Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

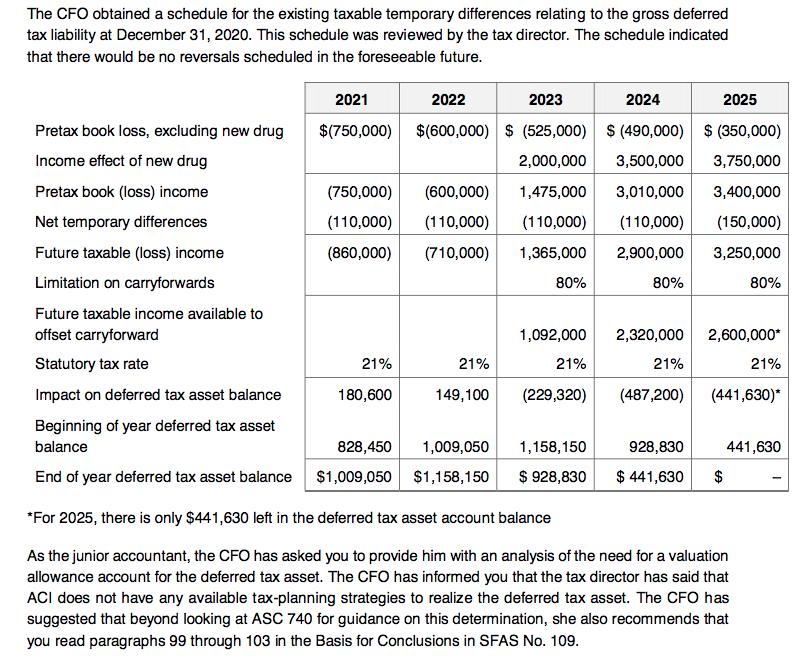

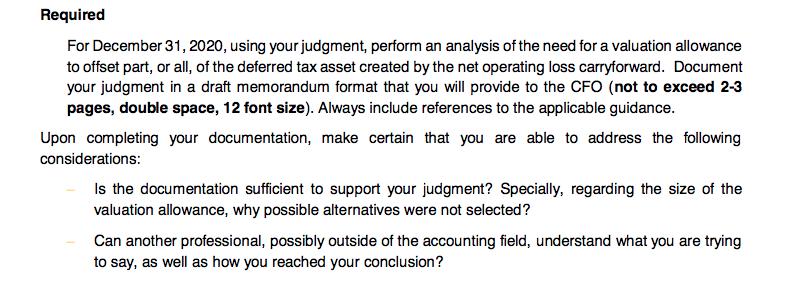

Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding the deferred tax asset, ACI total assets are $3.5 million. ACI was a profitable company. In 2018, ACI began reporting a net loss (both book and tax loss), which has been primarily attributable to significant research and development costs. Now it is 2020. The following table presents the loss figures for ACI. ACI's relevant statutory tax rate is 21% and the company did not have any permanent book-tax differences during 2018, 2019 or 2020. ACI did not establish a valuation allowance to offset the deferred tax asset in 2018 or 2019. Pretax book loss Net temporary differences Taxable loss Statutory tax rate Impact on the deferred tax asset balance Net loss (after tax)* Deferred tax asset balance Valuation allowance* 2018 $ (900,000) (210,000) (1,110,000) 21% 233,100 $(666,900) $233,100 2019 $(1,890,000) (60,000) (1,950,000) 21% 409,500 $(1,480,500) $642,600 2020 $(775,000) (110,000) (885,000) 21% 185,850 $(589,150) $828,450 ? ACI is assessing the need to record a valuation allowance to offset the deferred tax asset balance created by the net operating loss carryforward. While the company has reported losses in the past three years, management anticipates positive income in the future. The executives of ACI do not anticipate any fundamental shift in its business operations in the future. The company is currently in the final research and development stage of a new drug that has tremendous market opportunity. Management believes that this drug will be on the market within three years based on the company's past experience. The income projections for the next five years prepared by the CFO are presented below. The CFO determined that, while NOL can be carried forward indefinitely, predicting numbers beyond the 5- year period was impractical. However, the CFO does anticipate positive taxable income in 2026 and beyond, because the new drug can bring long-term profit and there lacks of any known competing drugs. The CFO has been with ACI for his entire career and has been extremely competent in terms of preparing income projections and meeting forecasts. The income effect of the new drug is based on information gathered when its most recent significant drug was released. There have been no actual or expected changes in tax laws indicating a potential change in the statutory tax rate. The projections provided have been shared with analysts and investors. The CFO obtained a schedule for the existing taxable temporary differences relating to the gross deferred tax liability at December 31, 2020. This schedule was reviewed by the tax director. The schedule indicated that there would be no reversals scheduled in the foreseeable future. Pretax book loss, excluding new drug Income effect of new drug Pretax book (loss) income Net temporary differences Future taxable (loss) income Limitation on carryforwards Future taxable income available to offset carryforward Statutory tax rate Impact on deferred tax asset balance 2021 2022 2023 $(750,000) $(600,000) $ (525,000) 2,000,000 1,475,000 (110,000) (110,000) 1,365,000 80% (750,000) (600,000) (110,000) (860,000) (710,000) 21% 180,600 21% 149,100 1,092,000 21% (229,320) 828,450 1,009,050 $1,009,050 $1,158,150 2024 $ (490,000) 3,500,000 3,010,000 (110,000) 2,900,000 80% 2,320,000 21% (487,200) 2025 $ (350,000) 3,750,000 3,400,000 (150,000) 3,250,000 80% 2,600,000* Beginning of year deferred tax asset balance End of year deferred tax asset balance *For 2025, there is only $441,630 left in the deferred tax asset account balance As the junior accountant, the CFO has asked you to provide him with an analysis of the need for a valuation allowance account for the deferred tax asset. The CFO has informed you that the tax director has said that ACI does not have any available tax-planning strategies to realize the deferred tax asset. The CFO has suggested that beyond looking at ASC 740 for guidance on this determination, she also recommends that you read paragraphs 99 through 103 in the Basis for Conclusions in SFAS No. 109. (441,630)* 21% 1,158,150 928,830 $ 928,830 $441,630 $ 441,630 Required For December 31, 2020, using your judgment, perform an analysis of the need for a valuation allowance to offset part, or all, of the deferred tax asset created by the net operating loss carryforward. Document your judgment in a draft memorandum format that you will provide to the CFO (not to exceed 2-3 pages, double space, 12 font size). Always include references to the applicable guidance. Upon completing your documentation, make certain that you are able to address the following considerations: Is the documentation sufficient to support your judgment? Specially, regarding the size of the valuation allowance, why possible alternatives were not selected? Can another professional, possibly outside of the accounting field, understand what you are trying to say, as well as how you reached your conclusion? Advanced Chemical Industries (ACI) is a leading pharmaceutical company. ACI only operates in the US. Excluding the deferred tax asset, ACI total assets are $3.5 million. ACI was a profitable company. In 2018, ACI began reporting a net loss (both book and tax loss), which has been primarily attributable to significant research and development costs. Now it is 2020. The following table presents the loss figures for ACI. ACI's relevant statutory tax rate is 21% and the company did not have any permanent book-tax differences during 2018, 2019 or 2020. ACI did not establish a valuation allowance to offset the deferred tax asset in 2018 or 2019. Pretax book loss Net temporary differences Taxable loss Statutory tax rate Impact on the deferred tax asset balance Net loss (after tax)* Deferred tax asset balance Valuation allowance* 2018 $ (900,000) (210,000) (1,110,000) 21% 233,100 $(666,900) $233,100 2019 $(1,890,000) (60,000) (1,950,000) 21% 409,500 $(1,480,500) $642,600 2020 $(775,000) (110,000) (885,000) 21% 185,850 $(589,150) $828,450 ? ACI is assessing the need to record a valuation allowance to offset the deferred tax asset balance created by the net operating loss carryforward. While the company has reported losses in the past three years, management anticipates positive income in the future. The executives of ACI do not anticipate any fundamental shift in its business operations in the future. The company is currently in the final research and development stage of a new drug that has tremendous market opportunity. Management believes that this drug will be on the market within three years based on the company's past