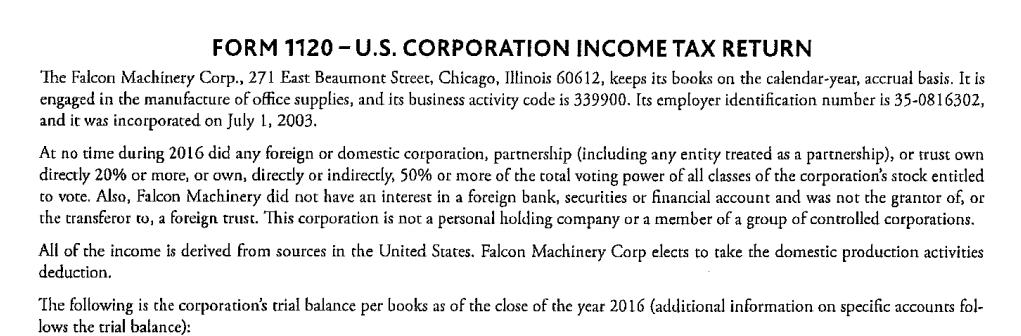

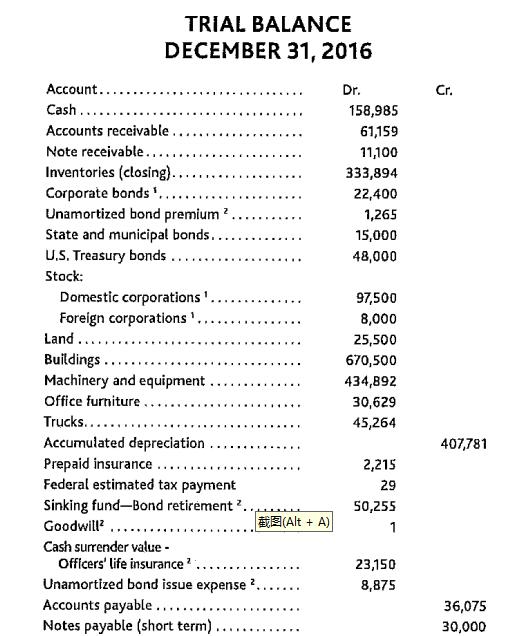

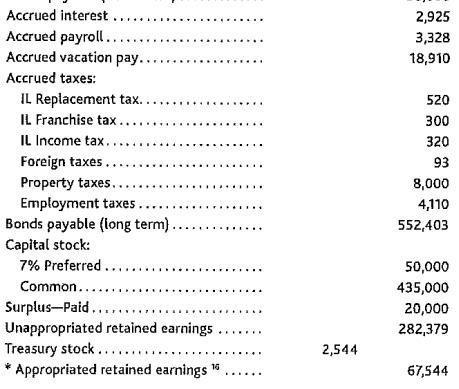

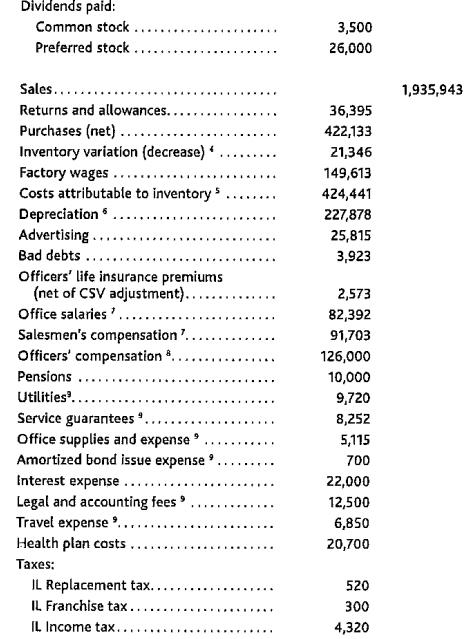

FORM 1120-U.S. CORPORATION INCOME TAX RETURN The Falcon Machinery Corp., 271 East Beaumont Street, Chicago, Illinois...

Fantastic news! We've Found the answer you've been seeking!

Question:

Transcribed Image Text:

