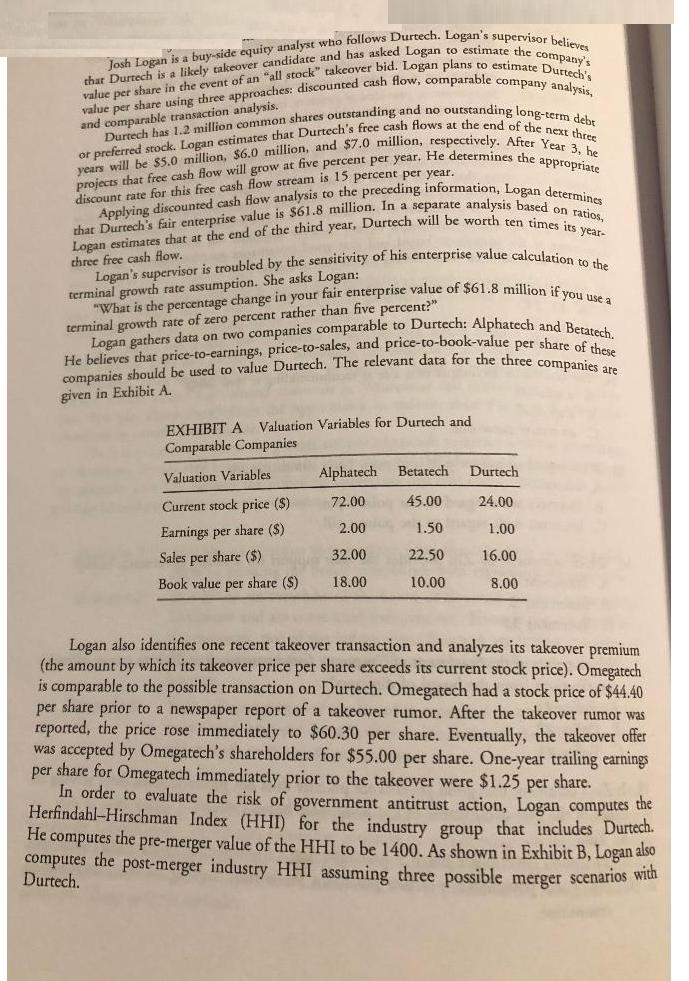

and comparable transaction analysis. that Durtech is a likely takeover candidate and has asked Logan to...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

