Assume that the security pays an annual coupon and that you are pricing the security on 11-MAY-2023.

Question:

Assume that the security pays an annual coupon and that you are pricing the security on 11-MAY-2023. In addition, assume that the only date on which the embedded option can be exercised is 11-MAY-2026 (i.e. ignore the 11-FEB-2027 date stated in the bond description). You should also assume that interest rate volatility is 20% and that interest rates follow a lognormal model, with an equal probability of an increase and decrease in rates each year (50% & 50%).

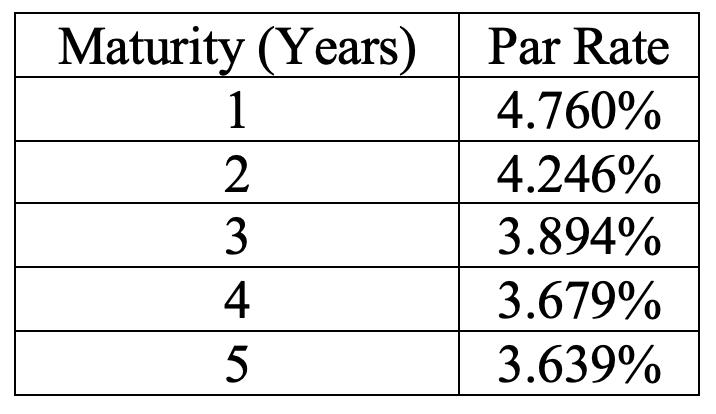

The relevant USD-denominated benchmark par curve is as follows:

Determine the price of this security (as a % of face value) assuming that OAS is equal to 40 bps. Briefly explain why the price you have calculated will not precisely match the theoretical price.

Expert Answer:

To calculate the price of the security we need to perform a binomial tree valuation for the embedded option Here are the steps to calculate the price 1 Determine the cash flows Since the security pays ... View the full answer

Financial Reporting And Analysis

ISBN: 9781260247848

8th Edition

Authors: Lawrence Revsine, Daniel Collins, Bruce Johnson, Fred Mittelstaedt, Leonard Soffer