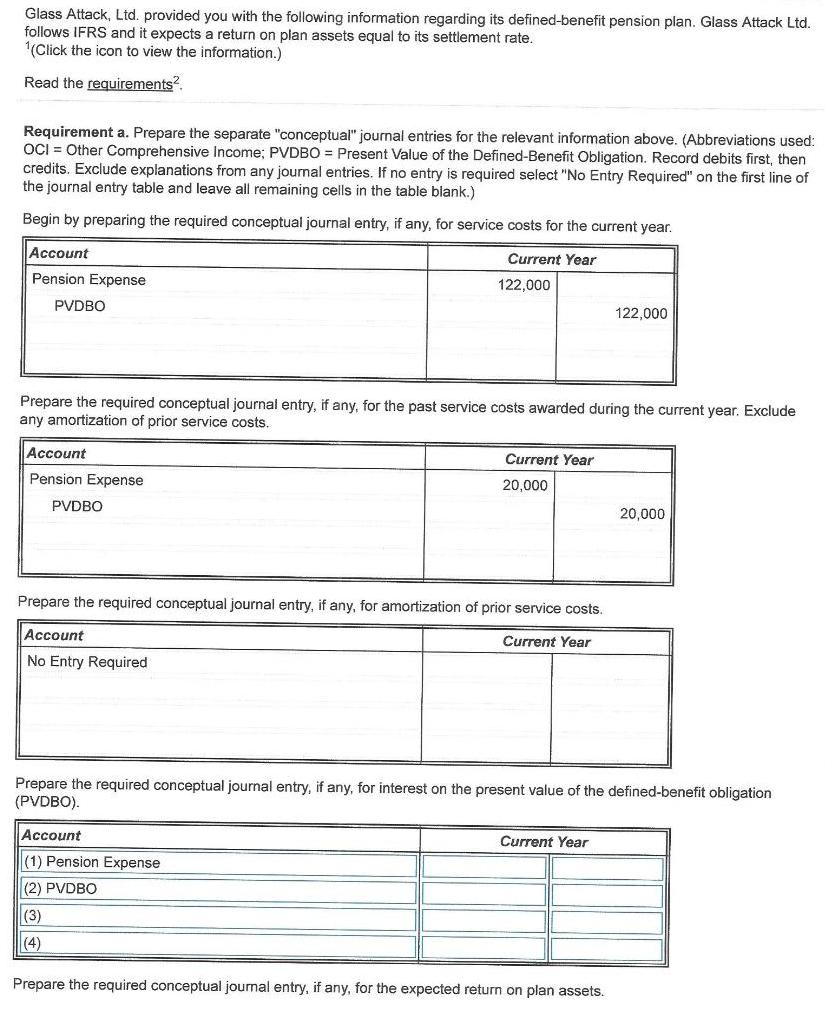

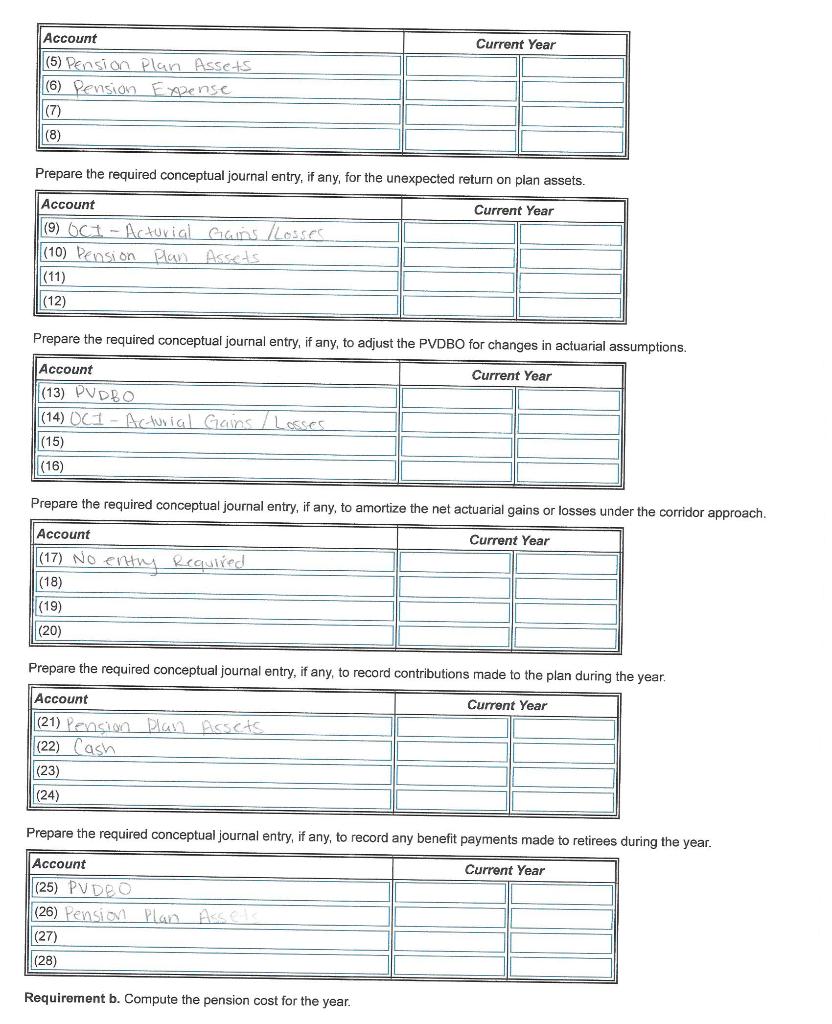

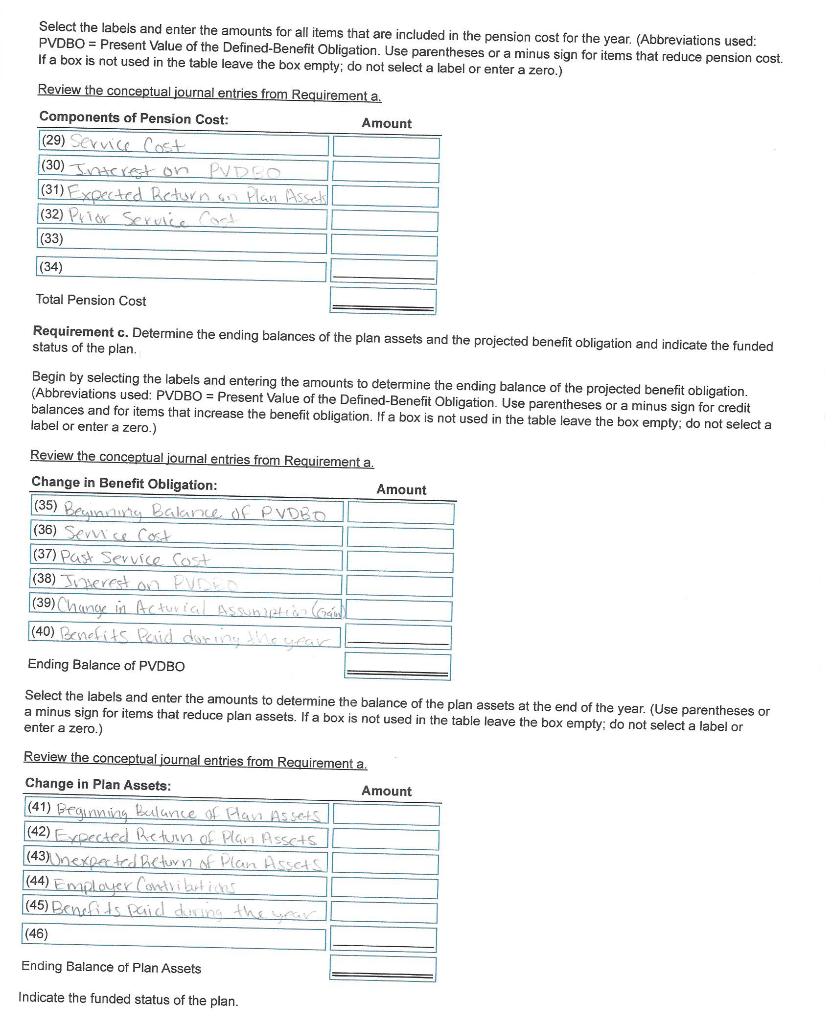

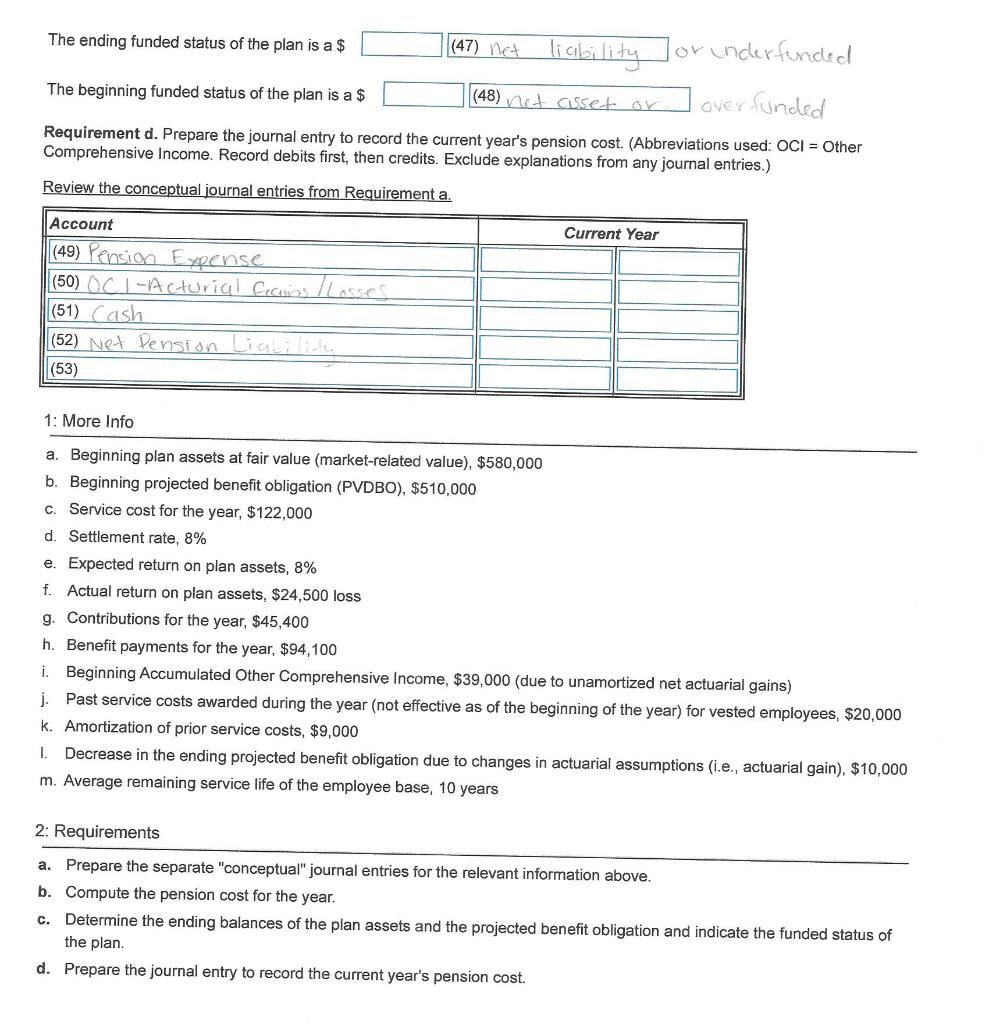

Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack Ltd. follows IFRS and it expects a return on plan assets equal to its settlement rate. 1(Click the icon to view the information.) Read the requirements². Requirement a. Prepare the separate "conceptual" journal entries for the relevant information above. (Abbreviations used: OCI = Other Comprehensive Income; PVDBO = Present Value of the Defined-Benefit Obligation. Record debits first, then credits. Exclude explanations from any journal entries. If no entry is required select "No Entry Required" on the first line of the journal entry table and leave all remaining cells in the table blank.) Begin by preparing the required conceptual journal entry, if any, for service costs for the current year. Account Pension Expense PVDBO Account Pension Expense Current Year PVDBO 122,000 Prepare the required conceptual journal entry, if any, for the past service costs awarded during the current year. Exclude any amortization of prior service costs. Current Year 20,000 Prepare the required conceptual journal entry, if any, for amortization of prior service costs. Account Current Year No Entry Required 122,000 Current Year Prepare the required conceptual journal entry, if any, for interest on the present value of the defined-benefit obligation (PVDBO). Account (1) Pension Expense (2) PVDBO (3) (4) Prepare the required conceptual journal entry, if any, for the expected return on plan assets. 20,000 Account (5) Pension Plan Assets (6) Pension Expense (7) (8) Prepare the required conceptual journal entry, if any, for the unexpected return on plan assets. Account Current Year (9) OCI - Acturial Gains / Losses (10) Pension Plan Assets. (11) (12) Prepare the required conceptual journal entry, if any, to adjust the PVDBO for changes in actuarial assumptions. Account Current Year (13) PVDBO (14) OCI - Acturial Gains / Losses (15) (16) Current Year Prepare the required conceptual journal entry, if any, to amortize the net actuarial gains or losses under the corridor approach. Account Current Year (17) No entry Required (18) (19) (20) Prepare the required conceptual journal entry, if any, to record contributions made to the plan during the year. Current Year Account (21) Pension Plan Assets (22) Cash (23) (24) Prepare the required conceptual journal entry, if any, to record any benefit payments made to retirees during the year. Current Year Account (25) PVDBO (26) Pension Plan Assels. (27) (28) Requirement b. Compute the pension cost for the year. Select the labels and enter the amounts for all items that are included in the pension cost for the year. (Abbreviations used: PVDBO Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for items that reduce pension cost. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Components of Pension Cost: Amount (29) Service Cost (30) Interest on PYDEO (31) Expected Return on Plan Assels (32) Prior Service Cart (33) (34) Total Pension Cost Requirement c. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. Begin by selecting the labels and entering the amounts to determine the ending balance of the projected benefit obligation. (Abbreviations used: PVDBO = Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for credit balances and for items that increase the benefit obligation. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Change in Benefit Obligation: (35) Beginning Balance of PVD BO (36) Service Cost (37) Past Service Cost (38) Interest on PUDEO (39) Change in Acturial Assumption (Gran)) (40) Benefits Paid during the year Ending Balance of PVDBO Select the labels and enter the amounts to determine the balance of the plan assets at the end of the year. (Use parentheses or a minus sign for items that reduce plan assets. If a box is not used in the table leave the box empty; do not selecta enter a zero.) label or Review the conceptual journal entries from Requirement a Change in Plan Assets: (41) Beginning Balance of Plan Assets (42) Expected Return of Plan Assets (43)Unexpected Return of Plan Assets Amount (44) Employer Contributions (45) Benefits paid during the year (46) Ending Balance of Plan Assets Indicate the funded status of the plan. Amount The ending funded status of the plan is a $ (47) net liability or underfunded over funded (48) not cisset or The beginning funded status of the plan is a $ Requirement d. Prepare the journal entry to record the current year's pension cost. (Abbreviations used: OCI = Other Comprehensive Income. Record debits first, then credits. Exclude explanations from any journal entries.) Review the conceptual journal entries from Requirement a. Account (49) Pension Expense (50) (C1-Acturial Grains / Lasses (51) Cash (52) Net Pension Liability (53) 1: More Info a. Beginning plan assets at fair value (market-related value), $580,000 b. Beginning projected benefit obligation (PVDBO), $510,000 c. Service cost for the year, $122,000 d. Settlement rate, 8% e. Expected return on plan assets, 8% f. Actual return on plan assets, $24,500 loss Current Year g. Contributions for the year, $45,400 h. Benefit payments for the year, $94,100 i. Beginning Accumulated Other Comprehensive Income, $39,000 (due to unamortized net actuarial gains) j. Past service costs awarded during the year (not effective as of the beginning of the year) for vested employees, $20,000 k. Amortization of prior service costs, $9,000 1. Decrease in the ending projected benefit obligation due to changes in actuarial assumptions (i.e., actuarial gain), $10,000 m. Average remaining service life of the employee base, 10 years 2: Requirements a. Prepare the separate "conceptual" journal entries for the relevant information above. b. Compute the pension cost for the year. C. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. d. Prepare the journal entry to record the current year's pension cost. Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack Ltd. follows IFRS and it expects a return on plan assets equal to its settlement rate. 1(Click the icon to view the information.) Read the requirements². Requirement a. Prepare the separate "conceptual" journal entries for the relevant information above. (Abbreviations used: OCI = Other Comprehensive Income; PVDBO = Present Value of the Defined-Benefit Obligation. Record debits first, then credits. Exclude explanations from any journal entries. If no entry is required select "No Entry Required" on the first line of the journal entry table and leave all remaining cells in the table blank.) Begin by preparing the required conceptual journal entry, if any, for service costs for the current year. Account Pension Expense PVDBO Account Pension Expense Current Year PVDBO 122,000 Prepare the required conceptual journal entry, if any, for the past service costs awarded during the current year. Exclude any amortization of prior service costs. Current Year 20,000 Prepare the required conceptual journal entry, if any, for amortization of prior service costs. Account Current Year No Entry Required 122,000 Current Year Prepare the required conceptual journal entry, if any, for interest on the present value of the defined-benefit obligation (PVDBO). Account (1) Pension Expense (2) PVDBO (3) (4) Prepare the required conceptual journal entry, if any, for the expected return on plan assets. 