Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

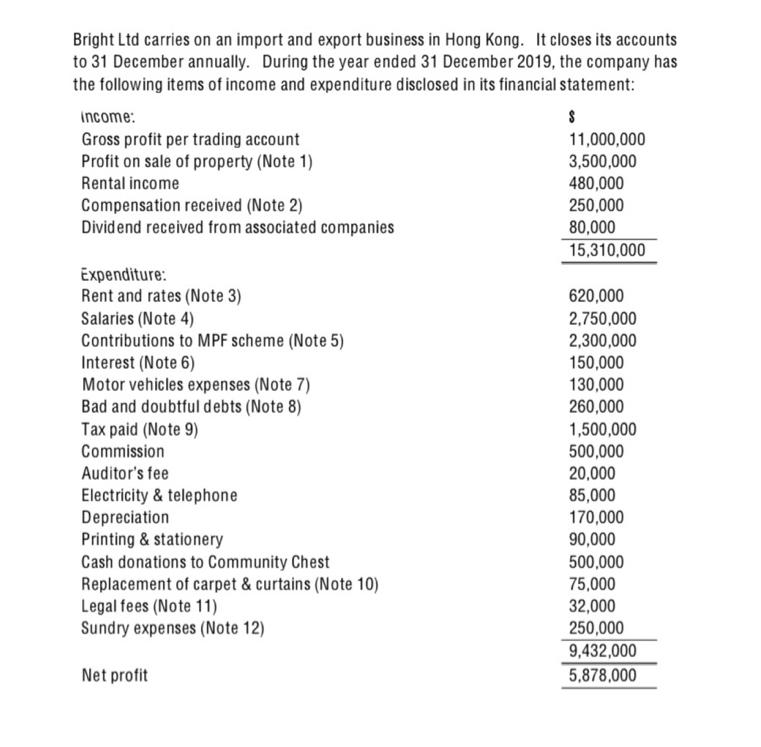

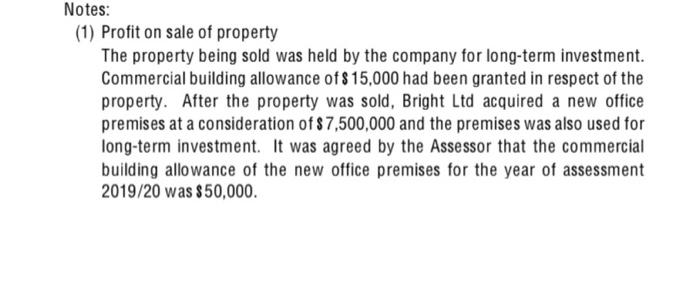

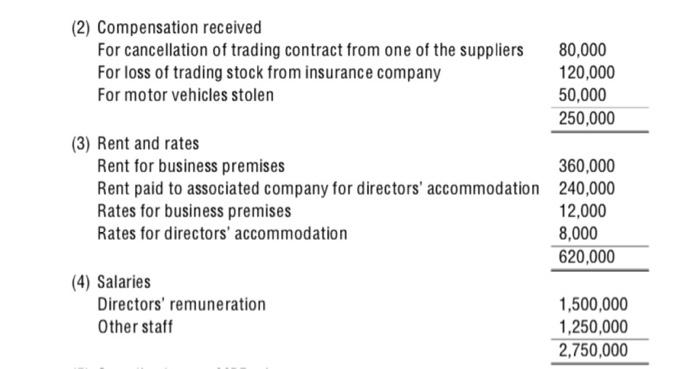

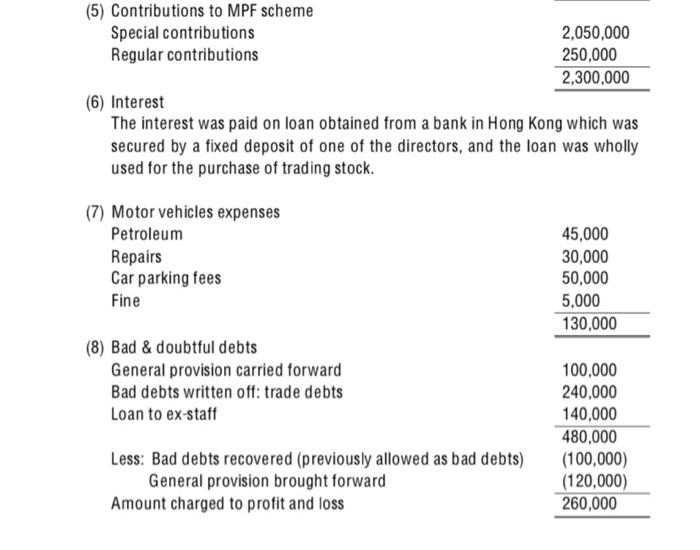

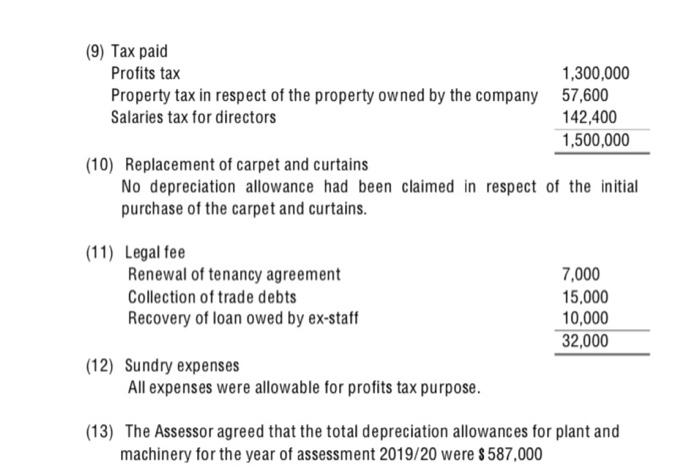

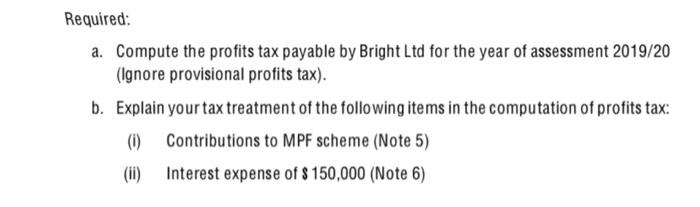

Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts to 31 December annually. During the year ended 31 December 2019, the company has the following items of income and expenditure disclosed in its financial statement: income: Gross profit per trading account Profit on sale of property (Note 1) Rental income Compensation received (Note 2) Dividend received from associated companies Expenditure: Rent and rates (Note 3) Salaries (Note 4) Contributions to MPF scheme (Note 5) Interest (Note 6) Motor vehicles expenses (Note 7) Bad and doubtful debts (Note 8) Tax paid (Note 9) Commission Auditor's fee Electricity & telephone Depreciation Printing & stationery Cash donations to Community Chest Replacement of carpet & curtains (Note 10) Legal fees (Note 11) Sundry expenses (Note 12) Net profit S 11,000,000 3,500,000 480,000 250,000 80,000 15,310,000 620,000 2,750,000 2,300,000 150,000 130,000 260,000 1,500,000 500,000 20,000 85,000 170,000 90,000 500,000 75,000 32,000 250,000 9,432,000 5,878,000 Notes: (1) Profit on sale of property The property being sold was held by the company for long-term investment. Commercial building allowance of $15,000 had been granted in respect of the property. After the property was sold, Bright Ltd acquired a new office premises at a consideration of $7,500,000 and the premises was also used for long-term investment. It was agreed by the Assessor that the commercial building allowance of the new office premises for the year of assessment 2019/20 was $50,000. (2) Compensation received For cancellation of trading contract from one of the suppliers For loss of trading stock from insurance company For motor vehicles stolen (3) Rent and rates Rent for business premises 360,000 Rent paid to associated company for directors' accommodation 240,000 Rates for business premises 12,000 Rates for directors' accommodation 8,000 620,000 (4) Salaries 80,000 120,000 50,000 250,000 Directors' remuneration Other staff 1,500,000 1,250,000 2,750,000 (5) Contributions to MPF scheme Special contributions Regular contributions (6) Interest The interest was paid on loan obtained from a bank in Hong Kong which was secured by a fixed deposit of one of the directors, and the loan was wholly used for the purchase of trading stock. (7) Motor vehicles expenses Petroleum Repairs Car parking fees Fine (8) Bad & doubtful debts General provision carried forward Bad debts written off: trade debts Loan to ex-staff Less: Bad debts recovered (previously allowed as bad debts) General provision brought forward 2,050,000 250,000 2,300,000 Amount charged to profit and loss 45,000 30,000 50,000 5,000 130,000 100,000 240,000 140,000 480,000 (100,000) (120,000) 260,000 (9) Tax paid Profits tax 1,300,000 Property tax in respect of the property owned by the company 57,600 Salaries tax for directors 142,400 1,500,000 (10) Replacement of carpet and curtains No depreciation allowance had been claimed in respect of the initial purchase of the carpet and curtains. (11) Legal fee Renewal of tenancy agreement Collection of trade debts Recovery of loan owed by ex-staff (12) Sundry expenses All expenses were allowable for profits tax purpose. 7,000 15,000 10,000 32,000 (13) The Assessor agreed that the total depreciation allowances for plant and machinery for the year of assessment 2019/20 were $587,000 Required: a. Compute the profits tax payable by Bright Ltd for the year of assessment 2019/20 (Ignore provisional profits tax). b. Explain your tax treatment of the following items in the computation of profits tax: (i) Contributions to MPF scheme (Note 5) (ii) Interest expense of $ 150,000 (Note 6) Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts to 31 December annually. During the year ended 31 December 2019, the company has the following items of income and expenditure disclosed in its financial statement: income: Gross profit per trading account Profit on sale of property (Note 1) Rental income Compensation received (Note 2) Dividend received from associated companies Expenditure: Rent and rates (Note 3) Salaries (Note 4) Contributions to MPF scheme (Note 5) Interest (Note 6) Motor vehicles expenses (Note 7) Bad and doubtful debts (Note 8) Tax paid (Note 9) Commission Auditor's fee Electricity & telephone Depreciation Printing & stationery Cash donations to Community Chest Replacement of carpet & curtains (Note 10) Legal fees (Note 11) Sundry expenses (Note 12) Net profit S 11,000,000 3,500,000 480,000 250,000 80,000 15,310,000 620,000 2,750,000 2,300,000 150,000 130,000 260,000 1,500,000 500,000 20,000 85,000 170,000 90,000 500,000 75,000 32,000 250,000 9,432,000 5,878,000 Notes: (1) Profit on sale of property The property being sold was held by the company for long-term investment. Commercial building allowance of $15,000 had been granted in respect of the property. After the property was sold, Bright Ltd acquired a new office premises at a consideration of $7,500,000 and the premises was also used for long-term investment. It was agreed by the Assessor that the commercial building allowance of the new office premises for the year of assessment 2019/20 was $50,000. (2) Compensation received For cancellation of trading contract from one of the suppliers For loss of trading stock from insurance company For motor vehicles stolen (3) Rent and rates Rent for business premises 360,000 Rent paid to associated company for directors' accommodation 240,000 Rates for business premises 12,000 Rates for directors' accommodation 8,000 620,000 (4) Salaries 80,000 120,000 50,000 250,000 Directors' remuneration Other staff 1,500,000 1,250,000 2,750,000 (5) Contributions to