experience. The income projections for the next five years prepared by the CFO are presented below. The CFO determined that, while NOL can be carried forward indefinitely, predicting numbers beyond the 5- year period was impractical. However, the CFO does anticipate positive taxable income in 2026 and beyond, because the new drug can bring long-term profit and there lacks of any known competing drugs. The CFO has been with ACI for his entire career and has been extremely competent in terms of preparing income projections and meeting forecasts. The income effect of the new drug is based on information gathered when its most recent significant drug was released. There have been no actual or expected changes in tax laws indicating a potential change in the statutory tax rate. The projections provided have been shared with analysts and investors. The CFO obtained a schedule for the existing taxable temporary differences relating to the gross deferred tax liability at December 31, 2020. This schedule was reviewed by the tax director. The schedule indicated that there would be no reversals scheduled in the foreseeable future. Pretax book loss, excluding new drug Income effect of new drug Pretax book (loss) income Net temporary differences Future taxable (loss) income Limitation on carryforwards Future taxable income available to offset carryforward Statutory tax rate Impact on deferred tax asset balance 2021 2022 2023 $(750,000) $(600,000) $ (525,000) 2,000,000 1,475,000 (110,000) (110,000) 1,365,000 80% (750,000) (600,000) (110,000) (860,000) (710,000) 21% 180,600 21% 149,100 1,092,000 21% (229,320) 828,450 1,009,050 $1,009,050 $1,158,150 2024 $ (490,000) 3,500,000 3,010,000 (110,000) 2,900,000 80% 2,320,000 21% (487,200) 2025 $ (350,000) 3,750,000 3,400,000 (150,000) 3,250,000 80% 2,600,000* Beginning of year deferred tax asset balance End of year deferred tax asset balance *For 2025, there is only $441,630 left in the deferred tax asset account balance As the junior accountant, the CFO has asked you to provide him with an analysis of the need for a valuation allowance account for the deferred tax asset. The CFO has informed you that the tax director has said that ACI does not have any available tax-planning strategies to realize the deferred tax asset. The CFO has suggested that beyond looking at ASC 740 for guidance on this determination, she also recommends that you read paragraphs 99 through 103 in the Basis for Conclusions in SFAS No. 109. (441,630)* 21% 1,158,150 928,830 $ 928,830 $441,630 $ 441,630 Required For December 31, 2020, using your judgment, perform an analysis of the need for a valuation allowance to offset part, or all, of the deferred tax asset created by the net operating loss carryforward. Document your judgment in a draft memorandum format that you will provide to the CFO (not to exceed 2-3 pages, double space, 12 font size). Always include references to the applicable guidance. Upon completing your documentation, make certain that you are able to address the following considerations: Is the documentation sufficient to support your judgment? Specially, regarding the size of the valuation allowance, why possible alternatives were not selected? Can another professional, possibly outside of the accounting field, understand what you are trying to say, as well as how you reached your conclusion?

