After preparing a draft statement of profit or loss for the year ended 30 September 20X5...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

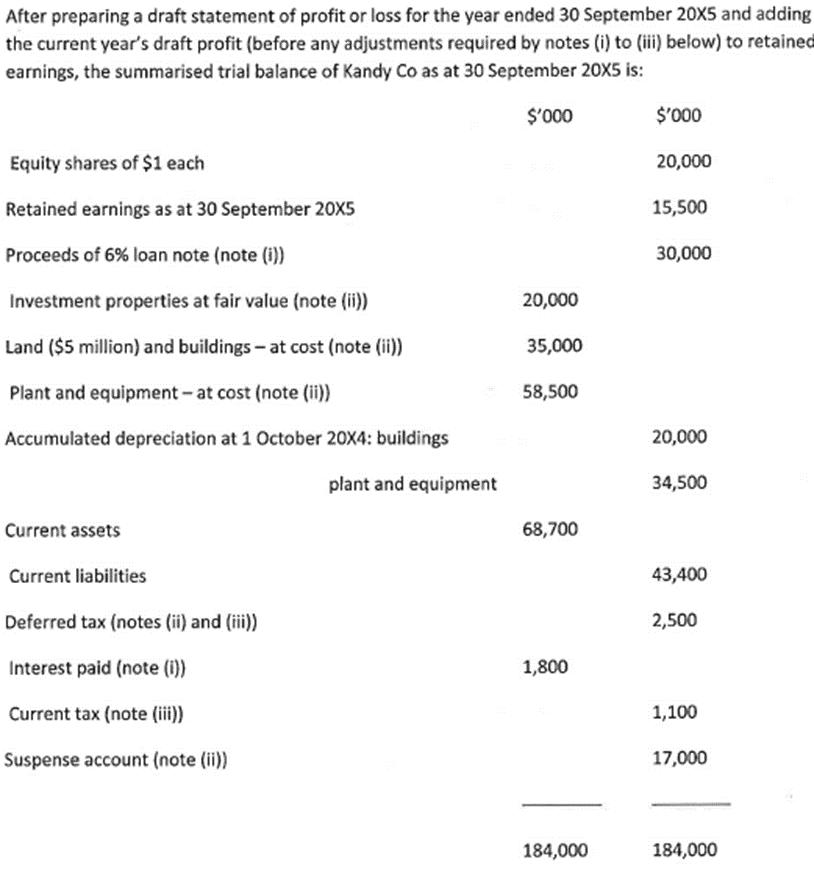

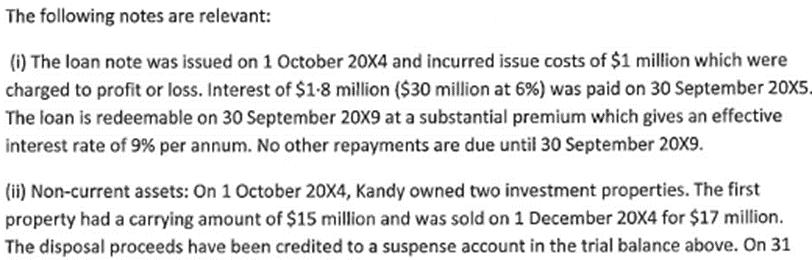

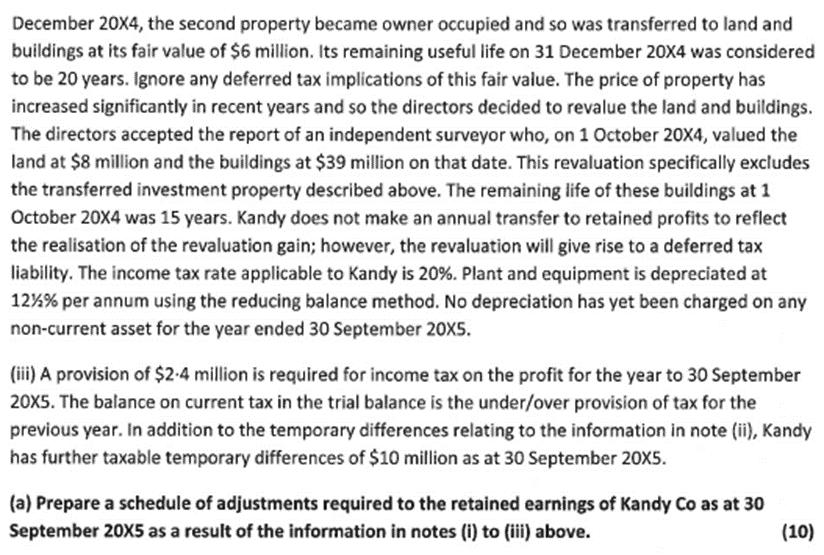

After preparing a draft statement of profit or loss for the year ended 30 September 20X5 and adding the current year's draft profit (before any adjustments required by notes (i) to (iii) below) to retained earnings, the summarised trial balance of Kandy Co as at 30 September 20X5 is: $'000 $'000 Equity shares of $1 each 20,000 Retained earnings as at 30 September 20X5 15,500 Proceeds of 6% loan note (note (i)) 30,000 Investment properties at fair value (note (ii)) 20,000 Land ($5 million) and buildings - at cost (note (ii)) 35,000 Plant and equipment - at cost (note (ii)) 58,500 Accumulated depreciation at 1 October 20X4: buildings 20,000 plant and equipment 34,500 Current assets 68,700 Current liabilities 43,400 Deferred tax (notes (ii) and (iii)) 2,500 Interest paid (note (i)) 1,800 Current tax (note (iii)) 1,100 Suspense account (note (ii)) 17,000 184,000 184,000 The following notes are relevant: (i) The loan note was issued on 1 October 20X4 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1.8 million ($30 million at 6%) was paid on 30 September 20X5 The loan is redeemable on 30 September 20X9 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 20X9. (ii) Non-current assets: On 1 October 20X4, Kandy owned two investment properties. The first property had a carrying amount of $15 million and was sold on 1 December 20X4 for $17 million. The disposal proceeds have been credited to a suspense account in the trial balance above. On 31 December 20X4, the second property became owner occupied and so was transferred to land and buildings at its fair value of $6 million. Its remaining useful life on 31 December 20X4 was considered to be 20 years. Ignore any deferred tax implications of this fair value. The price of property has increased significantly in recent years and so the directors decided to revalue the land and buildings. The directors accepted the report of an independent surveyor who, on 1 October 20X4, valued the land at $8 million and the buildings at $39 million on that date. This revaluation specifically excludes the transferred investment property described above. The remaining life of these buildings at 1 October 20X4 was 15 years. Kandy does not make an annual transfer to retained profits to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability. The income tax rate applicable to Kandy is 20%. Plant and equipment is depreciated at 12% % per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 September 20X5. (iii) A provision of $2.4 million is required for income tax on the profit for the year to 30 September 20X5. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (ii), Kandy has further taxable temporary differences of $10 million as at 30 September 20X5. (a) Prepare a schedule of adjustments required to the retained earnings of Kandy Co as at 30 September 20X5 as a result of the information in notes (i) to (iii) above. (10) After preparing a draft statement of profit or loss for the year ended 30 September 20X5 and adding the current year's draft profit (before any adjustments required by notes (i) to (iii) below) to retained earnings, the summarised trial balance of Kandy Co as at 30 September 20X5 is: $'000 $'000 Equity shares of $1 each 20,000 Retained earnings as at 30 September 20X5 15,500 Proceeds of 6% loan note (note (i)) 30,000 Investment properties at fair value (note (ii)) 20,000 Land ($5 million) and buildings - at cost (note (ii)) 35,000 Plant and equipment - at cost (note (ii)) 58,500 Accumulated depreciation at 1 October 20X4: buildings 20,000 plant and equipment 34,500 Current assets 68,700 Current liabilities 43,400 Deferred tax (notes (ii) and (iii)) 2,500 Interest paid (note (i)) 1,800 Current tax (note (iii)) 1,100 Suspense account (note (ii)) 17,000 184,000 184,000 The following notes are relevant: (i) The loan note was issued on 1 October 20X4 and incurred issue costs of $1 million which were charged to profit or loss. Interest of $1.8 million ($30 million at 6%) was paid on 30 September 20X5 The loan is redeemable on 30 September 20X9 at a substantial premium which gives an effective interest rate of 9% per annum. No other repayments are due until 30 September 20X9. (ii) Non-current assets: On 1 October 20X4, Kandy owned two investment properties. The first property had a carrying amount of $15 million and was sold on 1 December 20X4 for $17 million. The disposal proceeds have been credited to a suspense account in the trial balance above. On 31 December 20X4, the second property became owner occupied and so was transferred to land and buildings at its fair value of $6 million. Its remaining useful life on 31 December 20X4 was considered to be 20 years. Ignore any deferred tax implications of this fair value. The price of property has increased significantly in recent years and so the directors decided to revalue the land and buildings. The directors accepted the report of an independent surveyor who, on 1 October 20X4, valued the land at $8 million and the buildings at $39 million on that date. This revaluation specifically excludes the transferred investment property described above. The remaining life of these buildings at 1 October 20X4 was 15 years. Kandy does not make an annual transfer to retained profits to reflect the realisation of the revaluation gain; however, the revaluation will give rise to a deferred tax liability. The income tax rate applicable to Kandy is 20%. Plant and equipment is depreciated at 12% % per annum using the reducing balance method. No depreciation has yet been charged on any non-current asset for the year ended 30 September 20X5. (iii) A provision of $2.4 million is required for income tax on the profit for the year to 30 September 20X5. The balance on current tax in the trial balance is the under/over provision of tax for the previous year. In addition to the temporary differences relating to the information in note (ii), Kandy has further taxable temporary differences of $10 million as at 30 September 20X5. (a) Prepare a schedule of adjustments required to the retained earnings of Kandy Co as at 30 September 20X5 as a result of the information in notes (i) to (iii) above. (10)