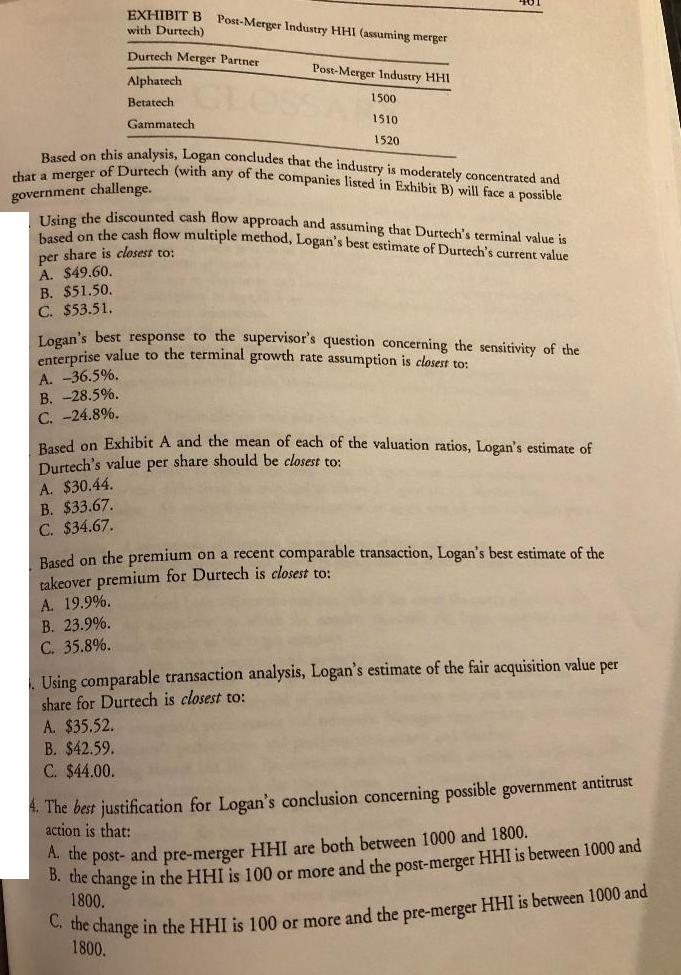

and comparable transaction analysis. that Durtech is a likely takeover candidate and has asked Logan to estimate the company's Josh Logan is a buy-side equity analyst who follows Durtech. Logan's supervisor believes value per share using three approaches: discounted cash flow, comparable company analysis, value per share in the event of an "all stock" takeover bid. Logan plans to estimate Durtech's Durtech has 1.2 million common shares outstanding and no outstanding long-term debr or preferred stock. Logan estimates that Durtech's free cash flows at the end of the next three years will be $5.0 million, $6.0 million, and $7.0 million, respectively. After Year 3, he projects that free cash flow will grow at five percent per year. He determines the appropriate that Durtech's fair enterprise value is $61.8 million. In a separate analysis based on ratios, Applying discounted cash flow analysis to the preceding information, Logan determines Logan estimates that at the end of the third year, Durtech will be worth ten times its year- discount rate for this free cash flow stream is 15 percent per year. three free cash flow. D Logan's supervisor is troubled by the sensitivity of his enterprise value calculation to the "What is the percentage change in your fair enterprise value of $61.8 million if you use a terminal growth rate assumption. She asks Logan: terminal growth rate of zero percent rather than five percent?" He believes that price-to-earnings, price-to-sales, and price-to-book-value per share of these Logan gathers data on two companies comparable to Durtech: Alphatech and Betatech. companies should be used to value Durtech. The relevant data for the three companies are given in Exhibit A. EXHIBIT A Valuation Variables for Durtech and Comparable Companies Valuation Variables Current stock price ($) Earnings per share ($) Sales per share ($) Book value per share ($) Alphatech Betatech Durtech 72.00 45.00 24.00 2.00 1.50 1.00 32.00 22.50 16.00 18.00 10.00 8.00 Logan also identifies one recent takeover transaction and analyzes its takeover premium (the amount by which its takeover price per share exceeds its current stock price). Omegatech is comparable to the possible transaction on Durtech. Omegatech had a stock price of $44.40 per share prior to a newspaper report of a takeover rumor. After the takeover rumor was reported, the price rose immediately to $60.30 per share. Eventually, the takeover offer was accepted by Omegatech's shareholders for $55.00 per share. One-year trailing earnings per share for Omegatech immediately prior to the takeover were $1.25 per share. In order to evaluate the risk of government antitrust action, Logan computes the Herfindahl-Hirschman Index (HHI) for the industry group that includes Durtech. He computes the pre-merger value of the HHI to be 1400. As shown in Exhibit B, Logan also computes the post-merger industry HHI assuming three possible merger scenarios with Durtech. EXHIBIT B Post-Merger Industry HHI (assuming merger with Durtech) Durtech Merger Partner Alphatech Betatech Gammatech A. $30.44. B. $33.67. C. $34.67. Post-Merger Industry HHI 1500 1510 Based on this analysis, Logan concludes that the industry is moderately concentrated and that a merger of Durtech (with any of the companies listed in Exhibit B) will face a possible government challenge. Using the discounted cash flow approach and assuming that Durtech's terminal value is based on the cash flow multiple method, Logan's best estimate of Durtech's current value per share is closest to: A. $49.60. B. $51.50. C. $53.51. 1520 Logan's best response to the supervisor's question concerning the sensitivity of the enterprise value to the terminal growth rate assumption is closest to: A. -36.5%. B.-28.5%. C.-24.8%. A. 19.9%. B. 23.9%. C. 35.8%. Based on Exhibit A and the mean of each of the valuation ratios, Logan's estimate of Durtech's value per share should be closest to: Based on the premium on a recent comparable transaction, Logan's best estimate of the takeover premium for Durtech is closest to: Using comparable transaction analysis, Logan's estimate of the fair acquisition value per share for Durtech is closest to: A. $35.52. B. $42.59. C. $44.00. 