Tracy-Ann ceased self-employment on 30 June 2021. She was then employed by Kitten ple for the...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

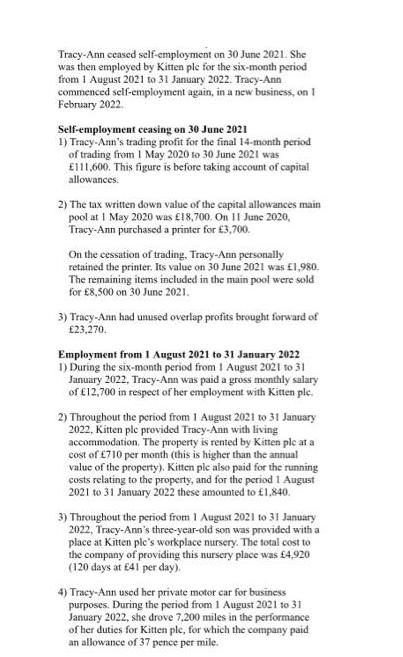

Tracy-Ann ceased self-employment on 30 June 2021. She was then employed by Kitten ple for the six-month period from 1 August 2021 to 31 January 2022. Tracy-Ann commenced self-employment again, in a new business, on 1 February 2022. Self-employment ceasing on 30 June 2021 1) Tracy-Ann's trading profit for the final 14-month period of trading from 1 May 2020 to 30 June 2021 was E111,600. This figure is before taking account of capital allowances. 2) The tax written down value of the capital allowances main pool at 1 May 2020 was £18,700. On 11 June 2020, Tracy-Ann purchased a printer for £3,700. On the cessation of trading, Tracy-Ann personally retained the printer. Its value on 30 June 2021 was £1,980. The remaining items included in the main pool were sold for £8,500 on 30 June 2021. 3) Tracy-Ann had unused overlap profits brought forward of £23,270 Employment from 1 August 2021 to 31 January 2022 1) During the six-month period from 1 August 2021 to 31 January 2022, Tracy-Ann was paid a gross monthly salary of £12,700 in respect of her employment with Kitten ple. 2) Throughout the period from 1 August 2021 to 31 January 2022, Kitten ple provided Tracy-Ann with living accommodation. The property is rented by Kitten ple at a cost of £710 per month (this is higher than the annual value of the property). Kitten ple also paid for the running costs relating to the property, and for the period 1 August 2021 to 31 January 2022 these amounted to £1,840. 3) Throughout the period from 1 August 2021 to 31 January 2022, Tracy-Ann's three-year-old son was provided with a place at Kitten ple's workplace nursery. The total cost to the company of providing this nursery place was £4,920 (120 days at £41 per day). 4) Tracy-Ann used her private motor car for business purposes. During the period from 1 August 2021 to 31 January 2022, she drove 7,200 miles in the performance of her duties for Kitten ple, for which the company paid an allowance of 37 pence per mile. Self-employment from 1 February 2022 1) Tracy-Ann's trading profit for the first five-month period of trading from 1 February to 30 June 2022 was £57,200. This figure is before taking account of capital allowances. 2) The only item of plant and machinery owned by Tracy- Ann, and used in this business, is office equipment which was purchased for £28,300 on 1 February 2022. Property income 1) During the period 1 August 2021 to 31 January 2022, Tracy-Ann let out her main residence at a monthly rent of £1,600. Tracy-Ann lived in this property up to 31 July 2021 and then again from 1 February 2022 onwards. 2) The only expenditure incurred by Tracy-Ann in respect of the letting was property insurance, which cost £750 for the year ended 5 April 2022. 3) Tracy-Ann has opted to calculate her property income using the accruals basis. Rent-a-room relief is not available in respect of the letting. Self-assessment tax return Tracy-Ann filed her self-assessment tax return for the tax year 2021-22 on 14 August 2022. She is quite confident that all of her income for the tax year 2021-22 was correctly declared and that no deductions were incorrectly claimed Required: (a) Calculate Tracy-Ann's taxable income for the tax year 2021-22. Note: You should indicate by the use of zero (0) any items which are not taxable or deductible. (12 marks) (b)(i) State the period during which HM Revenue and Customs (HMRC) will have to notify Tracy-Ann if they intend to carry out a compliance check in respect of her self-assessment tax return for the tax year 2021- 22, and the likely reason why such a check would be made. (2 marks) (ii) Advise Tracy-Ann as to how long she must retain the records used in preparing her self-assessment tax return for the tax year 2021-22. (1 mark) Tracy-Ann ceased self-employment on 30 June 2021. She was then employed by Kitten ple for the six-month period from 1 August 2021 to 31 January 2022. Tracy-Ann commenced self-employment again, in a new business, on 1 February 2022. Self-employment ceasing on 30 June 2021 1) Tracy-Ann's trading profit for the final 14-month period of trading from 1 May 2020 to 30 June 2021 was E111,600. This figure is before taking account of capital allowances. 