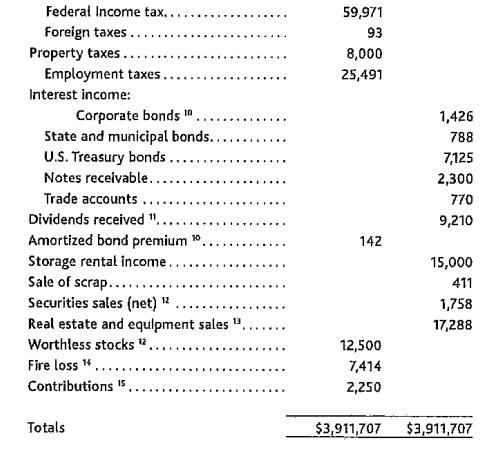

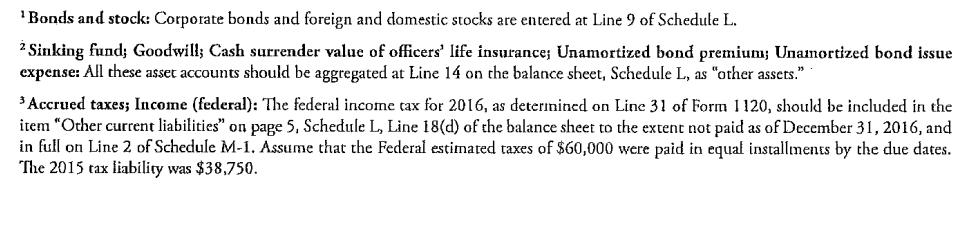

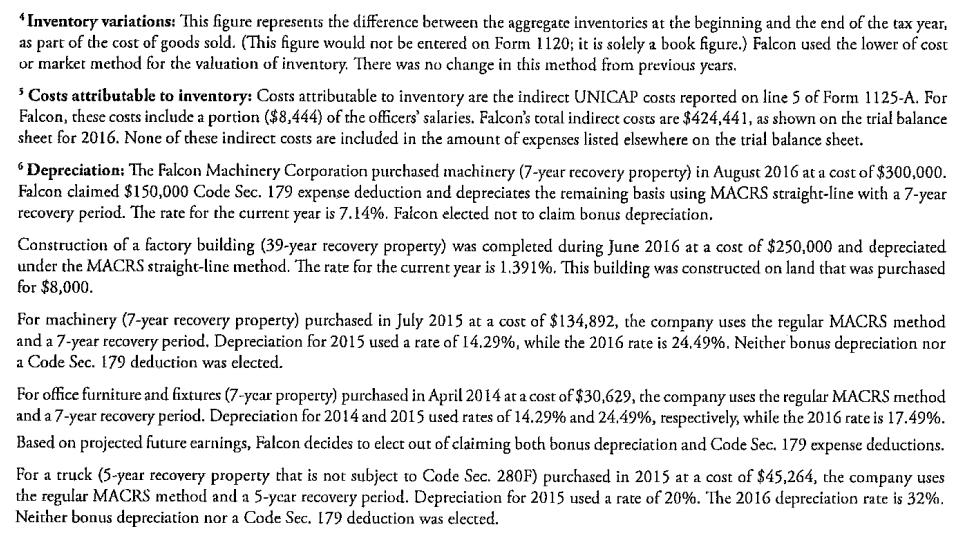

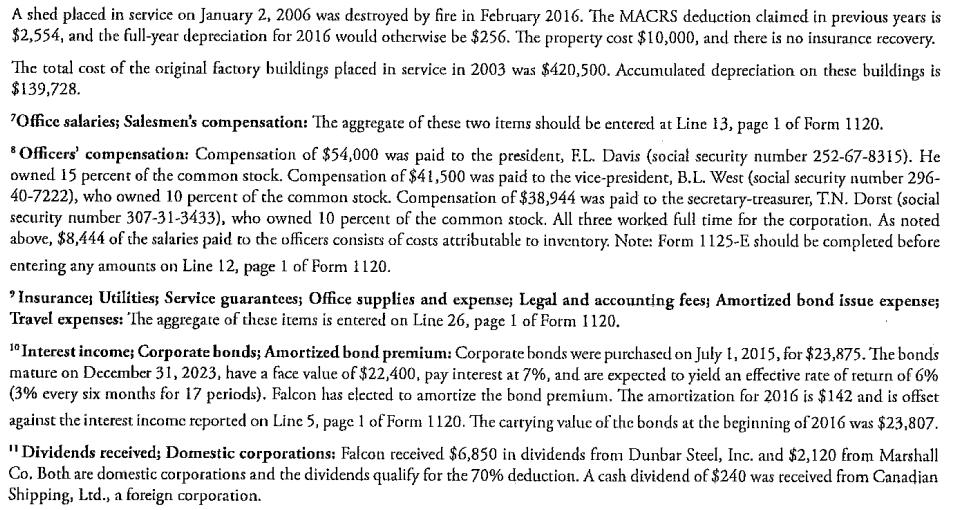

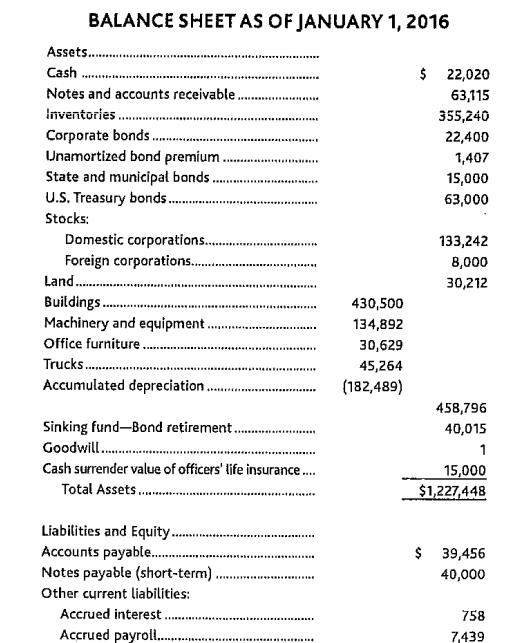

FORM 1120-U.S. CORPORATION INCOME TAX RETURN The Falcon Machinery Corp., 271 East Beaumont Street, Chicago, Illinois 60612, keeps its books on the calendar-year, accrual basis. It is engaged in the manufacture of office supplies, and its business activity code is 339900. Its employer identification number is 35-0816302, and it was incorporated on July 1, 2003. At no time during 2016 did any foreign or domestic corporation, partnership (including any entity treated as a partnership), or trust own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of the corporation's stock entitled to vote. Also, Falcon Machinery did not have an interest in a foreign bank, securities or financial account and was not the grantor of, or the transferor to, a foreign trust. This corporation is not a personal holding company or a member of a group of controlled corporations. All of the income is derived from sources in the United States. Falcon Machinery Corp elects to take the domestic production activities deduction. The following is the corporation's trial balance per books as of the close of the year 2016 (additional information on specific accounts fol- lows the trial balance): TRIAL BALANCE DECEMBER 31, 2016 Account.. Dr. Cr. Cash... 158,985 Accounts receivable.. 61,159 Note receivable... 11,100 Inventories (closing).. 333,894 Corporate bonds'.. 22,400 Unamortized bond premium 2. 1,265 State and municipal bonds... 15,000 U.S. Treasury bonds 48,000 Stock: Domestic corporations'. 97,500 Foreign corporations'. 8,000 Land 25,500 Buildings.... 670,500 Machinery and equipment. 434,892 Office furniture.... 30,629 Trucks........ 45,264 Accumulated depreciation. 407,781 Prepaid insurance .. 2,215 Federal estimated tax payment 29 Sinking fund-Bond retirement?. 50,255 Goodwill.... (Alt+A) 1 Cash surrender value - Officers' life insurance 2 23,150 Unamortized bond issue expense 2. 8,875 Accounts payable......... 36,075 Notes payable (short term). 30,000 Accrued interest .... 2,925 Accrued payroll... 3,328 Accrued vacation pay. 18,910 Accrued taxes: IL Replacement tax.... 520 IL Franchise tax.... 300 IL Income tax..... 320 Foreign taxes.. 93 Property taxes..... 8,000 Employment taxes.... 4,110 Bonds payable (long term)...... 552,403 Capital stock: 7% Preferred...... Common...... Surplus-Paid...... Unappropriated retained earnings. Treasury stock.... 50,000 435,000 20,000 282,379 2,544 * Appropriated retained earnings 16 67,544 Dividends paid: Common stock Preferred stock 3,500 26,000 Sales........ 1,935,943 Returns and allowances... 36,395 Purchases (net).... 422,133 Inventory variation (decrease) * 21,346 Factory wages.... 149,613 Costs attributable to inventory > 5 424,441 Depreciation 227,878 Advertising. 25,815 Bad debts.... 3,923 Officers' life insurance premiums (net of CSV adjustment)........ 2,573 Office salaries'... 82,392 Salesmen's compensation'.. 91,703 Officers' compensation *. 126,000 Pensions 10,000 Utilities'... 9,720 Service guarantees 9. 8,252 Office supplies and expense 5,115 Amortized bond issue expense 700 Interest expense. 22,000 Legal and accounting fees' 12,500 Travel expense ⁹....... 6,850 Health plan costs. 20,700 Taxes: IL Replacement tax... 520 IL Franchise tax... 300 IL Income tax... 4,320 Federal Income tax.. Foreign taxes. Property taxes... Employment taxes. Interest income: Corporate bonds 10 State and municipal bonds... U.S. Treasury bonds..... Notes receivable... Trade accounts Dividends received ".. 59,971 93 8,000 25,491 1,426 788 7,125 2,300 770 9,210 Amortized bond premium 10 142 Storage rental income... Sale of scrap....... Securities sales (net) 12 15,000 411 1,758 Real estate and equipment sales 13, 17,288 Worthless stocks 12 Fire loss ..... 14 12,500 7,414 Contributions 15 Totals 2,250 $3,911,707 $3,911,707 Bonds and stock: Corporate bonds and foreign and domestic stocks are entered at Line 9 of Schedule L. 2 Sinking fund; Goodwill; Cash surrender value of officers' life insurance; Unamortized bond premium; Unamortized bond issue expense: All these asset accounts should be aggregated at Line 14 on the balance sheet, Schedule L, as "other assets." 