Expert Answer:

Answer rating: 100% (QA)

Based on my analysis I recommend that the CFO should not establish a valuation allowance to offset the deferred tax asset balance because ACI is antic... View the full answer

Related Book For

Financial Reporting Financial Statement Analysis and Valuation a strategic perspective

ISBN: 978-1337614689

9th edition

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

Posted Date:

Students also viewed these accounting questions

-

Asbat Pharmaceuticals (Asbat) is a leading pharmaceutical company that has been in existence for 22 years. Asbat has a calendar year-end and is audited annually. Asbat only operates in the United...

-

The Company classifies its investments in both fixed income securities and publicly traded equity securities as available- for- sale investments. Fixed income securities primarily consist of U. S....

-

Lehman Brothers Holdings Inc. was originally founded in Montgomery, Alabama, in 1850 by three brothers. The company began as a small retailer that took cotton as payment for goods. The company...

-

Find the antiderivative for each function when C equals 0. a. f(x) = 1 7 b. g(x)== 11 +/- 150 is a. The antiderivative of 5 c. h(x)=4 -- X Part 1 of 3

-

Dead Eye Putters manufactures golf putters in three models: P450, Q550, and R650. Manufacturing overhead is assigned to each putter model using a predetermined overhead rate and the direct labor...

-

According to (4.8.15) in Section 4.8, the scattering rate for fermions is proportional to 1/2 (U D U E ) 2 , where UD is the direct interaction vertex and U E is the exchange vertex. In the diagram...

-

Pew Research Center collected data on the same 10 political value questions from 1994 to 2014 and combines these responses to place each person on a scale ranging from consistently liberal to...

-

BONDS ISSUED AT FACE VALUE WITH SINKING FUND Creswell Entertainment issued the following bonds: Date of issue and sale: ........April 1, 20-1 Principal amount: ..........$600,000 Sale price of bonds:...

-

What I learnt? Customer Behaviour: 1) Customer satisfaction only results in loyalty at the highest level of satisfaction - do not focus entirely on satisfaction 2) Improvements that are not...

-

Icementrics is a subcontract manufacturer that produces prototype products for organizations that may possibly want Icementrics to later manufacture their products for them.Icementrics has a R & D...

-

Compare and contrast Eriksons psychosocial model of development with Freuds psychosexual model.

-

Executive methods, market research, and the Delphi method are examples of Quantitative method of forecasting Qualitative method of forecasting Benchmarking None of the above

-

The Zenibeth Factory, which manufactured Quasar television sets, was taken over by a Japanese company in the USA in the 1980s. After overtaking the company, it was decided to make changes in the way...

-

Planning does not render flexibility. True False

-

Which of these is being devised by the managers? Long-term plans Short-term plans Medium-term plans None of the above

-

Planning is accompanied by ________ schedules. Flexible time Fixed time Both None of the above

-

Use the following table: Large stocks Small stocks Long-term corporate bonds Long-term government bonds U.S. Treasury bills Inflation Average return 11.94% 16.64 6.32 6.10 3.92 3.10 a. Determine the...

-

Find the radius of convergence in two ways: (a) Directly by the CauchyHadamard formula in Sec. 15.2. (b) From a series of simpler terms by using Theorem 3 or Theorem 4.

-

Canadian National Railway Company (CN) spans Canada and mid-America and provides freight transport services from the Atlantic Ocean to the Pacific Ocean and to the Gulf of Mexico. It is currently the...

-

Using the following key, identify the effects of the following transactions or conditions on the various financial statement elements: I = increases; D = decreases; NE = no effect. Note that the...

-

Massachusetts Stove Company manufactures wood-burning stoves for the heating of homes and businesses. The company has approached you, as chief lending officer for the Massachusetts Regional Bank,...

-

First-Year College GPA Researchers at the College Board wanted to build a model that describes one's first-year college GPA. The researchers obtained the following model: \[\hat{y}=0.06 x_{1}+0.07...

-

Find the upper and lower critical values at the \(\alpha=0.05\) level of significance from Table XI if \(n_{1}=10\) and \(n_{2}=5\). Approach Determine the intersection of the row corresponding to...

-

The data in Table 2 represent the monthly rates of return of the Standard and Poor's Index of 500 Stocks from January 2012 through March 2015. Test the randomness of positive monthly rates of return...

Study smarter with the SolutionInn App