2) The tax written down value of the capital allowances main pool at 1 May 2020 was £18,700. On 11 June 2020, Tracy-Ann purchased a printer for £3,700. On the cessation of trading, Tracy-Ann personally retained the printer. Its value on 30 June 2021 was £1,980. The remaining items included in the main pool were sold for £8,500 on 30 June 2021. 3) Tracy-Ann had unused overlap profits brought forward of £23,270 Employment from 1 August 2021 to 31 January 2022 1) During the six-month period from 1 August 2021 to 31 January 2022, Tracy-Ann was paid a gross monthly salary of £12,700 in respect of her employment with Kitten ple. 2) Throughout the period from 1 August 2021 to 31 January 2022, Kitten ple provided Tracy-Ann with living accommodation. The property is rented by Kitten ple at a cost of £710 per month (this is higher than the annual value of the property). Kitten ple also paid for the running costs relating to the property, and for the period 1 August 2021 to 31 January 2022 these amounted to £1,840. 3) Throughout the period from 1 August 2021 to 31 January 2022, Tracy-Ann's three-year-old son was provided with a place at Kitten ple's workplace nursery. The total cost to the company of providing this nursery place was £4,920 (120 days at £41 per day). 4) Tracy-Ann used her private motor car for business purposes. During the period from 1 August 2021 to 31 January 2022, she drove 7,200 miles in the performance of her duties for Kitten ple, for which the company paid an allowance of 37 pence per mile. Self-employment from 1 February 2022 1) Tracy-Ann's trading profit for the first five-month period of trading from 1 February to 30 June 2022 was £57,200. This figure is before taking account of capital allowances. 2) The only item of plant and machinery owned by Tracy- Ann, and used in this business, is office equipment which was purchased for £28,300 on 1 February 2022. Property income 1) During the period 1 August 2021 to 31 January 2022, Tracy-Ann let out her main residence at a monthly rent of £1,600. Tracy-Ann lived in this property up to 31 July 2021 and then again from 1 February 2022 onwards. 2) The only expenditure incurred by Tracy-Ann in respect of the letting was property insurance, which cost £750 for the year ended 5 April 2022. 3) Tracy-Ann has opted to calculate her property income using the accruals basis. Rent-a-room relief is not available in respect of the letting. Self-assessment tax return Tracy-Ann filed her self-assessment tax return for the tax year 2021-22 on 14 August 2022. She is quite confident that all of her income for the tax year 2021-22 was correctly declared and that no deductions were incorrectly claimed Required: (a) Calculate Tracy-Ann's taxable income for the tax year 2021-22. Note: You should indicate by the use of zero (0) any items which are not taxable or deductible. (12 marks) (b)(i) State the period during which HM Revenue and Customs (HMRC) will have to notify Tracy-Ann if they intend to carry out a compliance check in respect of her self-assessment tax return for the tax year 2021- 22, and the likely reason why such a check would be made. (2 marks) (ii) Advise Tracy-Ann as to how long she must retain the records used in preparing her self-assessment tax return for the tax year 2021-22. (1 mark)

Expert Answer:

Answer rating: 100% (QA)

a TracyAnns taxable income for the tax year 202122 is Profit from selfemployment 14 months 11160... View the full answer

Related Book For

Posted Date:

Students also viewed these accounting questions

-

Yaya Berhad intends to purchase equipment for RM1,500,000. The equipment has a 5-year useful life and will be depreciated on a straight-line basis. Addition of the equipment requires additional...