3 Accrued taxes; Income (federal): The federal income tax for 2016, as determined on Line 31 of Form 1120, should be included in the item "Other current liabilities" on page 5, Schedule L, Line 18(d) of the balance sheet to the extent not paid as of December 31, 2016, and in full on Line 2 of Schedule M-1. Assume that the Federal estimated taxes of $60,000 were paid in equal installments by the due dates. The 2015 tax liability was $38,750. "Inventory variations: This figure represents the difference between the aggregate inventories at the beginning and the end of the tax year, as part of the cost of goods sold. (This figure would not be entered on Form 1120; it is solely a book figure.) Falcon used the lower of cost or market method for the valuation of inventory. There was no change in this method from previous years. 5 Costs attributable to inventory: Costs attributable to inventory are the indirect UNICAP costs reported on line 5 of Form 1125-A. For Falcon, these costs include a portion ($8,444) of the officers' salaries. Falcon's total indirect costs are $424,441, as shown on the trial balance sheet for 2016. None of these indirect costs are included in the amount of expenses listed elsewhere on the trial balance sheet. Depreciation: The Falcon Machinery Corporation purchased machinery (7-year recovery property) in August 2016 at a cost of $300,000. Falcon claimed $150,000 Code Sec. 179 expense deduction and depreciates the remaining basis using MACRS straight-line with a 7-year recovery period. The rate for the current year is 7.14%. Falcon elected not to claim bonus depreciation. Construction of a factory building (39-year recovery property) was completed during June 2016 at a cost of $250,000 and depreciated under the MACRS straight-line method. The rate for the current year is 1.391%. This building was constructed on land that was purchased for $8,000. For machinery (7-year recovery property) purchased in July 2015 at a cost of $134,892, the company uses the regular MACRS method and a 7-year recovery period. Depreciation for 2015 used a rate of 14.29%, while the 2016 rate is 24.49%. Neither bonus depreciation nor a Code Sec. 179 deduction was elected. For office furniture and fixtures (7-year property) purchased in April 2014 at a cost of $30,629, the company uses the regular MACRS method and a 7-year recovery period. Depreciation for 2014 and 2015 used rates of 14.29% and 24.49%, respectively, while the 2016 rate is 17.49%. Based on projected future earnings, Falcon decides to elect out of claiming both bonus depreciation and Code Sec. 179 expense deductions. For a truck (5-year recovery property that is not subject to Code Sec. 280F) purchased in 2015 at a cost of $45,264, the company uses the regular MACRS method and a 5-year recovery period. Depreciation for 2015 used a rate of 20%. The 2016 depreciation rate is 32%. Neither bonus depreciation nor a Code Sec. 179 deduction was elected. A shed placed in service on January 2, 2006 was destroyed by fire in February 2016. The MACRS deduction claimed in previous years is $2,554, and the full-year depreciation for 2016 would otherwise be $256. The property cost $10,000, and there is no insurance recovery. The total cost of the original factory buildings placed in service in 2003 was $420,500. Accumulated depreciation on these buildings is $139,728. 'Office salaries; Salesmen's compensation: The aggregate of these two items should be entered at Line 13, page 1 of Form 1120. Officers' compensation: Compensation of $54,000 was paid to the president, F.L. Davis (social security number 252-67-8315). He owned 15 percent of the common stock. Compensation of $41,500 was paid to the vice-president, B.L. West (social security number 296- 40-7222), who owned 10 percent of the common stock. Compensation of $38,944 was paid to the secretary-treasurer, T.N. Dorst (social security number 307-31-3433), who owned 10 percent of the common stock. All three worked full time for the corporation. As noted above, $8,444 of the salaries paid to the officers consists of costs attributable to inventory. Note: Form 1125-E should be completed before entering any amounts on Line 12, page 1 of Form 1120. "Insurance; Utilities; Service guarantees; Office supplies and expense; Legal and accounting fees; Amortized bond issue expense; Travel expenses: 'The aggregate of these items is entered on Line 26, page 1 of Form 1120. 