20,000 Account (5) Pension Plan Assets (6) Pension Expense (7) (8) Prepare the required conceptual journal entry, if any, for the unexpected return on plan assets. Account Current Year (9) OCI - Acturial Gains / Losses (10) Pension Plan Assets. (11) (12) Prepare the required conceptual journal entry, if any, to adjust the PVDBO for changes in actuarial assumptions. Account Current Year (13) PVDBO (14) OCI - Acturial Gains / Losses (15) (16) Current Year Prepare the required conceptual journal entry, if any, to amortize the net actuarial gains or losses under the corridor approach. Account Current Year (17) No entry Required (18) (19) (20) Prepare the required conceptual journal entry, if any, to record contributions made to the plan during the year. Current Year Account (21) Pension Plan Assets (22) Cash (23) (24) Prepare the required conceptual journal entry, if any, to record any benefit payments made to retirees during the year. Current Year Account (25) PVDBO (26) Pension Plan Assels. (27) (28) Requirement b. Compute the pension cost for the year. Select the labels and enter the amounts for all items that are included in the pension cost for the year. (Abbreviations used: PVDBO Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for items that reduce pension cost. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Components of Pension Cost: Amount (29) Service Cost (30) Interest on PYDEO (31) Expected Return on Plan Assels (32) Prior Service Cart (33) (34) Total Pension Cost Requirement c. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. Begin by selecting the labels and entering the amounts to determine the ending balance of the projected benefit obligation. (Abbreviations used: PVDBO = Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for credit balances and for items that increase the benefit obligation. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Change in Benefit Obligation: (35) Beginning Balance of PVD BO (36) Service Cost (37) Past Service Cost (38) Interest on PUDEO (39) Change in Acturial Assumption (Gran)) (40) Benefits Paid during the year Ending Balance of PVDBO Select the labels and enter the amounts to determine the balance of the plan assets at the end of the year. (Use parentheses or a minus sign for items that reduce plan assets. If a box is not used in the table leave the box empty; do not selecta enter a zero.) label or Review the conceptual journal entries from Requirement a Change in Plan Assets: (41) Beginning Balance of Plan Assets (42) Expected Return of Plan Assets (43)Unexpected Return of Plan Assets Amount (44) Employer Contributions (45) Benefits paid during the year (46) Ending Balance of Plan Assets Indicate the funded status of the plan. Amount The ending funded status of the plan is a $ (47) net liability or underfunded over funded (48) not cisset or The beginning funded status of the plan is a $ Requirement d. Prepare the journal entry to record the current year's pension cost. (Abbreviations used: OCI = Other Comprehensive Income. Record debits first, then credits. Exclude explanations from any journal entries.) Review the conceptual journal entries from Requirement a. Account (49) Pension Expense (50) (C1-Acturial Grains / Lasses (51) Cash (52) Net Pension Liability (53) 1: More Info a. Beginning plan assets at fair value (market-related value), $580,000 b. Beginning projected benefit obligation (PVDBO), $510,000 c. Service cost for the year, $122,000 d. Settlement rate, 8% e. Expected return on plan assets, 8% f. Actual return on plan assets, $24,500 loss Current Year g. Contributions for the year, $45,400 h. Benefit payments for the year, $94,100 i. Beginning Accumulated Other Comprehensive Income, $39,000 (due to unamortized net actuarial gains) j. Past service costs awarded during the year (not effective as of the beginning of the year) for vested employees, $20,000 k. Amortization of prior service costs, $9,000 1. Decrease in the ending projected benefit obligation due to changes in actuarial assumptions (i.e., actuarial gain), $10,000 m. Average remaining service life of the employee base, 10 years 2: Requirements a. Prepare the separate "conceptual" journal entries for the relevant information above. b. Compute the pension cost for the year. C. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. d. Prepare the journal entry to record the current year's pension cost. Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack Ltd. follows IFRS and it expects a return on plan assets equal to its settlement rate. 1(Click the icon to view the information.) Read the requirements². Requirement a. Prepare the separate "conceptual" journal entries for the relevant information above. (Abbreviations used: OCI = Other Comprehensive Income; PVDBO = Present Value of the Defined-Benefit Obligation. Record debits first, then credits. Exclude explanations from any journal entries. If no entry is required select "No Entry Required" on the first line of the journal entry table and leave all remaining cells in the table blank.) Begin by preparing the required conceptual journal entry, if any, for service costs for the current year. Account Pension Expense PVDBO Account Pension Expense Current Year PVDBO 122,000 Prepare the required conceptual journal entry, if any, for the past service costs awarded during the current year. Exclude any amortization of prior service costs. Current Year 20,000 Prepare the required conceptual journal entry, if any, for amortization of prior service costs. Account Current Year No Entry Required 122,000 Current Year Prepare the required conceptual journal entry, if any, for interest on the present value of the defined-benefit obligation (PVDBO). Account (1) Pension Expense (2) PVDBO (3) (4) Prepare the required conceptual journal entry, if any, for the expected return on plan assets. 