MPF scheme Special contributions Regular contributions (6) Interest The interest was paid on loan obtained from a bank in Hong Kong which was secured by a fixed deposit of one of the directors, and the loan was wholly used for the purchase of trading stock. (7) Motor vehicles expenses Petroleum Repairs Car parking fees Fine (8) Bad & doubtful debts General provision carried forward Bad debts written off: trade debts Loan to ex-staff Less: Bad debts recovered (previously allowed as bad debts) General provision brought forward 2,050,000 250,000 2,300,000 Amount charged to profit and loss 45,000 30,000 50,000 5,000 130,000 100,000 240,000 140,000 480,000 (100,000) (120,000) 260,000 (9) Tax paid Profits tax 1,300,000 Property tax in respect of the property owned by the company 57,600 Salaries tax for directors 142,400 1,500,000 (10) Replacement of carpet and curtains No depreciation allowance had been claimed in respect of the initial purchase of the carpet and curtains. (11) Legal fee Renewal of tenancy agreement Collection of trade debts Recovery of loan owed by ex-staff (12) Sundry expenses All expenses were allowable for profits tax purpose. 7,000 15,000 10,000 32,000 (13) The Assessor agreed that the total depreciation allowances for plant and machinery for the year of assessment 2019/20 were $587,000 Required: a. Compute the profits tax payable by Bright Ltd for the year of assessment 2019/20 (Ignore provisional profits tax). b. Explain your tax treatment of the following items in the computation of profits tax: (i) Contributions to MPF scheme (Note 5) (ii) Interest expense of $ 150,000 (Note 6) Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts to 31 December annually. During the year ended 31 December 2019, the company has the following items of income and expenditure disclosed in its financial statement: income: Gross profit per trading account Profit on sale of property (Note 1) Rental income Compensation received (Note 2) Dividend received from associated companies Expenditure: Rent and rates (Note 3) Salaries (Note 4) Contributions to MPF scheme (Note 5) Interest (Note 6) Motor vehicles expenses (Note 7) Bad and doubtful debts (Note 8) Tax paid (Note 9) Commission Auditor's fee Electricity & telephone Depreciation Printing & stationery Cash donations to Community Chest Replacement of carpet & curtains (Note 10) Legal fees (Note 11) Sundry expenses (Note 12) Net profit S 11,000,000 3,500,000 480,000 250,000 80,000 15,310,000 620,000 2,750,000 2,300,000 150,000 130,000 260,000 1,500,000 500,000 20,000 85,000 170,000 90,000 500,000 75,000 32,000 250,000 9,432,000 5,878,000 Notes: (1) Profit on sale of property The property being sold was held by the company for long-term investment. Commercial building allowance of $15,000 had been granted in respect of the property. After the property was sold, Bright Ltd acquired a new office premises at a consideration of $7,500,000 and the premises was also used for long-term