10 Interest income; Corporate bonds; Amortized bond premium: Corporate bonds were purchased on July 1, 2015, for $23,875. The bonds mature on December 31, 2023, have a face value of $22,400, pay interest at 7%, and are expected to yield an effective rate of return of 6% (3% every six months for 17 periods). Falcon has elected to amortize the bond premium. The amortization for 2016 is $142 and is offset against the interest income reported on Line 5, page 1 of Form 1120. The carrying value of the bonds at the beginning of 2016 was $23,807. "Dividends received; Domestic corporations: Falcon received $6,850 in dividends from Dunbar Steel, Inc. and $2,120 from Marshall Co. Both are domestic corporations and the dividends qualify for the 70% deduction. A cash dividend of $240 was received from Canadian Shipping, Ltd., a foreign corporation. 12 Securities sales and worthless stock: On February 3, 2016, the corporation sold 100 shares of XYZ Corp. stock for $20,500. The stock was bought on May 26, 2015, for $18,487. On January 26, 2016, the corporation sold 200 shares of ABC Corp. preferred stock for $4,400. The stock had cost $4,755 on April 14, 2015. On May 14, 2016, the corporation sold for $15,100, net, U.S. Treasury bonds which had cost $15,000 on June 9, 2010. A 1099-B was received for these sales with the basis reported to the IRS. Further, 250 shares of Zero Corp. common stock became worthless in 2016. It was acquired on January 30, 2005, for $12,500, which was its adjusted basis at the time it became worthless. 13 Real estate sale: On July 5, 2016, the corporation sold vacant land for $30,000. It paid $12,712 for the land on June 1, 2006. The land had been used in the corporation's business. (The sale would be reported on Form 4797, Part I, and the gain should be carried over to Schedule D, Line 11.) 14 Fire loss: A shed used by the corporation in its manufacturing was destroyed by fire in February 2016. There was no insurance recovery. The shed had been acquired on January 2, 2006, at a cost of $10,000. Accumulated depreciation of $2,554 had been deducted prior to 2016. The shed had a fair market value of $3,000 prior to the fire, and a zero fair market value after the fire. 15 Contributions: Contributions were made to the following organizations: United Charities, $750; Boy Scouts of America, $500; Red Cross, $250; and Community Fund, $750. 16 Appropriated retained earnings: This figure includes appropriations of $50,000 for sinking fund requirements (bond retirement fund), $15,000 for contingencies, and $2,544 for the cost of treasury stock. During 2016, there were appropriations of $10,000 to the sinking fund reserve and $3,000 to the contingency reserve. BALANCE SHEET AS OF JANUARY 1, 2016 Assets............... Cash............... Notes and accounts receivable......... Inventories............ Corporate bonds....... Unamortized bond premium....... State and municipal bonds. U.S. Treasury bonds......... Stocks: Domestic corporations............. $ 22,020 63,115 355,240 22,400 1,407 15,000 63,000 133,242 Foreign corporation.......... 8,000 Land............... 30,212 Building............ 430,500 Machinery and equipment.. 134,892 Office furniture....... 30,629 Trucks.............. 45,264 Accumulated depreciation...... (182,489) 458,796 Sinking fund-Bond retirement.. 40,015 Goodwill............ 1 Cash surrender value of officers' life insurance.... 15,000 Total Assets.......... $1,227,448 Liabilities and Equity. Accounts payable.......... Notes payable (short-term) Other current liabilities: Accrued interest. Accrued payroll......... $ 39,456 40,000 758 7,439 Accrued vacation pay. 24,578 Accrued state income tax......... 4,185 Accrued property tax......... Accrued employment taxes.. 7,200 26,453 Bonds payable (long term). 225,000 Capital stock: 7% Preferred... Common ....... 50,000 435,000 Paid in surplus... 20,000 Treasury stock... (2,544) Retained Earnings: Unappropriated retained earnings. 295,379 Appropriated retained earnings......... Total Liabilities and Equity...... 