Expert Answer:

Related Book For

International Financial Reporting A Practical Guide

ISBN: 978-1292200743

6th edition

Authors: Alan Melville

Posted Date:

Students also viewed these accounting questions

-

On 1 June 20X2, Premier acquired 80 per cent of the equity share capital of Sanford. The consideration consisted of two elements: a share exchange of three shares in Premier for every five acquired...

-

Explain 3-Cyanopropyldimethylchlorosilane?

-

Which of the following is most nearly the mass of the Earth? (The radius of the Earth is about 6.4 106 m) A. 6 x 1024 kg B. 6 x 107 kg C. 6 x 103 kg D. 6 x 1033 kg E. 6 x 1036 kg

-

Use the financial statements of CoCo Roofers Inc., plus the following item (in millions): Number of common shares outstanding ..................... 0.8 1. Compute earnings per share (EPS) for CoCo...

-

A rule of thumb used to determine the internal resistance of a source is that it is the open-circuit voltage divided by the short-circuit current. Is this correct? Why or why not?

-

Why should you conduct technical reviews?

-

Record in T accounts the following stock transactions of Pigua Corporation, which represent all the companys treasury stock transactions during 2011: May 5Purchased 1,600 shares of its own $2 par...

-

Tempo Company's fixed budget (based on sales of 18,000 units) folllows. Fixed Budget Sales (18,000 units x $204 per unit) Costs Direct materials Direct labor Indirect materials Supervisor salary...

-

A commercial real estate investment fund must report its quarterly investment performance to investors. A summary of its (1) beginning and end-of-quarter assets and equity and (2) cash inflows and...

-

Westcomes investment approach for Maglavs pension plan can be best characterized as the: A. Norway model. B. Canadian model. C. endowment model. William Azarov is a portfolio manager for Westcome...

-

Identify the new investment approach proposed by Zang for managing the Fund. Justify your response. Bern Zang is the recently hired chief investment officer of the Janson University Endowment...

-

Identify the investment approach currently being used by the Investment Committee for managing the Fund. Justify your response. Bern Zang is the recently hired chief investment officer of the Janson...

-

Fiona Heselwith is a 40-year-old US citizen who has accepted a job with Lyricul, LLC, a UK-based company. Her benefits package includes a retirement savings plan. The company offers both a defined...

-

Dianna Mark is the chief financial officer of Antiliaro, a relatively mature textile production company headquartered in Italy. All of its revenues come from Europe, but the company is losing sales...

-

Question 5 Standard Costs and Variance Analysis STEFANO Company makes laptops, for which the following standards have been developed: Direct Costs Standard Inputs Expected for Each Unit of Output...

-

Suppose the government bond described in problem 1 above is held for five years and then the savings institution acquiring the bond decides to sell it at a price of $940. Can you figure out the...

-

Outline the structure and functions of: (a) The IFRS Foundation. (b) The International Accounting Standards Board (IASB). (c) The IFRS Advisory Council. (d) The IFRS Interpretations Committee.

-

A customer buys three DVDs from a mail order company. These DVDs could have been bought separately and are regarded as distinct. The prices normally charged for the DVDs (if bought separately) are...

-

On 1 December 2014, Gebouw plc entered into a finance lease requiring the company to make payments of 785,000 each on 1 December 2014, 2015, 2016, 2017 and 2018. The fair value of the leased asset on...

-

The rotor shown in Fig. 9.44 (a) is balanced temporarily in a balancing machine by adding the masses \(m_{1}=m_{2}=90 \mathrm{~g}\) in the plane \(A\) and \(m_{3}=m_{4}=90 \mathrm{~g}\) in the plane...

-

A turbine rotor is run at the natural frequency of the system. A stroboscope indicates that the maximum displacement of the rotor occurs at an angle \(229^{\circ}\) in the direction of rotation. At...

-

The cylinders of a four-cylinder in-line engine are placed at intervals of \(300 \mathrm{~mm}\) in the axial direction. The cranks have the same length, \(100 \mathrm{~mm}\), and their angular...

Study smarter with the SolutionInn App