investment. It was agreed by the Assessor that the commercial building allowance of the new office premises for the year of assessment 2019/20 was $50,000. (2) Compensation received For cancellation of trading contract from one of the suppliers For loss of trading stock from insurance company For motor vehicles stolen (3) Rent and rates Rent for business premises 360,000 Rent paid to associated company for directors' accommodation 240,000 Rates for business premises 12,000 Rates for directors' accommodation 8,000 620,000 (4) Salaries 80,000 120,000 50,000 250,000 Directors' remuneration Other staff 1,500,000 1,250,000 2,750,000 (5) Contributions to MPF scheme Special contributions Regular contributions (6) Interest The interest was paid on loan obtained from a bank in Hong Kong which was secured by a fixed deposit of one of the directors, and the loan was wholly used for the purchase of trading stock. (7) Motor vehicles expenses Petroleum Repairs Car parking fees Fine (8) Bad & doubtful debts General provision carried forward Bad debts written off: trade debts Loan to ex-staff Less: Bad debts recovered (previously allowed as bad debts) General provision brought forward 2,050,000 250,000 2,300,000 Amount charged to profit and loss 45,000 30,000 50,000 5,000 130,000 100,000 240,000 140,000 480,000 (100,000) (120,000) 260,000 (9) Tax paid Profits tax 1,300,000 Property tax in respect of the property owned by the company 57,600 Salaries tax for directors 142,400 1,500,000 (10) Replacement of carpet and curtains No depreciation allowance had been claimed in respect of the initial purchase of the carpet and curtains. (11) Legal fee Renewal of tenancy agreement Collection of trade debts Recovery of loan owed by ex-staff (12) Sundry expenses All expenses were allowable for profits tax purpose. 7,000 15,000 10,000 32,000 (13) The Assessor agreed that the total depreciation allowances for plant and machinery for the year of assessment 2019/20 were $587,000 Required: a. Compute the profits tax payable by Bright Ltd for the year of assessment 2019/20 (Ignore provisional profits tax). b. Explain your tax treatment of the following items in the computation of profits tax: (i) Contributions to MPF scheme (Note 5) (ii) Interest expense of $ 150,000 (Note 6) Bright Ltd carries on an import and export business in Hong Kong. It closes its accounts to 31 December annually. During the year ended 31 December 2019, the company has the following items of income and expenditure disclosed in its financial statement: income: Gross profit per trading account Profit on sale of property (Note 1) Rental income Compensation received (Note 2) Dividend received from associated companies Expenditure: Rent and rates (Note 3) Salaries (Note 4) Contributions to MPF scheme (Note 5) Interest (Note 6) Motor vehicles expenses (Note 7) Bad and doubtful debts (Note 8) Tax paid (Note 9) Commission Auditor's fee Electricity & telephone Depreciation Printing & stationery