54,544 $1,227,448 Additional Information The corporation had a $100 capital loss carryover from 2015. The corporation furnished the Government with information returns on Forms 1096 and 1099 for the dividends it paid during 2016 and also for other payments it made that required information returns. For purposes of the signatures on page 1 of Form 1120, it is assumed that John Service, of John Service, CPA, P.C. (EIN 36-1120987) pre- pared the return. His address is 1510 Steward Building, Suite 1500, Chicago, Illinois 60672; telephone number 312-555-1120; his PTIN is P11624121; and F.L. Davis, President, has authorized John to discuss Falcon Machinery Inc.'s tax return with the IRS. FORM 1120-U.S. CORPORATION INCOME TAX RETURN The Falcon Machinery Corp., 271 East Beaumont Street, Chicago, Illinois 60612, keeps its books on the calendar-year, accrual basis. It is engaged in the manufacture of office supplies, and its business activity code is 339900. Its employer identification number is 35-0816302, and it was incorporated on July 1, 2003. At no time during 2016 did any foreign or domestic corporation, partnership (including any entity treated as a partnership), or trust own directly 20% or more, or own, directly or indirectly, 50% or more of the total voting power of all classes of the corporation's stock entitled to vote. Also, Falcon Machinery did not have an interest in a foreign bank, securities or financial account and was not the grantor of, or the transferor to, a foreign trust. This corporation is not a personal holding company or a member of a group of controlled corporations. All of the income is derived from sources in the United States. Falcon Machinery Corp elects to take the domestic production activities deduction. The following is the corporation's trial balance per books as of the close of the year 2016 (additional information on specific accounts fol- lows the trial balance): TRIAL BALANCE DECEMBER 31, 2016 Account.. Dr. Cr. Cash... 158,985 Accounts receivable.. 61,159 Note receivable... 11,100 Inventories (closing).. 333,894 Corporate bonds'.. 22,400 Unamortized bond premium 2. 1,265 State and municipal bonds... 15,000 U.S. Treasury bonds 48,000 Stock: Domestic corporations'. 97,500 Foreign corporations'. 8,000 Land 25,500 Buildings.... 670,500 Machinery and equipment. 434,892 Office furniture.... 30,629 Trucks........ 45,264 Accumulated depreciation. 407,781 Prepaid insurance .. 2,215 Federal estimated tax payment 29 Sinking fund-Bond retirement?. 50,255 Goodwill.... (Alt+A) 1 Cash surrender value - Officers' life insurance 2 23,150 Unamortized bond issue expense 2. 8,875 Accounts payable......... 36,075 Notes payable (short term). 30,000 Accrued interest .... 2,925 Accrued payroll... 3,328 Accrued vacation pay. 18,910 Accrued taxes: IL Replacement tax.... 520 IL Franchise tax.... 300 IL Income tax..... 320 Foreign taxes.. 93 Property taxes..... 8,000 Employment taxes.... 4,110 Bonds payable (long term)...... 552,403 Capital stock: 7% Preferred...... Common...... Surplus-Paid...... Unappropriated retained earnings. Treasury stock.... 50,000 435,000 20,000 282,379 2,544 * Appropriated retained earnings 16 67,544 Dividends paid: Common stock Preferred stock 3,500 26,000 Sales........ 1,935,943 Returns and allowances... 36,395 Purchases (net).... 422,133 Inventory variation (decrease) * 21,346 Factory wages.... 149,613 Costs attributable to inventory > 5 424,441 Depreciation 227,878 Advertising. 25,815 Bad debts.... 3,923 Officers' life insurance premiums (net of CSV adjustment)........ 2,573 Office salaries'... 82,392 Salesmen's compensation'.. 91,703 Officers' compensation *. 126,000 Pensions 10,000 Utilities'... 9,720 Service guarantees 9. 8,252 Office supplies and expense 5,115 Amortized bond issue expense 700 Interest expense. 22,000 Legal and accounting fees' 12,500 Travel expense ⁹....... 6,850 Health plan costs. 20,700 Taxes: IL Replacement tax... 520 IL Franchise tax... 300 IL Income tax... 4,320 Federal Income tax.. Foreign taxes. Property taxes... Employment taxes. Interest income: Corporate bonds 10 State and municipal bonds... U.S. Treasury bonds..... Notes receivable... Trade accounts Dividends received ".. 59,971 93 8,000 25,491 1,426 788 7,125 2,300 770 9,210 Amortized bond premium 10 142 Storage rental income... Sale of scrap....... Securities sales (net) 12 15,000 411 1,758 Real estate and equipment sales 13, 17,288 Worthless stocks 12 Fire loss ..... 14 12,500 7,414 Contributions 15 Totals 2,250 $3,911,707 $3,911,707 Bonds and stock: Corporate bonds and foreign and domestic stocks are entered at Line 9 of Schedule L. 2 Sinking fund; Goodwill; Cash surrender value of officers' life insurance; Unamortized bond premium; Unamortized bond issue expense: All these asset accounts should be aggregated at Line 14 on the balance sheet, Schedule L, as "other assets." 