20,000 Account (5) Pension Plan Assets (6) Pension Expense (7) (8) Prepare the required conceptual journal entry, if any, for the unexpected return on plan assets. Account Current Year (9) OCI - Acturial Gains / Losses (10) Pension Plan Assets. (11) (12) Prepare the required conceptual journal entry, if any, to adjust the PVDBO for changes in actuarial assumptions. Account Current Year (13) PVDBO (14) OCI - Acturial Gains / Losses (15) (16) Current Year Prepare the required conceptual journal entry, if any, to amortize the net actuarial gains or losses under the corridor approach. Account Current Year (17) No entry Required (18) (19) (20) Prepare the required conceptual journal entry, if any, to record contributions made to the plan during the year. Current Year Account (21) Pension Plan Assets (22) Cash (23) (24) Prepare the required conceptual journal entry, if any, to record any benefit payments made to retirees during the year. Current Year Account (25) PVDBO (26) Pension Plan Assels. (27) (28) Requirement b. Compute the pension cost for the year. Select the labels and enter the amounts for all items that are included in the pension cost for the year. (Abbreviations used: PVDBO Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for items that reduce pension cost. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Components of Pension Cost: Amount (29) Service Cost (30) Interest on PYDEO (31) Expected Return on Plan Assels (32) Prior Service Cart (33) (34) Total Pension Cost Requirement c. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. Begin by selecting the labels and entering the amounts to determine the ending balance of the projected benefit obligation. (Abbreviations used: PVDBO = Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for credit balances and for items that increase the benefit obligation. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Change in Benefit Obligation: (35) Beginning Balance of PVD BO (36) Service Cost (37) Past Service Cost (38) Interest on PUDEO (39) Change in Acturial Assumption (Gran)) (40) Benefits Paid during the year Ending Balance of PVDBO Select the labels and enter the amounts to determine the balance of the plan assets at the end of the year. (Use parentheses or a minus sign for items that reduce plan assets. If a box is not used in the table leave the box empty; do not selecta enter a zero.) label or Review the conceptual journal entries from Requirement a Change in Plan Assets: (41) Beginning Balance of Plan Assets (42) Expected Return of Plan Assets (43)Unexpected Return of Plan Assets Amount (44) Employer Contributions (45) Benefits paid during the year (46) Ending Balance of Plan Assets Indicate the funded status of the plan. Amount The ending funded status of the plan is a $ (47) net liability or underfunded over funded (48) not cisset or The beginning funded status of the plan is a $ Requirement d. Prepare the journal entry to record the current year's pension cost. (Abbreviations used: OCI = Other Comprehensive Income. Record debits first, then credits. Exclude explanations from any journal entries.) Review the conceptual journal entries from Requirement a. Account (49) Pension Expense (50) (C1-Acturial Grains / Lasses (51) Cash (52) Net Pension Liability (53) 1: More Info a. Beginning plan assets at fair value (market-related value), $580,000 b. Beginning projected benefit obligation (PVDBO), $510,000 c. Service cost for the year, $122,000 d. Settlement rate, 8% e. Expected return on plan assets, 8% f. Actual return on plan assets, $24,500 loss Current Year g. Contributions for the year, $45,400 h. Benefit payments for the year, $94,100 i. Beginning Accumulated Other Comprehensive Income, $39,000 (due to unamortized net actuarial gains) j. Past service costs awarded during the year (not effective as of the beginning of the year) for vested employees, $20,000 k. Amortization of prior service costs, $9,000 1. Decrease in the ending projected benefit obligation due to changes in actuarial assumptions (i.e., actuarial gain), $10,000 m. Average remaining service life of the employee base, 10 years 2: Requirements a. Prepare the separate "conceptual" journal entries for the relevant information above. b. Compute the pension cost for the year. C. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. d. Prepare the journal entry to record the current year's pension cost. Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack Ltd. follows IFRS and it expects a return on plan assets equal to its settlement rate. 1(Click the icon to view the information.) Read the requirements². Requirement a. Prepare the separate "conceptual" journal entries for the relevant information above. (Abbreviations used: OCI = Other Comprehensive Income; PVDBO = Present Value of the Defined-Benefit Obligation. Record debits first, then credits. Exclude explanations from any journal entries. If no entry is required select "No Entry Required" on the first line of the journal entry table and leave all remaining cells in the table blank.) Begin by preparing the required conceptual journal entry, if any, for service costs for the current year. Account Pension Expense PVDBO Account Pension Expense Current Year PVDBO 122,000 Prepare the required conceptual journal entry, if any, for the past service costs awarded during the current year. Exclude any amortization of prior service costs. Current Year 20,000 Prepare the required conceptual journal entry, if any, for amortization of prior service costs. Account Current Year No Entry Required 122,000 Current Year Prepare the required conceptual journal entry, if any, for interest on the present value of the defined-benefit obligation (PVDBO). Account (1) Pension Expense (2) PVDBO (3) (4) Prepare the required conceptual journal entry, if any, for the expected return on plan assets. 20,000 Account (5) Pension Plan Assets (6) Pension Expense (7) (8) Prepare the required conceptual journal entry, if any, for the unexpected return on plan assets. Account Current Year (9) OCI - Acturial Gains / Losses (10) Pension Plan Assets. (11) (12) Prepare the required conceptual journal entry, if any, to adjust the PVDBO for changes in actuarial assumptions. Account Current Year (13) PVDBO (14) OCI - Acturial Gains / Losses (15) (16) Current Year Prepare the required conceptual journal entry, if any, to amortize the net actuarial gains or losses under the corridor approach. Account Current Year (17) No entry Required (18) (19) (20) Prepare the required conceptual journal entry, if any, to record contributions made to the plan during the year. Current Year Account (21) Pension Plan Assets (22) Cash (23) (24) Prepare the required conceptual journal entry, if any, to record any benefit payments made to retirees during the year. Current Year Account (25) PVDBO (26) Pension Plan Assels. (27) (28) Requirement b. Compute the pension cost for the year. Select the labels and enter the amounts for all items that are included in the pension cost for the year. (Abbreviations used: PVDBO Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for items that reduce pension cost. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Components of Pension Cost: Amount (29) Service Cost (30) Interest on PYDEO (31) Expected Return on Plan Assels (32) Prior Service Cart (33) (34) Total Pension Cost Requirement c. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. Begin by selecting the labels and entering the amounts to determine the ending balance of the projected benefit obligation. (Abbreviations used: PVDBO = Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for credit balances and for items that increase the benefit obligation. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Change in Benefit Obligation: (35) Beginning Balance of PVD BO (36) Service Cost (37) Past Service Cost (38) Interest on PUDEO (39) Change in Acturial Assumption (Gran)) (40) Benefits Paid during the year Ending Balance of PVDBO Select the labels and enter the amounts to determine the balance of the plan assets at the end of the year. (Use parentheses or a minus sign for items that reduce plan assets. If a box is not used in the table leave the box empty; do not selecta enter a zero.) label or Review the conceptual journal entries from Requirement a Change in Plan Assets: (41) Beginning Balance of Plan Assets (42) Expected Return of Plan Assets (43)Unexpected Return of Plan Assets Amount (44) Employer Contributions (45) Benefits paid during the year (46) Ending Balance of Plan Assets Indicate the funded status of the plan. Amount The ending funded status of the plan is a $ (47) net liability or underfunded over funded (48) not cisset or The beginning funded status of the plan is a $ Requirement d. Prepare the journal entry to record the current year's pension cost. (Abbreviations used: OCI = Other Comprehensive Income. Record debits first, then credits. Exclude explanations from any journal entries.) Review the conceptual journal entries from Requirement a. Account (49) Pension Expense (50) (C1-Acturial Grains / Lasses (51) Cash (52) Net Pension Liability (53) 1: More Info a. Beginning plan assets at fair value (market-related value), $580,000 b. Beginning projected benefit obligation (PVDBO), $510,000 c. Service cost for the year, $122,000 d. Settlement rate, 8% e. Expected return on plan assets, 8% f. Actual return on plan assets, $24,500 loss Current Year g. Contributions for the year, $45,400 h. Benefit payments for the year, $94,100 i. Beginning Accumulated Other Comprehensive Income, $39,000 (due to unamortized net actuarial gains) j. Past service costs awarded during the year (not effective as of the beginning of the year) for vested employees, $20,000 k. Amortization of prior service costs, $9,000 1. Decrease in the ending projected benefit obligation due to changes in actuarial assumptions (i.e., actuarial gain), $10,000 m. Average remaining service life of the employee base, 10 years 2: Requirements a. Prepare the separate "conceptual" journal entries for the relevant information above. b. Compute the pension cost for the year. C. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. d. Prepare the journal entry to record the current year's pension cost. Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack Ltd. follows IFRS and it expects a return on plan assets equal to its settlement rate. 1(Click the icon to view the information.) Read the requirements². Requirement a. Prepare the separate "conceptual" journal entries for the relevant information above. (Abbreviations used: OCI = Other Comprehensive Income; PVDBO = Present Value of the Defined-Benefit Obligation. Record debits first, then credits. Exclude explanations from any journal entries. If no entry is required select "No Entry Required" on the first line of the journal entry table and leave all remaining cells in the table blank.) Begin by preparing the required conceptual journal entry, if any, for service costs for the current year. Account Pension Expense PVDBO Account Pension Expense Current Year PVDBO 122,000 Prepare the required conceptual journal entry, if any, for the past service costs awarded during the current year. Exclude any amortization of prior service costs. Current Year 20,000 Prepare the required conceptual journal entry, if any, for amortization of prior service costs. Account Current Year No Entry Required 122,000 Current Year Prepare the required conceptual journal entry, if any, for interest on the present value of the defined-benefit obligation (PVDBO). Account (1) Pension Expense (2) PVDBO (3) (4) Prepare the required conceptual journal entry, if any, for the expected return on plan assets. 20,000 Account (5) Pension Plan Assets (6) Pension Expense (7) (8) Prepare the required conceptual journal entry, if any, for the unexpected return on plan assets. Account Current Year (9) OCI - Acturial Gains / Losses (10) Pension Plan Assets. (11) (12) Prepare the required conceptual journal entry, if any, to adjust the PVDBO for changes in actuarial assumptions. Account Current Year (13) PVDBO (14) OCI - Acturial Gains / Losses (15) (16) Current Year Prepare the required conceptual journal entry, if any, to amortize the net actuarial gains or losses under the corridor approach. Account Current Year (17) No entry Required (18) (19) (20) Prepare the required conceptual journal entry, if any, to record contributions made to the plan during the year. Current Year Account (21) Pension Plan Assets (22) Cash (23) (24) Prepare the required conceptual journal entry, if any, to record any benefit payments made to retirees during the year. Current Year Account (25) PVDBO (26) Pension Plan Assels. (27) (28) Requirement b. Compute the pension cost for the year. Select the labels and enter the amounts for all items that are included in the pension cost for the year. (Abbreviations used: PVDBO Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for items that reduce pension cost. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Components of Pension Cost: Amount (29) Service Cost (30) Interest on PYDEO (31) Expected Return on Plan Assels (32) Prior Service Cart (33) (34) Total Pension Cost Requirement c. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. Begin by selecting the labels and entering the amounts to determine the ending balance of the projected benefit obligation. (Abbreviations used: PVDBO = Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for credit balances and for items that increase the benefit obligation. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Change in Benefit Obligation: (35) Beginning Balance of PVD BO (36) Service Cost (37) Past Service Cost (38) Interest on PUDEO (39) Change in Acturial Assumption (Gran)) (40) Benefits Paid during the year Ending Balance of PVDBO Select the labels and enter the amounts to determine the balance of the plan assets at the end of the year. (Use parentheses or a minus sign for items that reduce plan assets. If a box is not used in the table leave the box empty; do not selecta enter a zero.) label or Review the conceptual journal entries from Requirement a Change in Plan Assets: (41) Beginning Balance of Plan Assets (42) Expected Return of Plan Assets (43)Unexpected Return of Plan Assets Amount (44) Employer Contributions (45) Benefits paid during the year (46) Ending Balance of Plan Assets Indicate the funded status of the plan. Amount The ending funded status of the plan is a $ (47) net liability or underfunded over funded (48) not cisset or The beginning funded status of the plan is a $ Requirement d. Prepare the journal entry to record the current year's pension cost. (Abbreviations used: OCI = Other Comprehensive Income. Record debits first, then credits. Exclude explanations from any journal entries.) Review the conceptual journal entries from Requirement a. Account (49) Pension Expense (50) (C1-Acturial Grains / Lasses (51) Cash (52) Net Pension Liability (53) 1: More Info a. Beginning plan assets at fair value (market-related value), $580,000 b. Beginning projected benefit obligation (PVDBO), $510,000 c. Service cost for the year, $122,000 d. Settlement rate, 8% e. Expected return on plan assets, 8% f. Actual return on plan assets, $24,500 loss Current Year g. Contributions for the year, $45,400 h. Benefit payments for the year, $94,100 i. Beginning Accumulated Other Comprehensive Income, $39,000 (due to unamortized net actuarial gains) j. Past service costs awarded during the year (not effective as of the beginning of the year) for vested employees, $20,000 k. Amortization of prior service costs, $9,000 1. Decrease in the ending projected benefit obligation due to changes in actuarial assumptions (i.e., actuarial gain), $10,000 m. Average remaining service life of the employee base, 10 years 2: Requirements a. Prepare the separate "conceptual" journal entries for the relevant information above. b. Compute the pension cost for the year. C. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. d. Prepare the journal entry to record the current year's pension cost. Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack Ltd. follows IFRS and it expects a return on plan assets equal to its settlement rate. 1(Click the icon to view the information.) Read the requirements². Requirement a. Prepare the separate "conceptual" journal entries for the relevant information above. (Abbreviations used: OCI = Other Comprehensive Income; PVDBO = Present Value of the Defined-Benefit Obligation. Record debits first, then credits. Exclude explanations from any journal entries. If no entry is required select "No Entry Required" on the first line of the journal entry table and leave all remaining cells in the table blank.) Begin by preparing the required conceptual journal entry, if any, for service costs for the current year. Account Pension Expense PVDBO Account Pension Expense Current Year PVDBO 122,000 Prepare the required conceptual journal entry, if any, for the past service costs awarded during the current year. Exclude any amortization of prior service costs. Current Year 20,000 Prepare the required conceptual journal entry, if any, for amortization of prior service costs. Account Current Year No Entry Required 122,000 Current Year Prepare the required conceptual journal entry, if any, for interest on the present value of the defined-benefit obligation (PVDBO). Account (1) Pension Expense (2) PVDBO (3) (4) Prepare the required conceptual journal entry, if any, for the expected return on plan assets. 20,000 Account (5) Pension Plan Assets (6) Pension Expense (7) (8) Prepare the required conceptual journal entry, if any, for the unexpected return on plan assets. Account Current Year (9) OCI - Acturial Gains / Losses (10) Pension Plan Assets. (11) (12) Prepare the required conceptual journal entry, if any, to adjust the PVDBO for changes in actuarial assumptions. Account Current Year (13) PVDBO (14) OCI - Acturial Gains / Losses (15) (16) Current Year Prepare the required conceptual journal entry, if any, to amortize the net actuarial gains or losses under the corridor approach. Account Current Year (17) No entry Required (18) (19) (20) Prepare the required conceptual journal entry, if any, to record contributions made to the plan during the year. Current Year Account (21) Pension Plan Assets (22) Cash (23) (24) Prepare the required conceptual journal entry, if any, to record any benefit payments made to retirees during the year. Current Year Account (25) PVDBO (26) Pension Plan Assels. (27) (28) Requirement b. Compute the pension cost for the year. Select the labels and enter the amounts for all items that are included in the pension cost for the year. (Abbreviations used: PVDBO Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for items that reduce pension cost. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Components of Pension Cost: Amount (29) Service Cost (30) Interest on PYDEO (31) Expected Return on Plan Assels (32) Prior Service Cart (33) (34) Total Pension Cost Requirement c. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. Begin by selecting the labels and entering the amounts to determine the ending balance of the projected benefit obligation. (Abbreviations used: PVDBO = Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for credit balances and for items that increase the benefit obligation. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Change in Benefit Obligation: (35) Beginning Balance of PVD BO (36) Service Cost (37) Past Service Cost (38) Interest on PUDEO (39) Change in Acturial Assumption (Gran)) (40) Benefits Paid during the year Ending Balance of PVDBO Select the labels and enter the amounts to determine the balance of the plan assets at the end of the year. (Use parentheses or a minus sign for items that reduce plan assets. If a box is not used in the table leave the box empty; do not selecta enter a zero.) label or Review the conceptual journal entries from Requirement a Change in Plan Assets: (41) Beginning Balance of Plan Assets (42) Expected Return of Plan Assets (43)Unexpected Return of Plan Assets Amount (44) Employer Contributions (45) Benefits paid during the year (46) Ending Balance of Plan Assets Indicate the funded status of the plan. Amount The ending funded status of the plan is a $ (47) net liability or underfunded over funded (48) not cisset or The beginning funded status