Cash donations to Community Chest Replacement of carpet & curtains (Note 10) Legal fees (Note 11) Sundry expenses (Note 12) Net profit S 11,000,000 3,500,000 480,000 250,000 80,000 15,310,000 620,000 2,750,000 2,300,000 150,000 130,000 260,000 1,500,000 500,000 20,000 85,000 170,000 90,000 500,000 75,000 32,000 250,000 9,432,000 5,878,000 Notes: (1) Profit on sale of property The property being sold was held by the company for long-term investment. Commercial building allowance of $15,000 had been granted in respect of the property. After the property was sold, Bright Ltd acquired a new office premises at a consideration of $7,500,000 and the premises was also used for long-term investment. It was agreed by the Assessor that the commercial building allowance of the new office premises for the year of assessment 2019/20 was $50,000. (2) Compensation received For cancellation of trading contract from one of the suppliers For loss of trading stock from insurance company For motor vehicles stolen (3) Rent and rates Rent for business premises 360,000 Rent paid to associated company for directors' accommodation 240,000 Rates for business premises 12,000 Rates for directors' accommodation 8,000 620,000 (4) Salaries 80,000 120,000 50,000 250,000 Directors' remuneration Other staff 1,500,000 1,250,000 2,750,000 (5) Contributions to MPF scheme Special contributions Regular contributions (6) Interest The interest was paid on loan obtained from a bank in Hong Kong which was secured by a fixed deposit of one of the directors, and the loan was wholly used for the purchase of trading stock. (7) Motor vehicles expenses Petroleum Repairs Car parking fees Fine (8) Bad & doubtful debts General provision carried forward Bad debts written off: trade debts Loan to ex-staff Less: Bad debts recovered (previously allowed as bad debts) General provision brought forward 2,050,000 250,000 2,300,000 Amount charged to profit and loss 45,000 30,000 50,000 5,000 130,000 100,000 240,000 140,000 480,000 (100,000) (120,000) 260,000 (9) Tax paid Profits tax 1,300,000 Property tax in respect of the property owned by the company 57,600 Salaries tax for directors 142,400 1,500,000 (10) Replacement of carpet and curtains No depreciation allowance had been claimed in respect of the initial purchase of the carpet and curtains. (11) Legal fee Renewal of tenancy agreement Collection of trade debts Recovery of loan owed by ex-staff (12) Sundry expenses All expenses were allowable for profits tax purpose. 7,000 15,000 10,000 32,000 (13) The Assessor agreed that the total depreciation allowances for plant and machinery for the year of assessment 2019/20 were $587,000 Required: a. Compute the profits tax payable by Bright Ltd for the year of assessment 2019/20 (Ignore provisional profits tax). b. Explain your tax treatment of the following items in the computation of profits tax: (i) Contributions to MPF scheme (Note 5) (ii) Interest expense of $ 150,000 (Note 6)