3 Accrued taxes; Income (federal): The federal income tax for 2016, as determined on Line 31 of Form 1120, should be included in the item "Other current liabilities" on page 5, Schedule L, Line 18(d) of the balance sheet to the extent not paid as of December 31, 2016, and in full on Line 2 of Schedule M-1. Assume that the Federal estimated taxes of $60,000 were paid in equal installments by the due dates. The 2015 tax liability was $38,750. "Inventory variations: This figure represents the difference between the aggregate inventories at the beginning and the end of the tax year, as part of the cost of goods sold. (This figure would not be entered on Form 1120; it is solely a book figure.) Falcon used the lower of cost or market method for the valuation of inventory. There was no change in this method from previous years. 5 Costs attributable to inventory: Costs attributable to inventory are the indirect UNICAP costs reported on line 5 of Form 1125-A. For Falcon, these costs include a portion ($8,444) of the officers' salaries. Falcon's total indirect costs are $424,441, as shown on the trial balance sheet for 2016. None of these indirect costs are included in the amount of expenses listed elsewhere on the trial balance sheet. Depreciation: The Falcon Machinery Corporation purchased machinery (7-year recovery property) in August 2016 at a cost of $300,000. Falcon claimed $150,000 Code Sec. 179 expense deduction and depreciates the remaining basis using MACRS straight-line with a 7-year recovery period. The rate for the current year is 7.14%. Falcon elected not to claim bonus depreciation. Construction of a factory building (39-year recovery property) was completed during June 2016 at a cost of $250,000 and depreciated under the MACRS straight-line method. The rate for the current year is 1.391%. This building was constructed on land that was purchased for $8,000. For machinery (7-year recovery property) purchased in July 2015 at a cost of $134,892, the company uses the regular MACRS method and a 7-year recovery period. Depreciation for 2015 used a rate of 14.29%, while the 2016 rate is 24.49%. Neither bonus depreciation nor a Code Sec. 179 deduction was elected. For office furniture and fixtures (7-year property) purchased in April 2014 at a cost of $30,629, the company uses the regular MACRS method and a 7-year recovery period. Depreciation for 2014 and 2015 used rates of 14.29% and 24.49%, respectively, while the 2016 rate is 17.49%. Based on projected future earnings, Falcon decides to elect out of claiming both bonus depreciation and Code Sec. 179 expense deductions. For a truck (5-year recovery property that is not subject to Code Sec. 280F) purchased in 2015 at a cost of $45,264, the company uses the regular MACRS method and a 5-year recovery period. Depreciation for 2015 used a rate of 20%. The 2016 depreciation rate is 32%. Neither bonus depreciation nor a Code Sec. 179 deduction was elected. A shed placed in service on January 2, 2006 was destroyed by fire in February 2016. The MACRS deduction claimed in previous years is $2,554, and the full-year depreciation for 2016 would otherwise be $256. The property cost $10,000, and there is no insurance recovery. The total cost of the original factory buildings placed in service in 2003 was $420,500. Accumulated depreciation on these buildings is $139,728. 'Office salaries; Salesmen's compensation: The aggregate of these two items should be entered at Line 13, page 1 of Form 1120. Officers' compensation: Compensation of $54,000 was paid to the president, F.L. Davis (social security number 252-67-8315). He owned 15 percent of the common stock. Compensation of $41,500 was paid to the vice-president, B.L. West (social security number 296- 40-7222), who owned 10 percent of the common stock. Compensation of $38,944 was paid to the secretary-treasurer, T.N. Dorst (social security number 307-31-3433), who owned 10 percent of the common stock. All three worked full time for the corporation. As noted above, $8,444 of the salaries paid to the officers consists of costs attributable to inventory. Note: Form 1125-E should be completed before entering any amounts on Line 12, page 1 of Form 1120. "Insurance; Utilities; Service guarantees; Office supplies and expense; Legal and accounting fees; Amortized bond issue expense; Travel expenses: 'The aggregate of these items is entered on Line 26, page 1 of Form 1120. 