-

Discuss what would be observed as a sample of water is taken along a path that encircles and is close to its critical point.

-

Assume a partner withdraws from a partnership and receives assets of greater value than the book value of his equity. Should the remaining partners share the resulting reduction in their equities in...

-

Access various employment Web sites (for example, www.monster.com and www.dice.com ) and find several job descriptions for a database administrator. Are the job descriptions similar? What are the...

-

What is the cause of the Brownian motion of dust particles? Why aren't larger objects, such as baseballs, similarly affected?

-

Provide a detailed example of two possible personality test items you would suggest they use, and why you would suggest using them.

-

What stakeholder affected by their behavior was Gilead weighting very lightly when it decided what to tell the FDA about the medicines it wished to have permission to sell?

-

Mutual Insurance Company of Iowa (MICI) has a major insurance office facility located in Des Moines, Iowa. The Des Moines office is responsible for processing all of MICIs insurance claims for the...

-

What ways can I make my Relational Data Model conversion meet the following requirements listed below? Am I on the right track? What corrections do I need to address? ERD: My Conversion of ERD onto a...

-

What is the breakeven point (in units) for a firm that has a fixed cost of $300,000 a year, a direct labor cost of $200 per unit, a materials cost of $150 per unit, and a selling price of $500 per...

-

Could you use a cross impact analysis to correlate the attendance at a music festival based on the same festival from the year before? If so, what would be some of the considerations in using this...

-

How do advancements in neuroscience and psychology shed light on the neurobiological processes underlying identity development, including the formation of self-concept, identity consolidation, and...

-

What's your diagnosis of the breach at Target was Target particularly vulnerable or simply unlucky? Then using the Gap analysis, discuss which technical or organizational actions or decisions would...

-

Could you elaborate on the dialectical relationship between identity and power dynamics, exploring how dominant narratives and structures influence the construction, negotiation, and contestation of...

-

Briefly describe the Air Canada 'business model'. How would you evaluate the current IT setup with regard to managing its business? Do you see any risk associated with their IT usage model? How would...

-

The input to the program is an integer variable, opCode and two double variables, X and Y with values 23.45 and 19.82 respectively.Use the table to write program that, based on the value of opCode,...

-

From 1970 to 1990, Sri Lanka's population grew by approximately 2.2 million persons every five years. The population in 1970 was 12.2 million people.What is the best formula for P, Sri Lanka's...

-

Calcium carbonate crystals in the form of aragonite have orthorhombic unit cells of dimensions a= 574.1 pm, b = 796.8 pm, and c= 495.9 pm. Calculate the glancing angles for the (100), (010), and...

-

Account for Le Chatelier's principle in terms of thermodynamic quantities.

-

The enzyme-catalyzed conversion of a substrate at 25C has a Michaelis constant of 0.042 mol dm-3. The rate of the reaction is 2.45 x 10-4 mol dm-3 s-1 when the substrate concentration is 0.890 mol...

-

Why is gifting an important estate planning tool? Why are assets that grow in value recommended as gifts?

-

Following his death in 2012, Zane Wulster's gross taxable estate was valued at $3,300,000. He has made a total of $200,000 of gifts that exceeded the annual gift tax exclusion. a. What is the amount...

-

Explain how the portable estate exemption, resulting from the 2010 Tax Relief Act, altered estate planning using family trusts.

Study smarter with the SolutionInn App