of the plan is a $ Requirement d. Prepare the journal entry to record the current year's pension cost. (Abbreviations used: OCI = Other Comprehensive Income. Record debits first, then credits. Exclude explanations from any journal entries.) Review the conceptual journal entries from Requirement a. Account (49) Pension Expense (50) (C1-Acturial Grains / Lasses (51) Cash (52) Net Pension Liability (53) 1: More Info a. Beginning plan assets at fair value (market-related value), $580,000 b. Beginning projected benefit obligation (PVDBO), $510,000 c. Service cost for the year, $122,000 d. Settlement rate, 8% e. Expected return on plan assets, 8% f. Actual return on plan assets, $24,500 loss Current Year g. Contributions for the year, $45,400 h. Benefit payments for the year, $94,100 i. Beginning Accumulated Other Comprehensive Income, $39,000 (due to unamortized net actuarial gains) j. Past service costs awarded during the year (not effective as of the beginning of the year) for vested employees, $20,000 k. Amortization of prior service costs, $9,000 1. Decrease in the ending projected benefit obligation due to changes in actuarial assumptions (i.e., actuarial gain), $10,000 m. Average remaining service life of the employee base, 10 years 2: Requirements a. Prepare the separate "conceptual" journal entries for the relevant information above. b. Compute the pension cost for the year. C. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. d. Prepare the journal entry to record the current year's pension cost. Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack Ltd. follows IFRS and it expects a return on plan assets equal to its settlement rate. 1(Click the icon to view the information.) Read the requirements². Requirement a. Prepare the separate "conceptual" journal entries for the relevant information above. (Abbreviations used: OCI = Other Comprehensive Income; PVDBO = Present Value of the Defined-Benefit Obligation. Record debits first, then credits. Exclude explanations from any journal entries. If no entry is required select "No Entry Required" on the first line of the journal entry table and leave all remaining cells in the table blank.) Begin by preparing the required conceptual journal entry, if any, for service costs for the current year. Account Pension Expense PVDBO Account Pension Expense Current Year PVDBO 122,000 Prepare the required conceptual journal entry, if any, for the past service costs awarded during the current year. Exclude any amortization of prior service costs. Current Year 20,000 Prepare the required conceptual journal entry, if any, for amortization of prior service costs. Account Current Year No Entry Required 122,000 Current Year Prepare the required conceptual journal entry, if any, for interest on the present value of the defined-benefit obligation (PVDBO). Account (1) Pension Expense (2) PVDBO (3) (4) Prepare the required conceptual journal entry, if any, for the expected return on plan assets. 20,000 Account (5) Pension Plan Assets (6) Pension Expense (7) (8) Prepare the required conceptual journal entry, if any, for the unexpected return on plan assets. Account Current Year (9) OCI - Acturial Gains / Losses (10) Pension Plan Assets. (11) (12) Prepare the required conceptual journal entry, if any, to adjust the PVDBO for changes in actuarial assumptions. Account Current Year (13) PVDBO (14) OCI - Acturial Gains / Losses (15) (16) Current Year Prepare the required conceptual journal entry, if any, to amortize the net actuarial gains or losses under the corridor approach. Account Current Year (17) No entry Required (18) (19) (20) Prepare the required conceptual journal entry, if any, to record contributions made to the plan during the year. Current Year Account (21) Pension Plan Assets (22) Cash (23) (24) Prepare the required conceptual journal entry, if any, to record any benefit payments made to retirees during the year. Current Year Account (25) PVDBO (26) Pension Plan Assels. (27) (28) Requirement b. Compute the pension cost for the year. Select the labels and enter the amounts for all items that are included in the pension cost for the year. (Abbreviations used: PVDBO Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for items that reduce pension cost. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Components of Pension Cost: Amount (29) Service Cost (30) Interest on PYDEO (31) Expected Return on Plan Assels (32) Prior Service Cart (33) (34) Total Pension Cost Requirement c. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. Begin by selecting the labels and entering the amounts to determine the ending balance of the projected benefit obligation. (Abbreviations used: PVDBO = Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for credit balances and for items that increase the benefit obligation. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Change in Benefit Obligation: (35) Beginning Balance of PVD BO (36) Service Cost (37) Past Service Cost (38) Interest on PUDEO (39) Change in Acturial Assumption (Gran)) (40) Benefits Paid during the year Ending Balance of PVDBO Select the labels and enter the amounts to determine the balance of the plan assets at the end of the year. (Use parentheses or a minus sign for items that reduce plan assets. If a box is not used in the table leave the box empty; do not selecta enter a zero.) label or Review the conceptual journal entries from Requirement a Change in Plan Assets: (41) Beginning Balance of Plan Assets (42) Expected Return of Plan Assets (43)Unexpected Return of Plan Assets Amount (44) Employer Contributions (45) Benefits paid during the year (46) Ending Balance of Plan Assets Indicate the funded status of the plan. Amount The ending funded status of the plan is a $ (47) net liability or underfunded over funded (48) not cisset or The beginning funded status of the plan is a $ Requirement d. Prepare the journal entry to record the current year's pension cost. (Abbreviations used: OCI = Other Comprehensive Income. Record debits first, then credits. Exclude explanations from any journal entries.) Review the conceptual journal entries from Requirement a. Account (49) Pension Expense (50) (C1-Acturial Grains / Lasses (51) Cash (52) Net Pension Liability (53) 1: More Info a. Beginning plan assets at fair value (market-related value), $580,000 b. Beginning projected benefit obligation (PVDBO), $510,000 c. Service cost for the year, $122,000 d. Settlement rate, 8% e. Expected return on plan assets, 8% f. Actual return on plan assets, $24,500 loss Current Year g. Contributions for the year, $45,400 h. Benefit payments for the year, $94,100 i. Beginning Accumulated Other Comprehensive Income, $39,000 (due to unamortized net actuarial gains) j. Past service costs awarded during the year (not effective as of the beginning of the year) for vested employees, $20,000 k. Amortization of prior service costs, $9,000 1. Decrease in the ending projected benefit obligation due to changes in actuarial assumptions (i.e., actuarial gain), $10,000 m. Average remaining service life of the employee base, 10 years 2: Requirements a. Prepare the separate "conceptual" journal entries for the relevant information above. b. Compute the pension cost for the year. C. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. d. Prepare the journal entry to record the current year's pension cost. Glass Attack, Ltd. provided you with the following information regarding its defined-benefit pension plan. Glass Attack Ltd. follows IFRS and it expects a return on plan assets equal to its settlement rate. 1(Click the icon to view the information.) Read the requirements². Requirement a. Prepare the separate "conceptual" journal entries for the relevant information above. (Abbreviations used: OCI = Other Comprehensive Income; PVDBO = Present Value of the Defined-Benefit Obligation. Record debits first, then credits. Exclude explanations from any journal entries. If no entry is required select "No Entry Required" on the first line of the journal entry table and leave all remaining cells in the table blank.) Begin by preparing the required conceptual journal entry, if any, for service costs for the current year. Account Pension Expense PVDBO Account Pension Expense Current Year PVDBO 122,000 Prepare the required conceptual journal entry, if any, for the past service costs awarded during the current year. Exclude any amortization of prior service costs. Current Year 20,000 Prepare the required conceptual journal entry, if any, for amortization of prior service costs. Account Current Year No Entry Required 122,000 Current Year Prepare the required conceptual journal entry, if any, for interest on the present value of the defined-benefit obligation (PVDBO). Account (1) Pension Expense (2) PVDBO (3) (4) Prepare the required conceptual journal entry, if any, for the expected return on plan assets. 20,000 Account (5) Pension Plan Assets (6) Pension Expense (7) (8) Prepare the required conceptual journal entry, if any, for the unexpected return on plan assets. Account Current Year (9) OCI - Acturial Gains / Losses (10) Pension Plan Assets. (11) (12) Prepare the required conceptual journal entry, if any, to adjust the PVDBO for changes in actuarial assumptions. Account Current Year (13) PVDBO (14) OCI - Acturial Gains / Losses (15) (16) Current Year Prepare the required conceptual journal entry, if any, to amortize the net actuarial gains or losses under the corridor approach. Account Current Year (17) No entry Required (18) (19) (20) Prepare the required conceptual journal entry, if any, to record contributions made to the plan during the year. Current Year Account (21) Pension Plan Assets (22) Cash (23) (24) Prepare the required conceptual journal entry, if any, to record any benefit payments made to retirees during the year. Current Year Account (25) PVDBO (26) Pension Plan Assels. (27) (28) Requirement b. Compute the pension cost for the year. Select the labels and enter the amounts for all items that are included in the pension cost for the year. (Abbreviations used: PVDBO Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for items that reduce pension cost. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Components of Pension Cost: Amount (29) Service Cost (30) Interest on PYDEO (31) Expected Return on Plan Assels (32) Prior Service Cart (33) (34) Total Pension Cost Requirement c. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. Begin by selecting the labels and entering the amounts to determine the ending balance of the projected benefit obligation. (Abbreviations used: PVDBO = Present Value of the Defined-Benefit Obligation. Use parentheses or a minus sign for credit balances and for items that increase the benefit obligation. If a box is not used in the table leave the box empty; do not select a label or enter a zero.) Review the conceptual journal entries from Requirement a. Change in Benefit Obligation: (35) Beginning Balance of PVD BO (36) Service Cost (37) Past Service Cost (38) Interest on PUDEO (39) Change in Acturial Assumption (Gran)) (40) Benefits Paid during the year Ending Balance of PVDBO Select the labels and enter the amounts to determine the balance of the plan assets at the end of the year. (Use parentheses or a minus sign for items that reduce plan assets. If a box is not used in the table leave the box empty; do not selecta enter a zero.) label or Review the conceptual journal entries from Requirement a Change in Plan Assets: (41) Beginning Balance of Plan Assets (42) Expected Return of Plan Assets (43)Unexpected Return of Plan Assets Amount (44) Employer Contributions (45) Benefits paid during the year (46) Ending Balance of Plan Assets Indicate the funded status of the plan. Amount The ending funded status of the plan is a $ (47) net liability or underfunded over funded (48) not cisset or The beginning funded status of the plan is a $ Requirement d. Prepare the journal entry to record the current year's pension cost. (Abbreviations used: OCI = Other Comprehensive Income. Record debits first, then credits. Exclude explanations from any journal entries.) Review the conceptual journal entries from Requirement a. Account (49) Pension Expense (50) (C1-Acturial Grains / Lasses (51) Cash (52) Net Pension Liability (53) 1: More Info a. Beginning plan assets at fair value (market-related value), $580,000 b. Beginning projected benefit obligation (PVDBO), $510,000 c. Service cost for the year, $122,000 d. Settlement rate, 8% e. Expected return on plan assets, 8% f. Actual return on plan assets, $24,500 loss Current Year g. Contributions for the year, $45,400 h. Benefit payments for the year, $94,100 i. Beginning Accumulated Other Comprehensive Income, $39,000 (due to unamortized net actuarial gains) j. Past service costs awarded during the year (not effective as of the beginning of the year) for vested employees, $20,000 k. Amortization of prior service costs, $9,000 1. Decrease in the ending projected benefit obligation due to changes in actuarial assumptions (i.e., actuarial gain), $10,000 m. Average remaining service life of the employee base, 10 years 2: Requirements a. Prepare the separate "conceptual" journal entries for the relevant information above. b. Compute the pension cost for the year. C. Determine the ending balances of the plan assets and the projected benefit obligation and indicate the funded status of the plan. d. Prepare the journal entry to record the current year's pension cost.