10 Interest income; Corporate bonds; Amortized bond premium: Corporate bonds were purchased on July 1, 2015, for $23,875. The bonds mature on December 31, 2023, have a face value of $22,400, pay interest at 7%, and are expected to yield an effective rate of return of 6% (3% every six months for 17 periods). Falcon has elected to amortize the bond premium. The amortization for 2016 is $142 and is offset against the interest income reported on Line 5, page 1 of Form 1120. The carrying value of the bonds at the beginning of 2016 was $23,807. "Dividends received; Domestic corporations: Falcon received $6,850 in dividends from Dunbar Steel, Inc. and $2,120 from Marshall Co. Both are domestic corporations and the dividends qualify for the 70% deduction. A cash dividend of $240 was received from Canadian Shipping, Ltd., a foreign corporation. 12 Securities sales and worthless stock: On February 3, 2016, the corporation sold 100 shares of XYZ Corp. stock for $20,500. The stock was bought on May 26, 2015, for $18,487. On January 26, 2016, the corporation sold 200 shares of ABC Corp. preferred stock for $4,400. The stock had cost $4,755 on April 14, 2015. On May 14, 2016, the corporation sold for $15,100, net, U.S. Treasury bonds which had cost $15,000 on June 9, 2010. A 1099-B was received for these sales with the basis reported to the IRS. Further, 250 shares of Zero Corp. common stock became worthless in 2016. It was acquired on January 30, 2005, for $12,500, which was its adjusted basis at the time it became worthless. 13 Real estate sale: On July 5, 2016, the corporation sold vacant land for $30,000. It paid $12,712 for the land on June 1, 2006. The land had been used in the corporation's business. (The sale would be reported on Form 4797, Part I, and the gain should be carried over to Schedule D, Line 11.) 14 Fire loss: A shed used by the corporation in its manufacturing was destroyed by fire in February 2016. There was no insurance recovery. The shed had been acquired on January 2, 2006, at a cost of $10,000. Accumulated depreciation of $2,554 had been deducted prior to 2016. The shed had a fair market value of $3,000 prior to the fire, and a zero fair market value after the fire. 15 Contributions: Contributions were made to the following organizations: United Charities, $750; Boy Scouts of America, $500; Red Cross, $250; and Community Fund, $750. 16 Appropriated retained earnings: This figure includes appropriations of $50,000 for sinking fund requirements (bond retirement fund), $15,000 for contingencies, and $2,544 for the cost of treasury stock. During 2016, there were appropriations of $10,000 to the sinking fund reserve and $3,000 to the contingency reserve. BALANCE SHEET AS OF JANUARY 1, 2016 Assets............... Cash............... Notes and accounts receivable......... Inventories............ Corporate bonds....... Unamortized bond premium....... State and municipal bonds. U.S. Treasury bonds......... Stocks: Domestic corporations............. $ 22,020 63,115 355,240 22,400 1,407 15,000 63,000 133,242 Foreign corporation.......... 8,000 Land............... 30,212 Building............ 430,500 Machinery and equipment.. 134,892 Office furniture....... 30,629 Trucks.............. 45,264 Accumulated depreciation...... (182,489) 458,796 Sinking fund-Bond retirement.. 40,015 Goodwill............ 1 Cash surrender value of officers' life insurance.... 15,000 Total Assets.......... $1,227,448 Liabilities and Equity. Accounts payable.......... Notes payable (short-term) Other current liabilities: Accrued interest. Accrued payroll......... $ 39,456 40,000 758 7,439 Accrued vacation pay. 24,578 Accrued state income tax......... 4,185 Accrued property tax......... Accrued employment taxes.. 7,200 26,453 Bonds payable (long term). 225,000 Capital stock: 7% Preferred... Common ....... 50,000 435,000 Paid in surplus... 20,000 Treasury stock... (2,544) Retained Earnings: Unappropriated retained earnings. 295,379 Appropriated retained earnings......... Total Liabilities and Equity...... 54,544 $1,227,448 Additional Information The corporation had a $100 capital loss carryover from 2015. The corporation furnished the Government with information returns on Forms 1096 and 1099 for the dividends it paid during 2016 and also for other payments it made that required information returns. For purposes of the signatures on page 1 of Form 1120, it is assumed that John Service, of John Service, CPA, P.C. (EIN 36-1120987) pre- pared the return. His address is 1510 Steward Building, Suite 1500, Chicago, Illinois 60672; telephone number 312-555-1120; his PTIN is P11624121; and F.L. Davis, President, has authorized John to discuss Falcon Machinery Inc.'s tax return with the IRS.

