Question

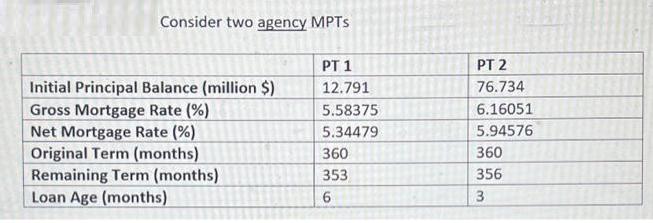

Consider two agency MPTS Initial Principal Balance (million $) Gross Mortgage Rate (%) Net Mortgage Rate (%) Original Term (months) Remaining Term (months) Loan

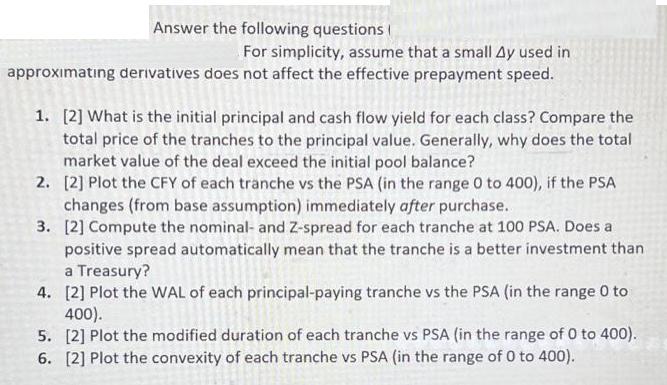

Consider two agency MPTS Initial Principal Balance (million $) Gross Mortgage Rate (%) Net Mortgage Rate (%) Original Term (months) Remaining Term (months) Loan Age (months) PT 1 12.791 5.58375 5.34479 360 353 6 PT 2 76.734 6.16051 5.94576 360 356 3 Answer the following questions For simplicity, assume that a small Ay used in approximating derivatives does not affect the effective prepayment speed. 1. [2] What is the initial principal and cash flow yield for each class? Compare the total price of the tranches to the principal value. Generally, why does the total market value of the deal exceed the initial pool balance? 2. [2] Plot the CFY of each tranche vs the PSA (in the range 0 to 400), if the PSA changes (from base assumption) immediately after purchase. 3. [2] Compute the nominal- and Z-spread for each tranche at 100 PSA. Does a positive spread automatically mean that the tranche is a better investment than a Treasury? 4. [2] Plot the WAL of each principal-paying tranche vs the PSA (in the range 0 to 400). 5. [2] Plot the modified duration of each tranche vs PSA (in the range of 0 to 400). 6. [2] Plot the convexity of each tranche vs PSA (in the range of 0 to 400).

Step by Step Solution

3.33 Rating (108 Votes )

There are 3 Steps involved in it

Step: 1

price couponpvaf ytm5redemptionpvif ytm5 1039923 Modified duration and c...

Get Instant Access with AI-Powered Solutions

See step-by-step solutions with expert insights and AI powered tools for academic success

Step: 2

Step: 3

Ace Your Homework with AI

Get the answers you need in no time with our AI-driven, step-by-step assistance

Get Started

Financial Reporting Financial Statement Analysis And Valuation A Strategic Perspective

Authors: James M. Wahlen, Stephen P. Baginski, Mark Bradshaw

9th Edition

1337614689, 1337614688, 9781337668262, 978-1337614689