Expert Answer:

Answer rating: 100% (QA)

Pension Work Sheet Negative sign indicates Credits Positive Sign Indicates Debits Items Balance Jan ... View the full answer

Related Book For

Accounting Tools for Business Decision Making

ISBN: 978-1118096895

6th edition

Authors: Paul D. Kimmel, Jerry J. Weygandt, Donald E. Kieso

Posted Date:

Students also viewed these accounting questions

-

Precision Castparts, a manufacturer of processed engine parts in the automotive and airline industries, borrows $39 million cash on October 1, 2015, to provide working capital for anticipated...

-

Copperhead Company has provided you with the following information regarding its inventory of copper for September and October. Copperhead uses a perpetual inventory system....

-

A manufacturing company has provided you with the following data, which relate to component RYX for the period which has just ended: Overheads are absorbed at a rate per standard labour hour. (a) (i)...

-

The Dell Corporation borrowed $10,000,000 at 7% interest per year, which must be repaid in equal EOY amounts (including both interest and principal) over the next six years. How much must Dell repay...

-

A group of researchers at a company that produces a leading brand of ice cream design an experiment to evaluate the impact of several artificial sweeteners on the texture of the product. It is well...

-

For next month, a hotel manager forecasts revenue of $800,000. 60% of the revenue to be generated in the month will be made to customers who will not pay their bills within the same month as they are...

-

The motion of a nightingales wingtips can be modeled as simple harmonic motion. In one study, the tips of a birds wings were found to move up and down with an amplitude of 8.8 cm and a period of 0.82...

-

A tabular analysis of the transactions made during August 2012 by Nigel Company during its first month of operations is shown below. Each increase and decrease in stockholders?? equity is explained....

-

IF THE UNIT OF THE HOSPITAL'S CENUS IS 40 PATIENTS AND FOR THE MONTH OF JANUARY THERE HAS BEEN 4 FALLS WHAT IS THE PERCENTAGE OF FALLS FOR THE MONTH OF JANUARY?

-

S. L. P. Craft would like your help in developing a layout for a new outpatient clinic to be built in California. From analysis of another recently built clinic, she obtains the data shown in the...

-

Amber has a tax basis of $67,000 in her partnership interest in Lightfoot Partnership, which consists of her $27,000 net contribution to partnership capital and her $40,000 share of partnership debt....

-

Determining and evaluating project cash flows for a home solar system You are keen on the use of solar power and have decided to evaluate investing in a solar system for your home. After consulting...

-

Doug Horn will buy more and more of a good or service until _____. a) marginal utility is greater than price b) price is greater than marginal utility c) price is equal to marginal utility

-

An economy has 100 people divided among the following groups: 25 have full-time jobs, 20 have one part-time job, 5 have two part-time jobs, 10 would like to work and are looking for jobs, 10 would...

-

As Keith Collins buys more and more of any good or service, his ____. a) total utility and marginal utility both decline b) total utility and marginal utility both rise c) total utility rises and...

-

In the long run a business has two options: to _______or ________ to .

-

The Figure below shows a conveyor belt system. The objective of the system is to move the work piece by a pre-set speed. a) There is a component missing in the figure below, identify this component...

-

The unadjusted trial balance of Secretarial Services is as follows: SECRETARIAL SERVICES Unadjusted Trial Balance as at 31 December 2017 Account Debit Credit Cash at bank Office supplies Prepaid...

-

The net income for Mongan Co. for 2017 was $280,000. For 2017, depreciation on plant assets was $70,000, and the company incurred a loss on disposal of plant assets of $28,000. Compute net cash...

-

The following financial information is for Priscoll Company Additional information 1. Inventory at the beginning of 2016 was $115,000. 2. Accounts receivable (net) at the beginning of 2016 were...

-

Maria Lopez, CEO of Sales Bin Stores is considering a recommendation made by both the company's purchasing manager and director of finance dial the company should invest in a sophisticated.

-

Raye believes the previous advisers specification for debt is incorrect given that, for purposes of asset allocation, asset classes should be: A. diversifying. B. mutually exclusive. C. relatively...

-

Raye believes the previous advisers asset class specifications for equity and derivatives are inappropriate given that, for purposes of asset allocation, asset classes should be: A. diversifying. B....

-

Rayes approach to rebalancing global equities is consistent with: A. the Laws being risk averse. B. global equities having higher transaction costs than other asset classes. C. global equities having...

Study smarter with the SolutionInn App