Expert Answer:

Answer rating: 100% (QA)

Depreciation of a shed A shed placed in service on January 2 2006 was destroyed by fire in February ... View the full answer

Related Book For

Business Law Legal Environment Online Commerce Business Ethics and International Issues

ISBN: 978-0134004006

9th edition

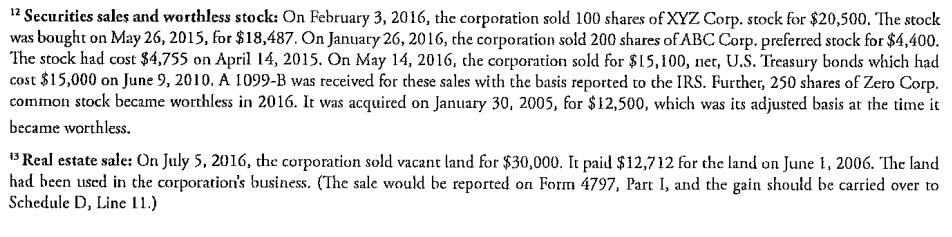

Authors: Henry R. Cheeseman

Posted Date:

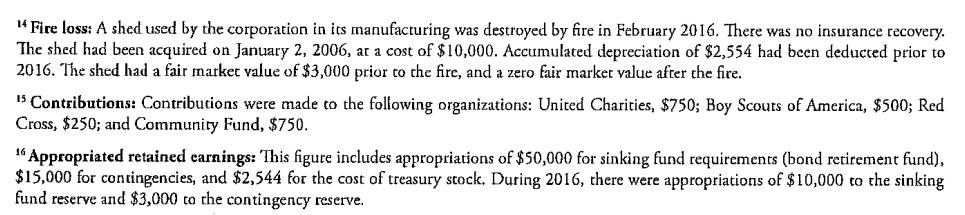

Students also viewed these law questions

-

The Fruehauf Corporation (Fruehauf) is engaged in the manufacture of large trucks and industrial vehicles. The Edelman group (Edelman) made a cash tender offer for the shares of Fruehauf for $ 48.50...

-

Teller Pen is engaged in the manufacture of mechanical pens and pencils, porous pens, and a recently developed line of disposable lighters. Since the firm sells to a great many distributors, and its...

-

The Arrowroot Corporation is engaged in the manufacture and distribution of fine spices for the restaurant market. It has been in this business for 30 years. Arrowroot has also been in the specialty...

-

2. Evaluate the following definite integrals (a) (2x - 6x) dx /6 (b) 16 cos 3t + 2 sin 3t dt x+1 2 da

-

Use the sum-of-the-years'-digits depreciation method to make a depreciation schedule (first three years) for a forklift that cost $28,000, has an expected useful life often years, and has a residual...

-

What could be included in an effective opening and closing of a claim or complaint letter?

-

Bert C. Roberts Jr. was chairman of WorldComs board of directors. Immediately before that, he had been chairman of MCI, which WorldCom acquired on September 14, 1998, in a transaction valued at...

-

Classification of Costs and Interest Capitalization On January 1, 2010, Blair Corporation purchased for $500,000 a tract of land (site number 101) with a building. Blair paid a real estate brokers...

-

Q2 If Z is a normal N (0, 1), then the X = tz; process is continuous and is marginally distributed as a normal N (0, t). Is X a Brownian motion?

-

Overview The milestone for Project One involves applying accounting principles and methods to long-term liabilities and equity. You will also evaluate these financial statement components for...

-

In the year 2008, Wiggins Processing Company had the following contribution income statement: WIGGINS PROCESSING COMPANY Contribution Income Statement For the Year 2008 Sales Variable costs Cost of...

-

Table: Marginal Tax Rates Income Bracket Marginal Tax Rate $0?12,000 0% 12,001?24,000 8 24,001?40,000 12 40,001?70,000 16 How much income tax is owed on an income of $50,000?

-

What are the THREE different transfer pricing methods for internal transfer of goods / services ? Briefly describe each method.

-

1. (3.5 points total) Bacteria with the formula C10H1304N2 (MW = 225.0 g/mol) is grown in a batch reactor on sugar bagasse (C11H1809, MW = 294.0 g/mol) as the carbon source for the production of...

-

In Sade's song Is It A Crime she sings about a cheatingboyfriend whom shes trying to woo back. Some of the lyrics go: It may come, it may come as some surprise But I miss you I could see through, all...

-

QUESTION 11 An avocado costs 2 dollars in Miami and 6,000 pesos in Bogota. How many pesos can be purchased with 1 dollar IF purchasing power parity holds? Enter your answer using whole numbers. Do...

-

What is the difference between a stock and a bond? What is the purpose of a stock exchange? What is diversification in investing? What is a mutual fund? What is a hedge fund? What is the difference...

-

A line l passes through the points with coordinates (0, 5) and (6, 7). a. Find the gradient of the line. b. Find an equation of the line in the form ax + by + c = 0.

-

James L. Skip Deupree, a developer, was building a development of townhouses called Point South in Destin, Florida. All the townhouses in the development were to have individual boat slips. Sam and...

-

Ally is a member and a manager of a manager managed limited liability company called Movers & You, LLC, a moving company. The main business of Movers & You, LLC, is moving large corporations from old...

-

The employees of the Shop Rite Foods, Inc. (Shop Rite), warehouse in Lubbock, Texas, elected the United Packinghouse, Food and Allied Workers (Union) as its bargaining agent. Negotiations for a...

-

Which of Yellows statements regarding the factors affecting the selection of a trading strategy is correct? A. Statement 1 B. Statement 2 C. Statement 3 Robert Harding is a portfolio manager at...

-

Given the parameters for the benchmark given by Harding, Yellow should recommend a benchmark that is based on the: A. arrival price. B. time-weighted average price. C. volume-weighted average price....

-

To fill the remaining portion of the ABC order, Yellow is using: A. an arrival price trading strategy. B. a TWAP participation strategy. C. a VWAP participation strategy. Robert Harding is a...

Study smarter with the SolutionInn App