Expert Answer:

Answer rating: 100% (QA)

Required Compute the profits tax payable by Bright Ltd for the year of assessment 201920 Ignore p... View the full answer

Related Book For

Advanced Accounting

ISBN: 978-0538480284

11th edition

Authors: Paul M. Fischer, William J. Tayler, Rita H. Cheng

Posted Date:

Students also viewed these general management questions

-

During the year ended 30 June 2019 XYZ Pty Limited, a resident Australian private company (non BRE), received a franked dividend of $10,800 with $3,200 of attached franking credits. XYZ Pty Limited...

-

The Viking Corporation has the following items of income for 2016: Operating income ........................................................ $350,000 Dividend income (12%-owned corporations)...

-

During the year ended December 31, 2014, Bowersox International Corporation earned $ 3,500,000 in net income after taxes. The company reported $ 100,000 of net unrealized gains on available-for-sale...

-

Route Canal Shipping Company has the following schedule for aging of accounts receivable: AGE OF RECEIVABLES APRIL 30, 2001 a. Fill in column (4) for each month. b. If the firm had $1,440,000 in...

-

On February 1, 2014, Holl Co. decides to invest excess cash of $ 20,000 by purchasing 1,000 shares of Cooke, Inc. stock at $ 20 per share. At year- end, December 31, 2014, Cookes market price was $...

-

Morris Corporation has current liabilities of $800 million, and its current ratio is 2.5. What is its level of current assets? ($2,000 million) If this firms quick ratio is 2, how much inventory does...

-

For the following products and countries, identify the type of warehouse that should be used as well as the method of transportation that should deliver the product to end users. Using the Internet,...

-

(Entries for Bond Transactions) Presented below are two independent situations. 1. On January 1, 2010, Divac Company issued $300,000 of 9%, 10-year bonds at par. Interest is payable quarterly on...

-

Without using row reduction, apply block operation on A to compute its inverse. [1 2000 3 50 00 A=0 0 2 00 0007 8 0 0056

-

A simple ac generator consists of a coil with 10 turns (each turn has an area of 50 cm2). The coil rotates in a uniform magnetic field of 350 mT with a frequency of 60 Hz. (a) Write an expression in...

-

Let -3 -2 4 A = 0. 3. -2 -2 3 If possible, find an invertible matrix P so that D PAP is a diagonal matrix. If it is not possible, enter the identity matrix for P and the matrix A for D. You must...

-

Choose one type of disability management provider (third-party insurance, employer-based, WCB, unionized employer-based). Describe the providers role and the benefits and challenges associated with...

-

Company: Bravura Solutions Limited Using the 2022 Annual Report Each group member should identify one additional inherent risk that was not an actual KAM (each group member must have a different...

-

James has been in his management position for many years and is comfortable there. Recently, the CEO has been applying pressure on James to get his department to become more computer literate,...

-

September 2021, Australia cancelled a $90mAUD submarine deal with France following the announcement of AUKUS, a security-pact alliance between the USA, UK, and Australia. Do some further research on...

-

The following partial financial Information (in thousands of dollars) is available for Thole, Incorporated: Corporate overhead costs at Thole are allocated to divisions based on relative sales....

-

You purchase a property for $125,000. Your cash flow from the first year is $6,000. Each year, your cash flow grows by 3%. After 4 years (4 cash flows), you sell the property for $175,000. What is...

-

Suppose the market is semistrong form efficient. Can you expect to earn excess returns if you make trades based on? a. Your brokers information about record earnings for a stock? b. Rumors about a...

-

Refer to the preceding facts for Postmans acquisition of 80% of Spartans common stock and the bond transactions. Postman uses the simple equity method to account for its investment in Spartan. On...

-

On June 30, 2015, the shareholders equity of Fabinet, a foreign corporation, was 10,500,000 FC. At that time, Newcore, a U.S. corporation, acquired 40% in Fabinet by paying $3,120,000 when 1 FC was...

-

Company S has the following stockholders equity on January 1, 2015: Common stock ($1par, 100,000 shares) ............... $100,000 6%preferred stock ($100par, 2,000 shares ............. 200,000...

-

Describe and compare the properties of the least squares and generalized least squares estimators when heteroskedasticity exists.

-

Test for heteroskedasticity using a Goldfeld-Quandt test applied to (a) two subsamples with potentially different variances and (b) a model where the variance is hypothesized to depend on an...

-

Explain why the linear probability model exhibits heteroskedasticity.

Study smarter with the SolutionInn App