4. The best justification for Logan's conclusion concerning possible government antitrust action is that: A. the post- and pre-merger HHI are both between 1000 and 1800. the change in the HHI is 100 1800. C. the change in the HHI is 100 or more and the pre-merger HHI is between 1000 and 1800. more and the post-merger HHI is between 1000 and and comparable transaction analysis. that Durtech is a likely takeover candidate and has asked Logan to estimate the company's Josh Logan is a buy-side equity analyst who follows Durtech. Logan's supervisor believes value per share using three approaches: discounted cash flow, comparable company analysis, value per share in the event of an "all stock" takeover bid. Logan plans to estimate Durtech's Durtech has 1.2 million common shares outstanding and no outstanding long-term debr or preferred stock. Logan estimates that Durtech's free cash flows at the end of the next three years will be $5.0 million, $6.0 million, and $7.0 million, respectively. After Year 3, he projects that free cash flow will grow at five percent per year. He determines the appropriate that Durtech's fair enterprise value is $61.8 million. In a separate analysis based on ratios, Applying discounted cash flow analysis to the preceding information, Logan determines Logan estimates that at the end of the third year, Durtech will be worth ten times its year- discount rate for this free cash flow stream is 15 percent per year. three free cash flow. D Logan's supervisor is troubled by the sensitivity of his enterprise value calculation to the "What is the percentage change in your fair enterprise value of $61.8 million if you use a terminal growth rate assumption. She asks Logan: terminal growth rate of zero percent rather than five percent?" He believes that price-to-earnings, price-to-sales, and price-to-book-value per share of these Logan gathers data on two companies comparable to Durtech: Alphatech and Betatech. companies should be used to value Durtech. The relevant data for the three companies are given in Exhibit A. EXHIBIT A Valuation Variables for Durtech and Comparable Companies Valuation Variables Current stock price ($) Earnings per share ($) Sales per share ($) Book value per share ($) Alphatech Betatech Durtech 72.00 45.00 24.00 2.00 1.50 1.00 32.00 22.50 16.00 18.00 10.00 8.00 Logan also identifies one recent takeover transaction and analyzes its takeover premium (the amount by which its takeover price per share exceeds its current stock price). Omegatech is comparable to the possible transaction on Durtech. Omegatech had a stock price of $44.40 per share prior to a newspaper report of a takeover rumor. After the takeover rumor was reported, the price rose immediately to $60.30 per share. Eventually, the takeover offer was accepted by Omegatech's shareholders for $55.00 per share. One-year trailing earnings per share for Omegatech immediately prior to the takeover were $1.25 per share. In order to evaluate the risk of government antitrust action, Logan computes the Herfindahl-Hirschman Index (HHI) for the industry group that includes Durtech. He computes the pre-merger value of the HHI to be 1400. As shown in Exhibit B, Logan also computes the post-merger industry HHI assuming three possible merger scenarios with Durtech. EXHIBIT B Post-Merger Industry HHI (assuming merger with Durtech) Durtech Merger Partner Alphatech Betatech Gammatech A. $30.44. B. $33.67. C. $34.67. Post-Merger Industry HHI 1500 1510 Based on this analysis, Logan concludes that the industry is moderately concentrated and that a merger of Durtech (with any of the companies listed in Exhibit B) will face a possible government challenge. Using the discounted cash flow approach and assuming that Durtech's terminal value is based on the cash flow multiple method, Logan's best estimate of Durtech's current value per share is closest to: A. $49.60. B. $51.50. C. $53.51. 1520 Logan's best response to the supervisor's question concerning the sensitivity of the enterprise value to the terminal growth rate assumption is closest to: A. -36.5%. B.-28.5%. C.-24.8%. A. 19.9%. B. 23.9%. C. 35.8%. Based on Exhibit A and the mean of each of the valuation ratios, Logan's estimate of Durtech's value per share should be closest to: Based on the premium on a recent comparable transaction, Logan's best estimate of the takeover premium for Durtech is closest to: Using comparable transaction analysis, Logan's estimate of the fair acquisition value per share for Durtech is closest to: A. $35.52. B. $42.59. C. $44.00. 4. The best justification for Logan's conclusion concerning possible government antitrust action is that: A. the post- and pre-merger HHI are both between 1000 and 1800. the change in the HHI is 100 1800. C. the change in the HHI is 100 or more and the pre-merger HHI is between 1000 and 1800. more and the post-merger HHI is between 1000 and

Expert Answer:

Related Book For

Corporate Finance A Focused Approach

ISBN: 978-1439078082

4th Edition

Authors: Michael C. Ehrhardt, Eugene F. Brigham

Posted Date:

Students also viewed these accounting questions

-

Audrey Inc. has 1 million common shares outstanding as at January 1, 2011. On June 30, 2011, 4% convertible bonds were converted into 100,000 additional shares. Up to that point, the bonds had paid...

-

Audrey Inc. has 1 million common shares outstanding as at January 1, 2014. On June 30, 2014, 4% convertible bonds were converted into 100,000 additional shares. Up to that point, the bonds had paid...

-

Audrey Inc. has 1 million common shares outstanding as at January 1, 2017. On June 30, 2017, 4% convertible bonds were converted into 100,000 additional shares. Up to that point, the bonds had paid...

-

DS Unlimited has the following transactions during August. August 6 Purchases 88 handheld game devices on account from GameGirl, Inc., for $290 each, terms 1/10, n/60. August 7 Pays $490 to Sure...

-

Find the amount of interest earned by each of the following deposits: $27,630.35 at 4.4% compounded quarterly for 3.7 years.

-

Suppose a market research firm enlisted 800 families in one U.S. city to participate in a study of expenditures for the December holiday season. Each family kept a log of spending for this holiday...

-

Which motion of follower is best for high speed cams? (a) SHM follower motion (b) Uniform acceleration and retardation of follower motion (c) Cycloidal motion follower (d) All of the above

-

RST business entity reported the following items during the current year: Dividends from 25%-owned domestic corporation $ 19,000 Municipal bond interest received 18,000 Corporate bond interest...

-

The clinic s COO asks you to create a budgeted income statement ( also called a profit and loss statement ) for the clinic for the upcoming fiscal year. She has asked an intern to create a volume...

-

Zia Co. makes flowerpots from recycled plastic in two departments, Molding and Packaging. Zia uses the weighted average method, and units completed in the Molding department are transferred to the...

-

What are the challenges associated with emerging markets? Give an example, and how Procter & Gamble, Siemens, Nestle, and Unilever overcome those challenges. One of the most basic issues at the...

-

Does section 402A of the Restatement apply to sales and services?

-

True Or False Plaintiffs in negligence actions cannot recover if they are only users of a product but did not purchase it.

-

True Or False If a defendant promises to buy the plaintiffs house for $100,000 but actually has no intention of doing so, and the plaintiff sues for breach of contract, the defendant will probably...

-

Under a comparative-negligence defense, a plaintiff who was awarded $1,000,000 and who was found to be 30 percent negligent would receive an award of ____________.

-

What is a 1983 action? Who can bring one?

-

Gironde Water Systems (GWS) is planning to build a water treatment plant in Cornucopia, a developing country with foreign currency sovereign debt ratings of Ba2/BB-/BB. GWS has signed a 15-year water...

-

How do network effects help Facebook fend off smaller social-networking rivals? Could an online retailer doing half as much business compete on an equal footing with Amazon in terms of costs? Explain.

-

What is the cost of equity based on the over-own-bond- yield-plus-judgmental-risk-premium method?

-

What is the impact of multinational operations on each of the following financial management topics? Cash management.

-

Suppose you suddenly remembered that the coefficient of variation (CV) is generally regarded as being a better measure of stand-alone risk than the standard deviation when the alternatives being...

-

Why is it important to test a theory? Why not simply accept a theory if it sounds right?

-

What is the intuition behind the geometric growth in interest?

-

You have $100,000 to donate to your college. You want to endow a perpetual scholarship that makes its first payment in 1 year. If the colleges discount rate is 4%, how large will the annual...

Study smarter with the SolutionInn App